Untransferred completed projects under the TF - ₱87,392,781.11

4. Fourteen completed projects under the TF totaling ₱87,392,781.11 were not

transferred to the GF due to insufficient monitoring and improper recording,

contrary to Section 104(1.i) of the NGAS Manual, Volume I and IPSAS No. 17, thus,

overstating the Construction in Progress (CIP) account in the TF while understating

the related PPE accounts in the GF by the same amount, as well as the depreciation

expense by ₱29,358,125.96, which affected the fair presentation of these accounts in

the financial statements.

4.1. During the construction period, PPE shall be classified as CIP with the appropriate

asset classification. As soon as these are completed, the CIP accounts shall then be

transferred to their appropriate asset accounts. The CIP account is used to record the

value of work performed in accordance with the terms of the applicable construction

contracts.

4.2. Section 104(1.i) of the NGAS Manual for LGUs, Volume I, requires that completed

projects under the TF be transferred to the GF upon their completion.

4.3. Moreover, with the adoption of the IPSAS, infrastructure assets shall be taken up as

PPE, and the annual consumption of their service potential along with any loss of

value due to depreciation and impairment shall also be recognized.

4.4. Depreciation is defined under IPSAS No. 17 as the systematic allocation of the

depreciable amount of an asset over its useful life. Paragraph 71 of IPSAS No. 17

provides that “depreciation of an asset begins when it is available for use i.e., when

it is in the location and condition necessary for it to be capable of operating in the

manner intended by management.”

4.5. Item 4.1 of the Philippine Application Guideline for IPSAS No. 17 states that “xxx

For simplicity and to avoid proportionate computation, depreciation shall be for one

month if the PPE is available for use on or before the 15th of the month. However, if

the PPE is available for use after the 15th of the month, depreciation shall be for the

succeeding month.”

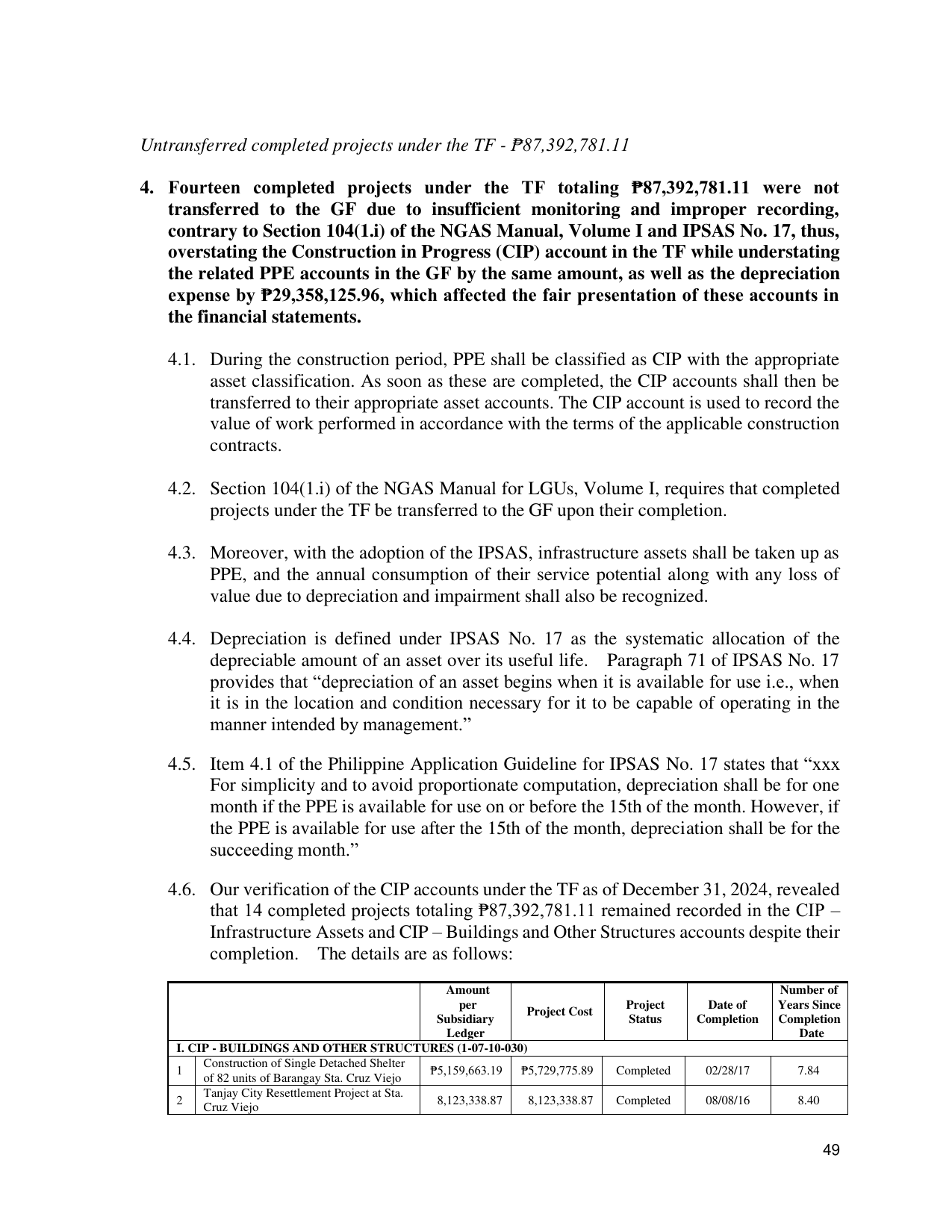

4.6. Our verification of the CIP accounts under the TF as of December 31, 2024, revealed

that 14 completed projects totaling ₱87,392,781.11 remained recorded in the CIP –

Infrastructure Assets and CIP – Buildings and Other Structures accounts despite their

completion. The details are as follows:

Amount Number of

per Project Date of Years Since

Project Cost

Subsidiary Status Completion Completion

Ledger Date

I. CIP - BUILDINGS AND OTHER STRUCTURES (1-07-10-030)###########

Construction of Single Detached Shelter

1 ₱5,159,663.19 ₱5,729,775.89 Completed 02/28/17 7.84

of 82 units of Barangay Sta. Cruz Viejo

Tanjay City Resettlement Project at Sta.

2 8,123,338.87 8,123,338.87 Completed 08/08/16 8.40

Cruz Viejo

49