b) Any costs directly attributable to bringing the asset to the location and

condition necessary for it to be capable of operating in the manner intended

by management.

c) The initial estimate of the costs of dismantling and removing the item and

restoring the site on which it is located, the obligation for which an entity

incurs either when the item is acquired, or as a consequence of having used

the item during a particular period for purposes other than to produce

inventories during that period.

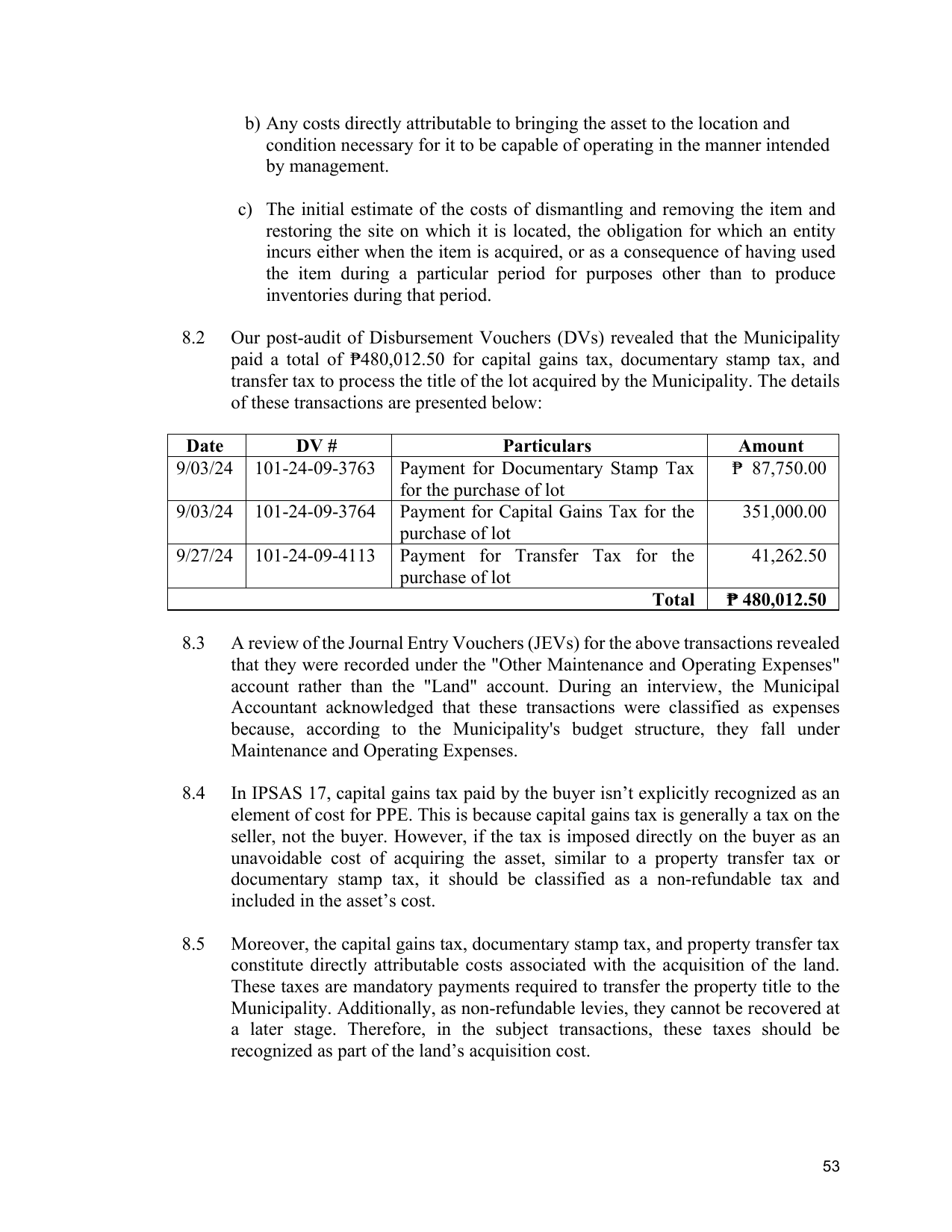

8.2 Our post-audit of Disbursement Vouchers (DVs) revealed that the Municipality

paid a total of ₱480,012.50 for capital gains tax, documentary stamp tax, and

transfer tax to process the title of the lot acquired by the Municipality. The details

of these transactions are presented below:

Date DV # Particulars Amount

9/03/24 101-24-09-3763 Payment for Documentary Stamp Tax ₱ 87,750.00

for the purchase of lot

9/03/24 101-24-09-3764 Payment for Capital Gains Tax for the 351,000.00

purchase of lot

9/27/24 101-24-09-4113 Payment for Transfer Tax for the 41,262.50

purchase of lot

Total ₱ 480,012.50

8.3 A review of the Journal Entry Vouchers (JEVs) for the above transactions revealed

that they were recorded under the "Other Maintenance and Operating Expenses"

account rather than the "Land" account. During an interview, the Municipal

Accountant acknowledged that these transactions were classified as expenses

because, according to the Municipality's budget structure, they fall under

Maintenance and Operating Expenses.

8.4 In IPSAS 17, capital gains tax paid by the buyer isn’t explicitly recognized as an

element of cost for PPE. This is because capital gains tax is generally a tax on the

seller, not the buyer. However, if the tax is imposed directly on the buyer as an

unavoidable cost of acquiring the asset, similar to a property transfer tax or

documentary stamp tax, it should be classified as a non-refundable tax and

included in the asset’s cost.

8.5 Moreover, the capital gains tax, documentary stamp tax, and property transfer tax

constitute directly attributable costs associated with the acquisition of the land.

These taxes are mandatory payments required to transfer the property title to the

Municipality. Additionally, as non-refundable levies, they cannot be recovered at

a later stage. Therefore, in the subject transactions, these taxes should be

recognized as part of the land’s acquisition cost.

53