Page 89 of 124

STATUS OF

REFERENCE OBSERVATION RECOMMENDATION IMPLEMENTATION /

RESULTS OF VALIDATION

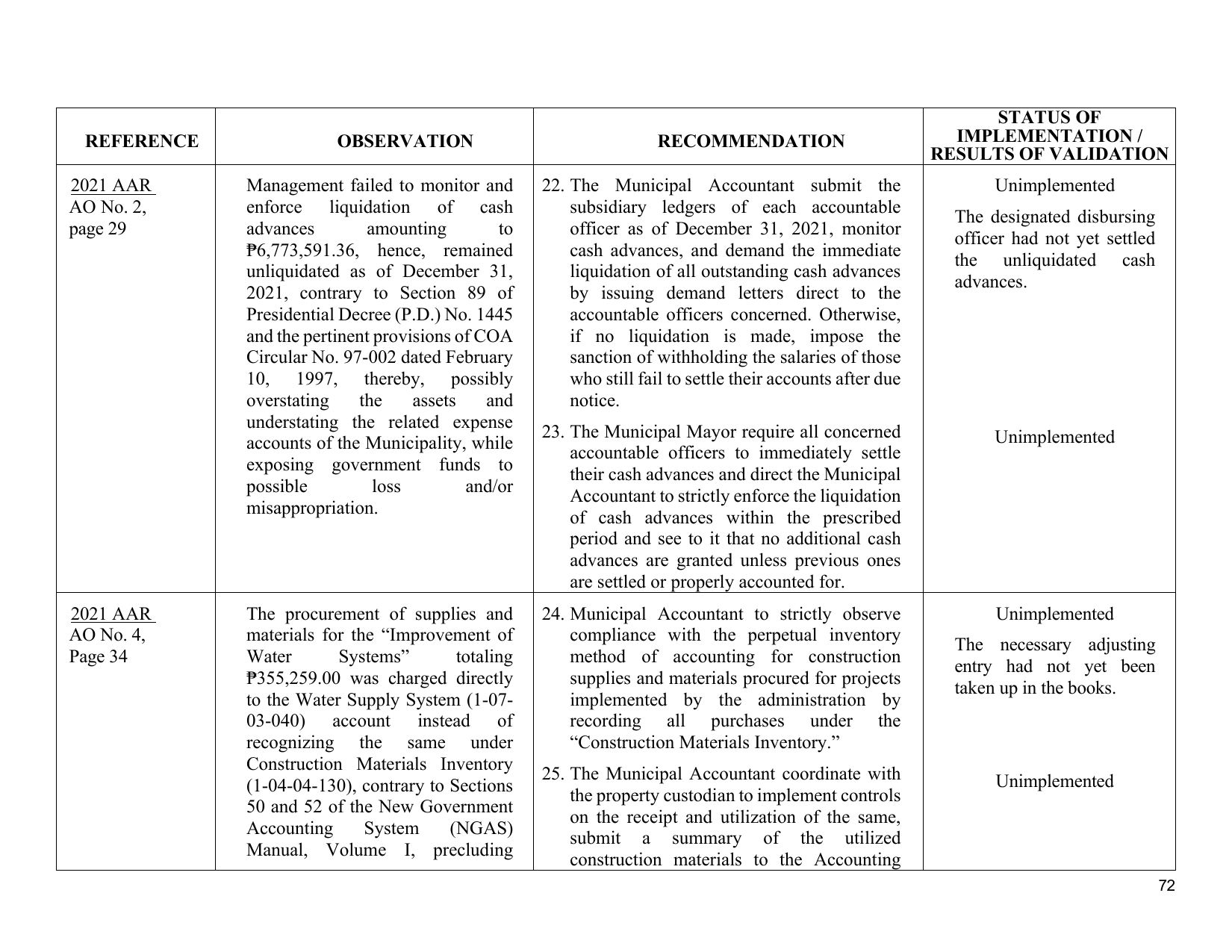

2021 AAR Management failed to monitor and 22. The Municipal Accountant submit the Unimplemented

AO No. 2, enforce liquidation of cash subsidiary ledgers of each accountable

The designated disbursing

page 29 advances amounting to officer as of December 31, 2021, monitor

officer had not yet settled

₱6,773,591.36, hence, remained cash advances, and demand the immediate

the unliquidated cash

unliquidated as of December 31, liquidation of all outstanding cash advances

advances.

2021, contrary to Section 89 of by issuing demand letters direct to the

Presidential Decree (P.D.) No. 1445 accountable officers concerned. Otherwise,

and the pertinent provisions of COA if no liquidation is made, impose the

Circular No. 97-002 dated February sanction of withholding the salaries of those

10, 1997, thereby, possibly who still fail to settle their accounts after due

overstating the assets and notice.

understating the related expense

23. The Municipal Mayor require all concerned Unimplemented

accounts of the Municipality, while

accountable officers to immediately settle

exposing government funds to

their cash advances and direct the Municipal

possible loss and/or

Accountant to strictly enforce the liquidation

misappropriation.

of cash advances within the prescribed

period and see to it that no additional cash

advances are granted unless previous ones

are settled or properly accounted for.

2021 AAR The procurement of supplies and 24. Municipal Accountant to strictly observe Unimplemented

AO No. 4, materials for the “Improvement of compliance with the perpetual inventory

The necessary adjusting

Page 34 Water Systems” totaling method of accounting for construction

entry had not yet been

₱355,259.00 was charged directly supplies and materials procured for projects

taken up in the books.

to the Water Supply System (1-07- implemented by the administration by

03-040) account instead of recording all purchases under the

recognizing the same under “Construction Materials Inventory.”

Construction Materials Inventory

25. The Municipal Accountant coordinate with Unimplemented

(1-04-04-130), contrary to Sections

the property custodian to implement controls

50 and 52 of the New Government

on the receipt and utilization of the same,

Accounting System (NGAS)

submit a summary of the utilized

Manual, Volume I, precluding

construction materials to the Accounting

72