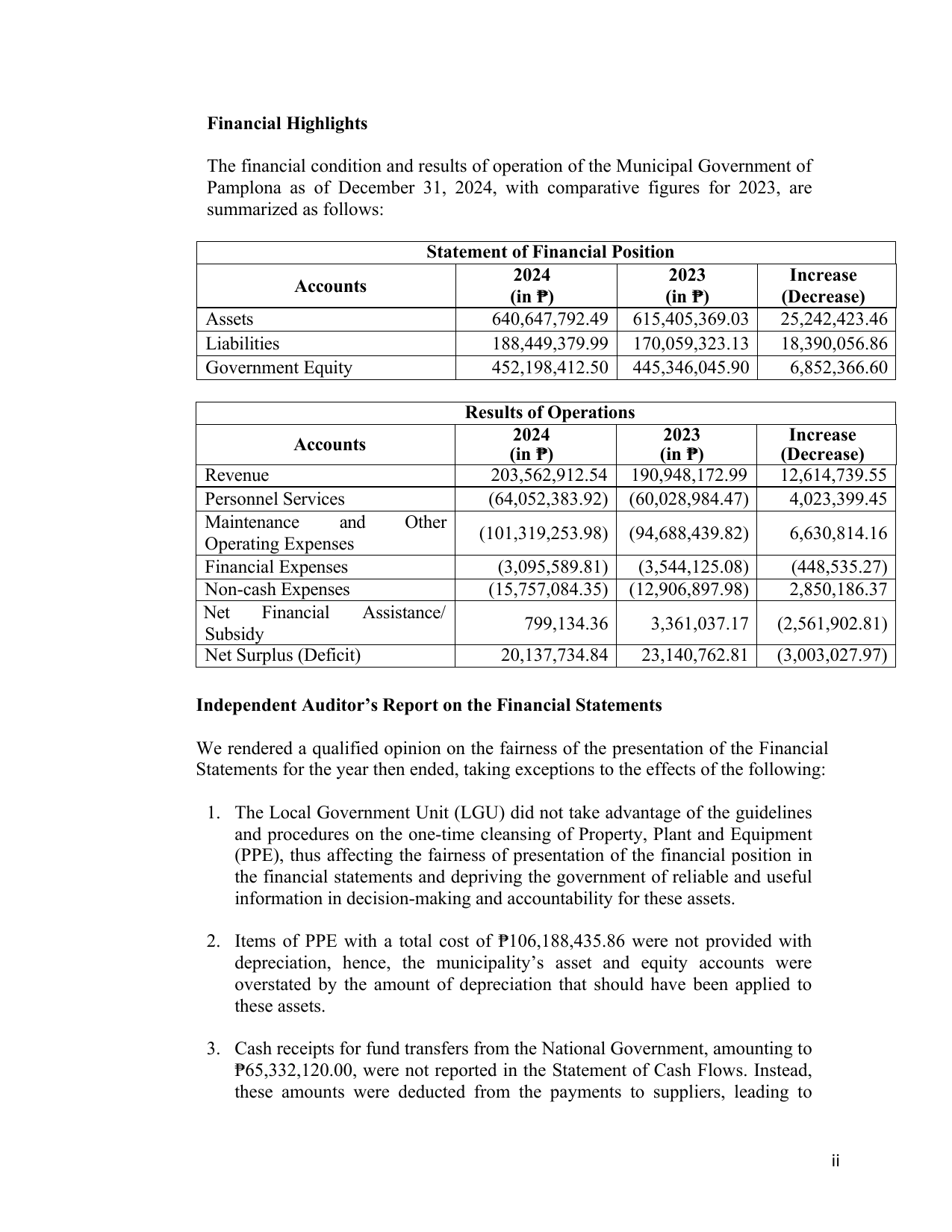

Financial Highlights

The financial condition and results of operation of the Municipal Government of

Pamplona as of December 31, 2024, with comparative figures for 2023, are

summarized as follows:

Statement of Financial Position

2024 2023 Increase

Accounts

(in ₱) (in ₱) (Decrease)

Assets 640,647,792.49 615,405,369.03 25,242,423.46

Liabilities 188,449,379.99 170,059,323.13 18,390,056.86

Government Equity 452,198,412.50 445,346,045.90 6,852,366.60

Results of Operations

2024 2023 Increase

Accounts

(in ₱) (in ₱) (Decrease)

Revenue 203,562,912.54 190,948,172.99 12,614,739.55

Personnel Services (64,052,383.92) (60,028,984.47) 4,023,399.45

Maintenance and Other

(101,319,253.98) (94,688,439.82) 6,630,814.16

Operating Expenses

Financial Expenses (3,095,589.81) (3,544,125.08) (448,535.27)

Non-cash Expenses (15,757,084.35) (12,906,897.98) 2,850,186.37

Net Financial Assistance/

799,134.36 3,361,037.17 (2,561,902.81)

Subsidy

Net Surplus (Deficit) 20,137,734.84 23,140,762.81 (3,003,027.97)

Independent Auditor’s Report on the Financial Statements

We rendered a qualified opinion on the fairness of the presentation of the Financial

Statements for the year then ended, taking exceptions to the effects of the following:

1. The Local Government Unit (LGU) did not take advantage of the guidelines

and procedures on the one-time cleansing of Property, Plant and Equipment

(PPE), thus affecting the fairness of presentation of the financial position in

the financial statements and depriving the government of reliable and useful

information in decision-making and accountability for these assets.

2. Items of PPE with a total cost of ₱106,188,435.86 were not provided with

depreciation, hence, the municipality’s asset and equity accounts were

overstated by the amount of depreciation that should have been applied to

these assets.

3. Cash receipts for fund transfers from the National Government, amounting to

₱65,332,120.00, were not reported in the Statement of Cash Flows. Instead,

these amounts were deducted from the payments to suppliers, leading to

ii