EXECUTIVE SUMMARY

Introduction

The Municipality of Pamplona was formerly among the sitios of the City of

Tanjay. However, on June 16, 1950, it became a town in the Province of Negros

Oriental by the enactment of Republic Act No. 535. Pamplona has 16 barangays

and is currently classified as a 3rd class municipality. It is located 38 kilometers

northwest of Dumaguete City and 7.5 kilometers west of the City of Tanjay.

According to the 2020 census, it had a population of 39,805 people.

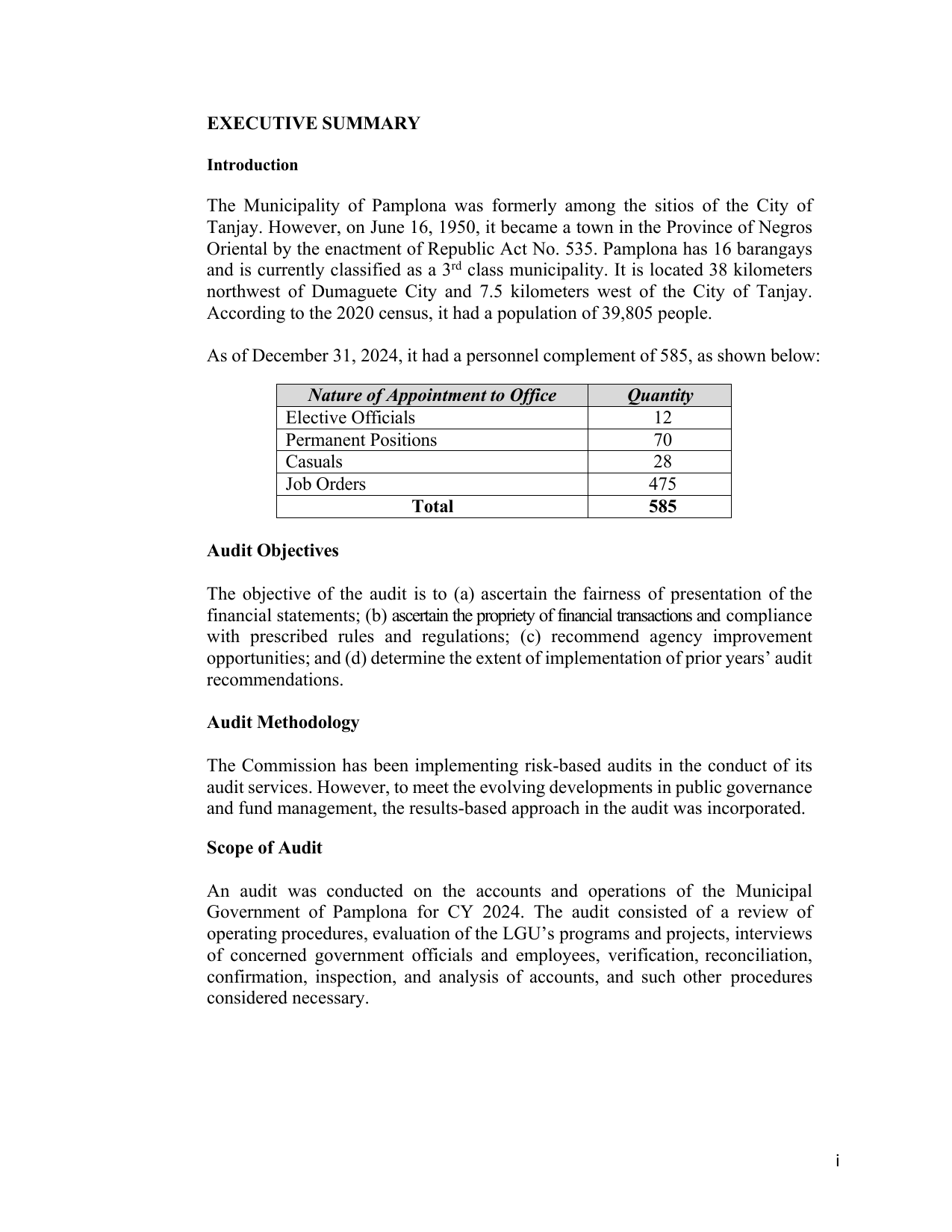

As of December 31, 2024, it had a personnel complement of 585, as shown below:

Nature of Appointment to Office Quantity

Elective Officials 12

Permanent Positions 70

Casuals 28

Job Orders 475

Total 585

Audit Objectives

The objective of the audit is to (a) ascertain the fairness of presentation of the

financial statements; (b) ascertain the propriety of financial transactions and compliance

with prescribed rules and regulations; (c) recommend agency improvement

opportunities; and (d) determine the extent of implementation of prior years’ audit

recommendations.

Audit Methodology

The Commission has been implementing risk-based audits in the conduct of its

audit services. However, to meet the evolving developments in public governance

and fund management, the results-based approach in the audit was incorporated.

Scope of Audit

An audit was conducted on the accounts and operations of the Municipal

Government of Pamplona for CY 2024. The audit consisted of a review of

operating procedures, evaluation of the LGU’s programs and projects, interviews

of concerned government officials and employees, verification, reconciliation,

confirmation, inspection, and analysis of accounts, and such other procedures

considered necessary.

i