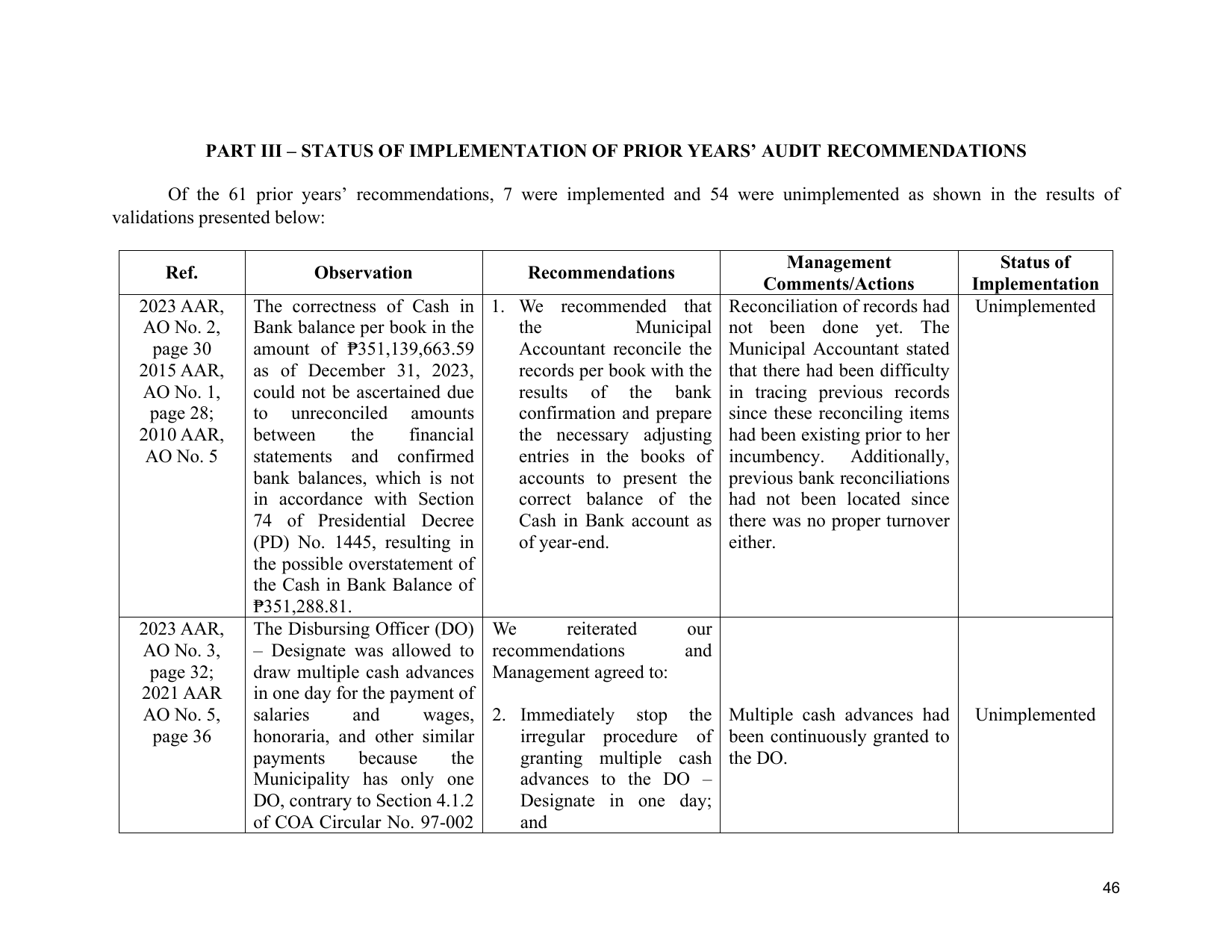

PART III – STATUS OF IMPLEMENTATION OF PRIOR YEARS’ AUDIT RECOMMENDATIONS

Of the 61 prior years’ recommendations, 7 were implemented and 54 were unimplemented as shown in the results of

validations presented below:

Management Status of

Ref. Observation Recommendations

Comments/Actions Implementation

2023 AAR, The correctness of Cash in 1. We recommended that Reconciliation of records had Unimplemented

AO No. 2, Bank balance per book in the the Municipal not been done yet. The

page 30 amount of ₱351,139,663.59 Accountant reconcile the Municipal Accountant stated

2015 AAR, as of December 31, 2023, records per book with the that there had been difficulty

AO No. 1, could not be ascertained due results of the bank in tracing previous records

page 28; to unreconciled amounts confirmation and prepare since these reconciling items

2010 AAR, between the financial the necessary adjusting had been existing prior to her

AO No. 5 statements and confirmed entries in the books of incumbency. Additionally,

bank balances, which is not accounts to present the previous bank reconciliations

in accordance with Section correct balance of the had not been located since

74 of Presidential Decree Cash in Bank account as there was no proper turnover

(PD) No. 1445, resulting in of year-end. either.

the possible overstatement of

the Cash in Bank Balance of

₱351,288.81.

2023 AAR, The Disbursing Officer (DO) We reiterated our

AO No. 3, – Designate was allowed to recommendations and

page 32; draw multiple cash advances Management agreed to:

2021 AAR in one day for the payment of

AO No. 5, salaries and wages, 2. Immediately stop the Multiple cash advances had Unimplemented

page 36 honoraria, and other similar irregular procedure of been continuously granted to

payments because the granting multiple cash the DO.

Municipality has only one advances to the DO –

DO, contrary to Section 4.1.2 Designate in one day;

of COA Circular No. 97-002 and

46