2. The balances of the Real Property Tax (RPT) Receivable and Special Education Tax

(SET) Receivable accounts as of December 31, 2024, between the records of the

Municipal Accounting Office (MAO) and the Municipal Treasurer’s Office (MTO)

showed a difference of ₱90,418,239.18 due to the non-reconciliation of their records thus,

the RPT/SET Receivable and Deferred Income accounts, as presented in the financial

statements, are deemed unreliable.

We recommended that the Municipal Mayor instruct the Municipal Accountant and

Municipal Treasurer to reconcile the difference amounting to ₱90,418,239.18 between

the Real Property Tax (RPT) and Special Education Tax (SET) Receivables account

balances.

To prevent the further accumulation of unreconciled differences, we further

recommended that they, in coordination with the Municipal Assessor, conduct regular

and timely reconciliations of the total collectibles from the Basic and Special Education

Taxes against the recorded RPT and SET Receivables account balances.

Additionally, to promote transparency and ensure full disclosure, we recommended that

any remaining unreconciled differences be properly reported in the Notes to the Financial

Statements.

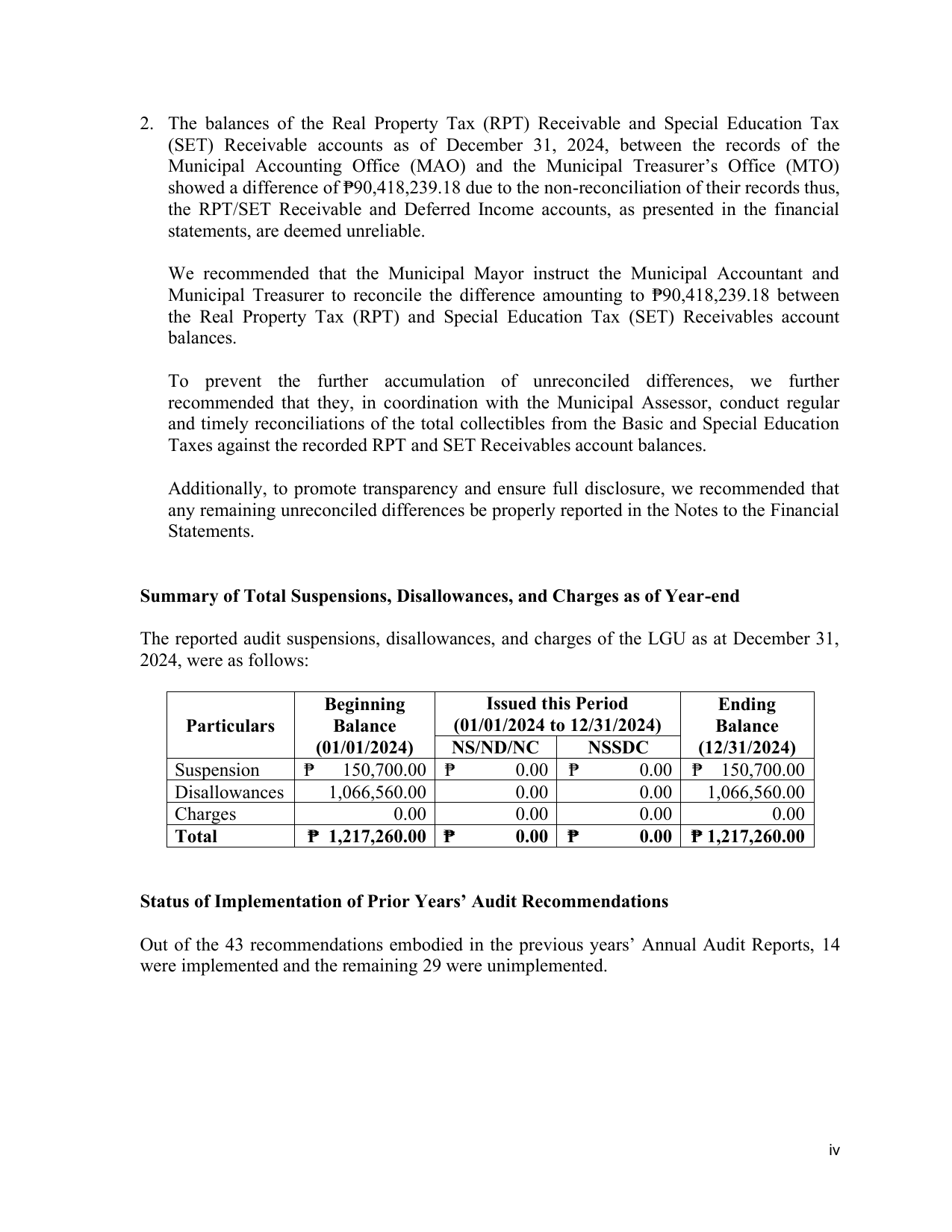

Summary of Total Suspensions, Disallowances, and Charges as of Year-end

The reported audit suspensions, disallowances, and charges of the LGU as at December 31,

2024, were as follows:

Beginning Issued this Period Ending

Particulars Balance (01/01/2024 to 12/31/2024) Balance

(01/01/2024) NS/ND/NC NSSDC (12/31/2024)

Suspension ₱ 150,700.00 ₱ 0.00 ₱ 0.00 ₱ 150,700.00

Disallowances 1,066,560.00 0.00 0.00 1,066,560.00

Charges 0.00 0.00 0.00 0.00

Total ₱ 1,217,260.00 ₱ 0.00 ₱ 0.00 ₱ 1,217,260.00

Status of Implementation of Prior Years’ Audit Recommendations

Out of the 43 recommendations embodied in the previous years’ Annual Audit Reports, 14

were implemented and the remaining 29 were unimplemented.

iv