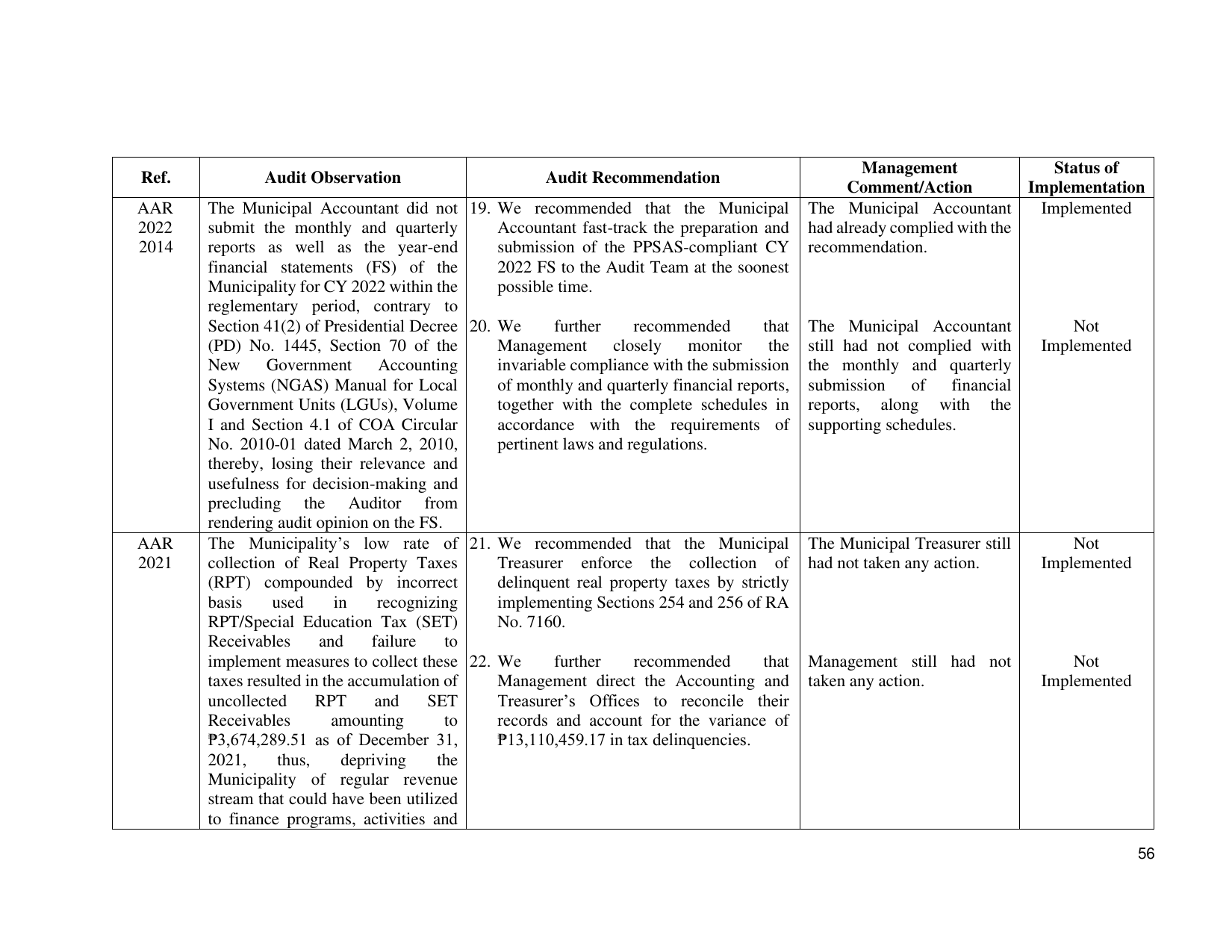

Management Status of

Ref. Audit Observation Audit Recommendation

Comment/Action Implementation

AAR The Municipal Accountant did not 19. We recommended that the Municipal The Municipal Accountant Implemented

2022 submit the monthly and quarterly Accountant fast-track the preparation and had already complied with the

2014 reports as well as the year-end submission of the PPSAS-compliant CY recommendation.

financial statements (FS) of the 2022 FS to the Audit Team at the soonest

Municipality for CY 2022 within the possible time.

reglementary period, contrary to

Section 41(2) of Presidential Decree 20. We further recommended that The Municipal Accountant Not

(PD) No. 1445, Section 70 of the Management closely monitor the still had not complied with Implemented

New Government Accounting invariable compliance with the submission the monthly and quarterly

Systems (NGAS) Manual for Local of monthly and quarterly financial reports, submission of financial

Government Units (LGUs), Volume together with the complete schedules in reports, along with the

I and Section 4.1 of COA Circular accordance with the requirements of supporting schedules.

No. 2010-01 dated March 2, 2010, pertinent laws and regulations.

thereby, losing their relevance and

usefulness for decision-making and

precluding the Auditor from

rendering audit opinion on the FS.

AAR The Municipality’s low rate of 21. We recommended that the Municipal The Municipal Treasurer still Not

2021 collection of Real Property Taxes Treasurer enforce the collection of had not taken any action. Implemented

(RPT) compounded by incorrect delinquent real property taxes by strictly

basis used in recognizing implementing Sections 254 and 256 of RA

RPT/Special Education Tax (SET) No. 7160.

Receivables and failure to

implement measures to collect these 22. We further recommended that Management still had not Not

taxes resulted in the accumulation of Management direct the Accounting and taken any action. Implemented

uncollected RPT and SET Treasurer’s Offices to reconcile their

Receivables amounting to records and account for the variance of

₱3,674,289.51 as of December 31, ₱13,110,459.17 in tax delinquencies.

2021, thus, depriving the

Municipality of regular revenue

stream that could have been utilized

to finance programs, activities and

56