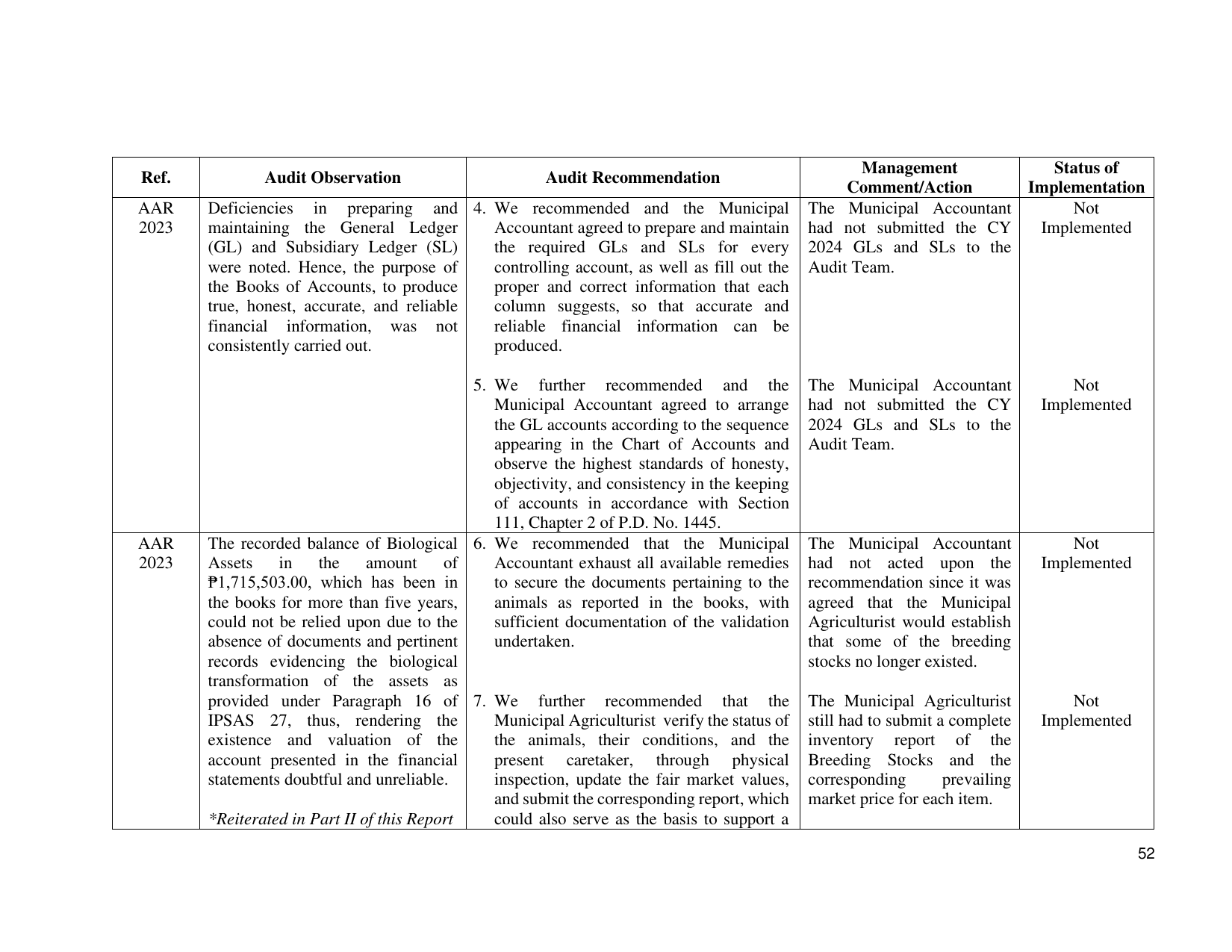

Management Status of

Ref. Audit Observation Audit Recommendation

Comment/Action Implementation

AAR Deficiencies in preparing and 4. We recommended and the Municipal The Municipal Accountant Not

2023 maintaining the General Ledger Accountant agreed to prepare and maintain had not submitted the CY Implemented

(GL) and Subsidiary Ledger (SL) the required GLs and SLs for every 2024 GLs and SLs to the

were noted. Hence, the purpose of controlling account, as well as fill out the Audit Team.

the Books of Accounts, to produce proper and correct information that each

true, honest, accurate, and reliable column suggests, so that accurate and

financial information, was not reliable financial information can be

consistently carried out. produced.

5. We further recommended and the The Municipal Accountant Not

Municipal Accountant agreed to arrange had not submitted the CY Implemented

the GL accounts according to the sequence 2024 GLs and SLs to the

appearing in the Chart of Accounts and Audit Team.

observe the highest standards of honesty,

objectivity, and consistency in the keeping

of accounts in accordance with Section

111, Chapter 2 of P.D. No. 1445.

AAR The recorded balance of Biological 6. We recommended that the Municipal The Municipal Accountant Not

2023 Assets in the amount of Accountant exhaust all available remedies had not acted upon the Implemented

₱1,715,503.00, which has been in to secure the documents pertaining to the recommendation since it was

the books for more than five years, animals as reported in the books, with agreed that the Municipal

could not be relied upon due to the sufficient documentation of the validation Agriculturist would establish

absence of documents and pertinent undertaken. that some of the breeding

records evidencing the biological stocks no longer existed.

transformation of the assets as

provided under Paragraph 16 of 7. We further recommended that the The Municipal Agriculturist Not

IPSAS 27, thus, rendering the Municipal Agriculturist verify the status of still had to submit a complete Implemented

existence and valuation of the the animals, their conditions, and the inventory report of the

account presented in the financial present caretaker, through physical Breeding Stocks and the

statements doubtful and unreliable. inspection, update the fair market values, corresponding prevailing

and submit the corresponding report, which market price for each item.

*Reiterated in Part II of this Report could also serve as the basis to support a

52