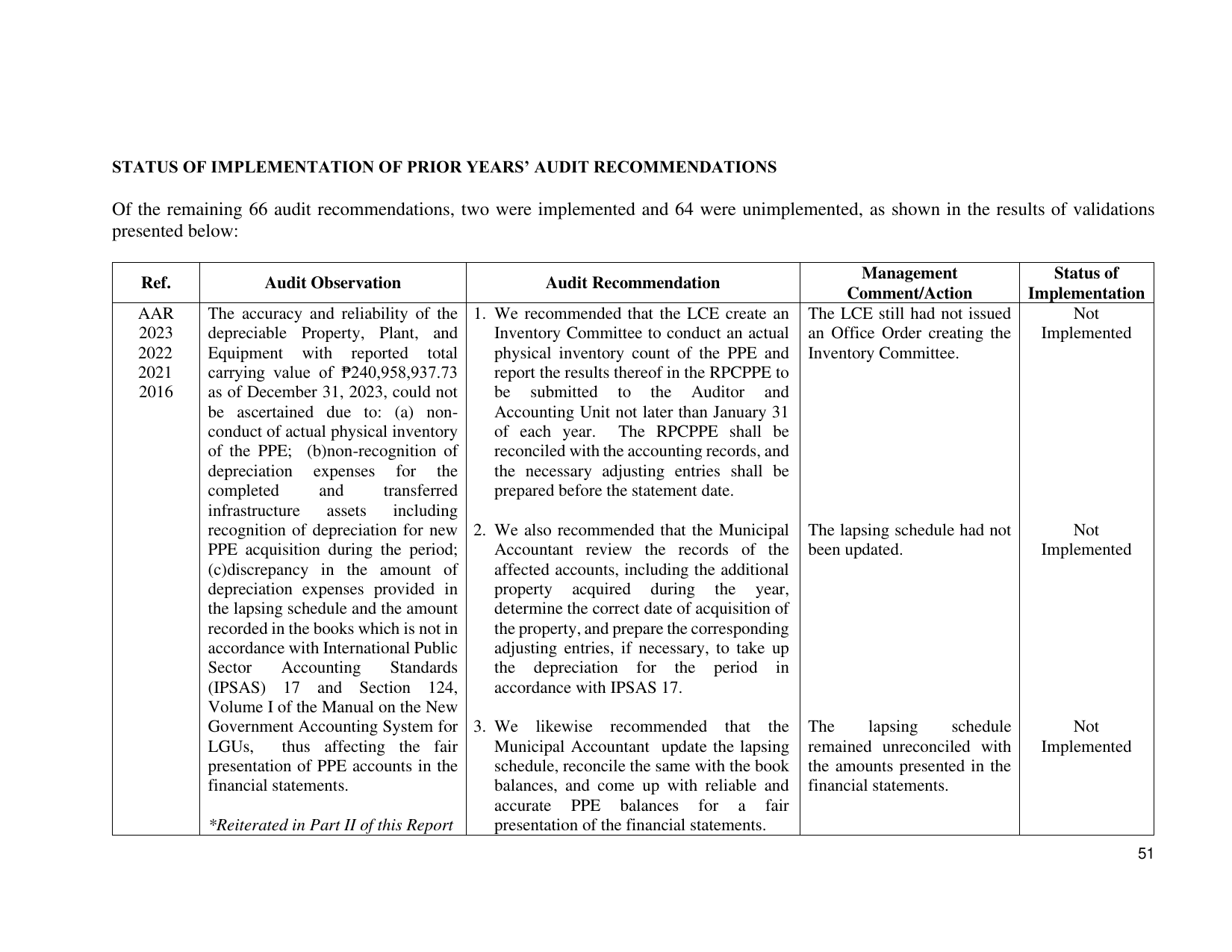

STATUS OF IMPLEMENTATION OF PRIOR YEARS’ AUDIT RECOMMENDATIONS

Of the remaining 66 audit recommendations, two were implemented and 64 were unimplemented, as shown in the results of validations

presented below:

Management Status of

Ref. Audit Observation Audit Recommendation

Comment/Action Implementation

AAR The accuracy and reliability of the 1. We recommended that the LCE create an The LCE still had not issued Not

2023 depreciable Property, Plant, and Inventory Committee to conduct an actual an Office Order creating the Implemented

2022 Equipment with reported total physical inventory count of the PPE and Inventory Committee.

2021 carrying value of ₱240,958,937.73 report the results thereof in the RPCPPE to

2016 as of December 31, 2023, could not be submitted to the Auditor and

be ascertained due to: (a) non- Accounting Unit not later than January 31

conduct of actual physical inventory of each year. The RPCPPE shall be

of the PPE; (b)non-recognition of reconciled with the accounting records, and

depreciation expenses for the the necessary adjusting entries shall be

completed and transferred prepared before the statement date.

infrastructure assets including

recognition of depreciation for new 2. We also recommended that the Municipal The lapsing schedule had not Not

PPE acquisition during the period; Accountant review the records of the been updated. Implemented

(c)discrepancy in the amount of affected accounts, including the additional

depreciation expenses provided in property acquired during the year,

the lapsing schedule and the amount determine the correct date of acquisition of

recorded in the books which is not in the property, and prepare the corresponding

accordance with International Public adjusting entries, if necessary, to take up

Sector Accounting Standards the depreciation for the period in

(IPSAS) 17 and Section 124, accordance with IPSAS 17.

Volume I of the Manual on the New

Government Accounting System for 3. We likewise recommended that the The lapsing schedule Not

LGUs, thus affecting the fair Municipal Accountant update the lapsing remained unreconciled with Implemented

presentation of PPE accounts in the schedule, reconcile the same with the book the amounts presented in the

financial statements. balances, and come up with reliable and financial statements.

accurate PPE balances for a fair

*Reiterated in Part II of this Report presentation of the financial statements.

51