4.2.2. Non-compliance with the Perpetual Inventory Method

4.2.2.1. Sections 51 and 114, Volume 1, of the NGAS Manual for LGUs

provide the proper recording and accounting for purchases of

supplies and materials in an agency. Further, the same sections state

that purchases of supplies and materials for stock, regardless of

whether they are consumed within the accounting period, shall be

recorded as assets using the inventory account following the

Perpetual Inventory Method.

4.2.2.2. Using the Perpetual Inventory Method, any purchases of supplies

and materials for stock should be recorded as inventory, irrespective

of whether they are used up within the accounting period. This

method involves maintaining an inventory control account in the

General Ledger on an ongoing basis. Additionally, detailed

inventory records must be kept for each item.

4.2.2.3. Our analysis of the year-end balances of the inventory accounts

disclosed that the ₱6,709,224.00 balance at year-end was carried

over from the CY 2023 ending balances.

4.2.2.4. The Municipal Accountant confirmed that the Perpetual Inventory

Method was not implemented, as this had long been their practice.

He also mentioned that, due to the absence of a warehouse for

storing supplies and materials, all items delivered were immediately

issued to the respective requesting offices.

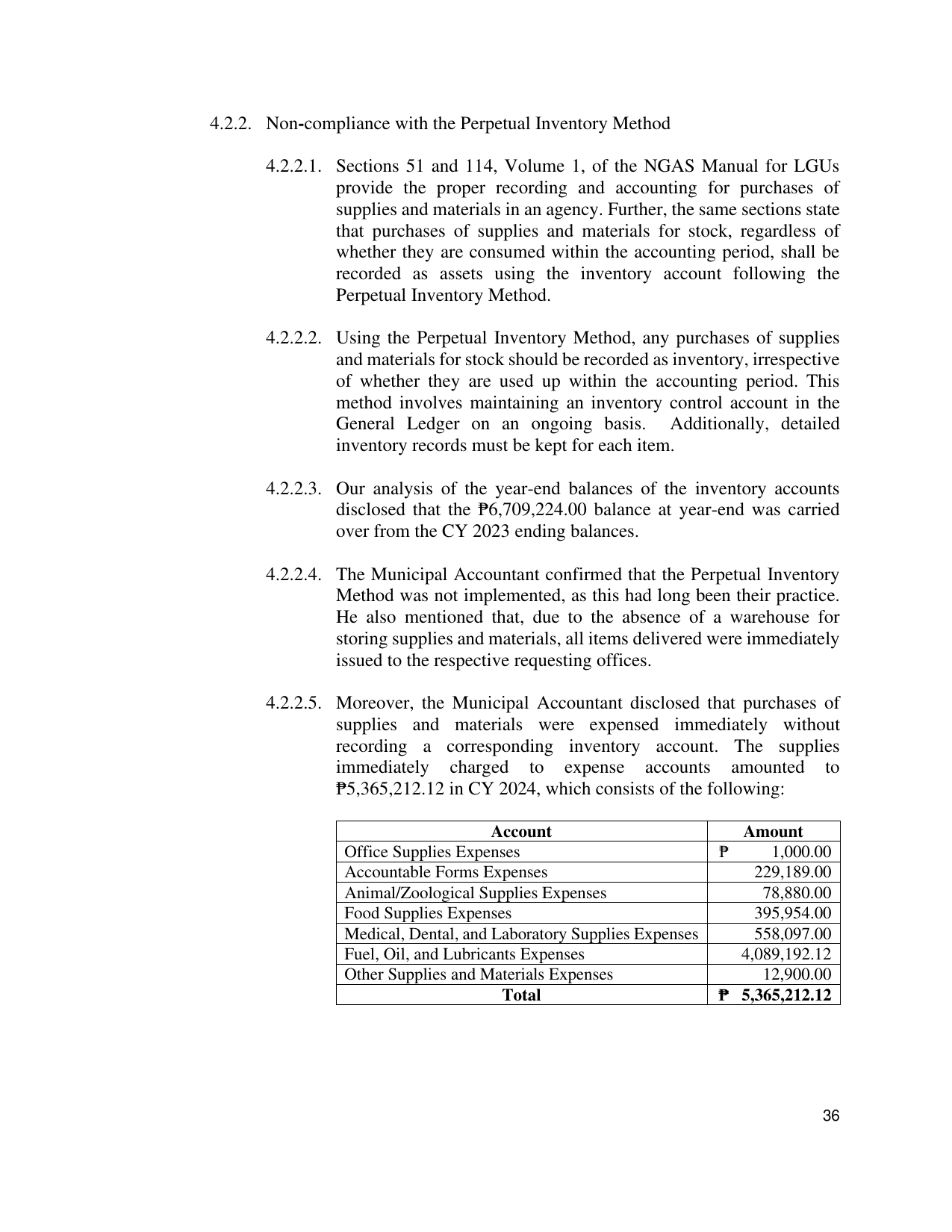

4.2.2.5. Moreover, the Municipal Accountant disclosed that purchases of

supplies and materials were expensed immediately without

recording a corresponding inventory account. The supplies

immediately charged to expense accounts amounted to

₱5,365,212.12 in CY 2024, which consists of the following:

Account Amount

Office Supplies Expenses ₱ 1,000.00

Accountable Forms Expenses 229,189.00

Animal/Zoological Supplies Expenses 78,880.00

Food Supplies Expenses 395,954.00

Medical, Dental, and Laboratory Supplies Expenses 558,097.00

Fuel, Oil, and Lubricants Expenses 4,089,192.12

Other Supplies and Materials Expenses 12,900.00

Total ₱ 5,365,212.12

36