Inventory Accounts

4. The existence, validity, and correctness of the Inventory accounts totaling

₱6,709,224.00 as of December 31, 2024, have not been established due to (a) non-

conduct of the year-end physical count, (b) non-compliance with the Perpetual

Inventory Method, and (c) non-maintenance of supplies ledger cards and stock cards

by the Offices of the Municipal Accountant and Municipal Treasurer, respectively,

which goes against the provisions set forth in the NGAS Manual for LGUs, Volume

1, thereby, affecting the fairness of the presentation of these accounts in the financial

statements.

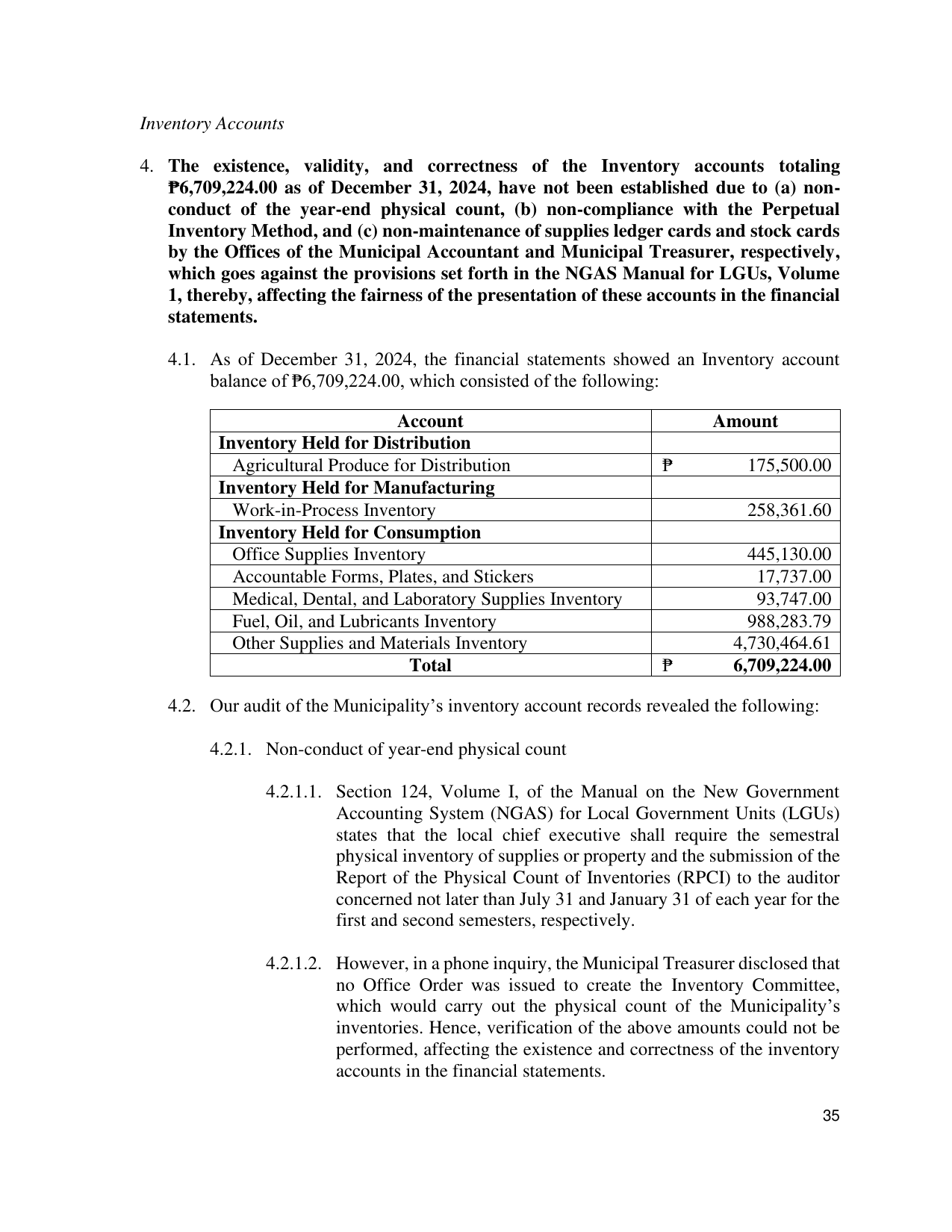

4.1. As of December 31, 2024, the financial statements showed an Inventory account

balance of ₱6,709,224.00, which consisted of the following:

Account Amount

Inventory Held for Distribution

Agricultural Produce for Distribution ₱ 175,500.00

Inventory Held for Manufacturing

Work-in-Process Inventory 258,361.60

Inventory Held for Consumption

Office Supplies Inventory 445,130.00

Accountable Forms, Plates, and Stickers 17,737.00

Medical, Dental, and Laboratory Supplies Inventory 93,747.00

Fuel, Oil, and Lubricants Inventory 988,283.79

Other Supplies and Materials Inventory 4,730,464.61

Total ₱ 6,709,224.00

4.2. Our audit of the Municipality’s inventory account records revealed the following:

4.2.1. Non-conduct of year-end physical count

4.2.1.1. Section 124, Volume I, of the Manual on the New Government

Accounting System (NGAS) for Local Government Units (LGUs)

states that the local chief executive shall require the semestral

physical inventory of supplies or property and the submission of the

Report of the Physical Count of Inventories (RPCI) to the auditor

concerned not later than July 31 and January 31 of each year for the

first and second semesters, respectively.

4.2.1.2. However, in a phone inquiry, the Municipal Treasurer disclosed that

no Office Order was issued to create the Inventory Committee,

which would carry out the physical count of the Municipality’s

inventories. Hence, verification of the above amounts could not be

performed, affecting the existence and correctness of the inventory

accounts in the financial statements.

35