2.3.1.3. In a phone inquiry, the Municipal Accountant explained that the

discrepancy has been an ongoing issue since he assumed office. He

added that due to a lack of manpower and his current workload, he

was not able to prioritize the reconciliation of the Lapsing Schedule

and the financial statements.

2.3.1.4. Additionally, the Audit Team requested the General and Subsidiary

Ledgers for the above items; however, as of this date, the Municipal

Accountant has not yet submitted the requested documents.

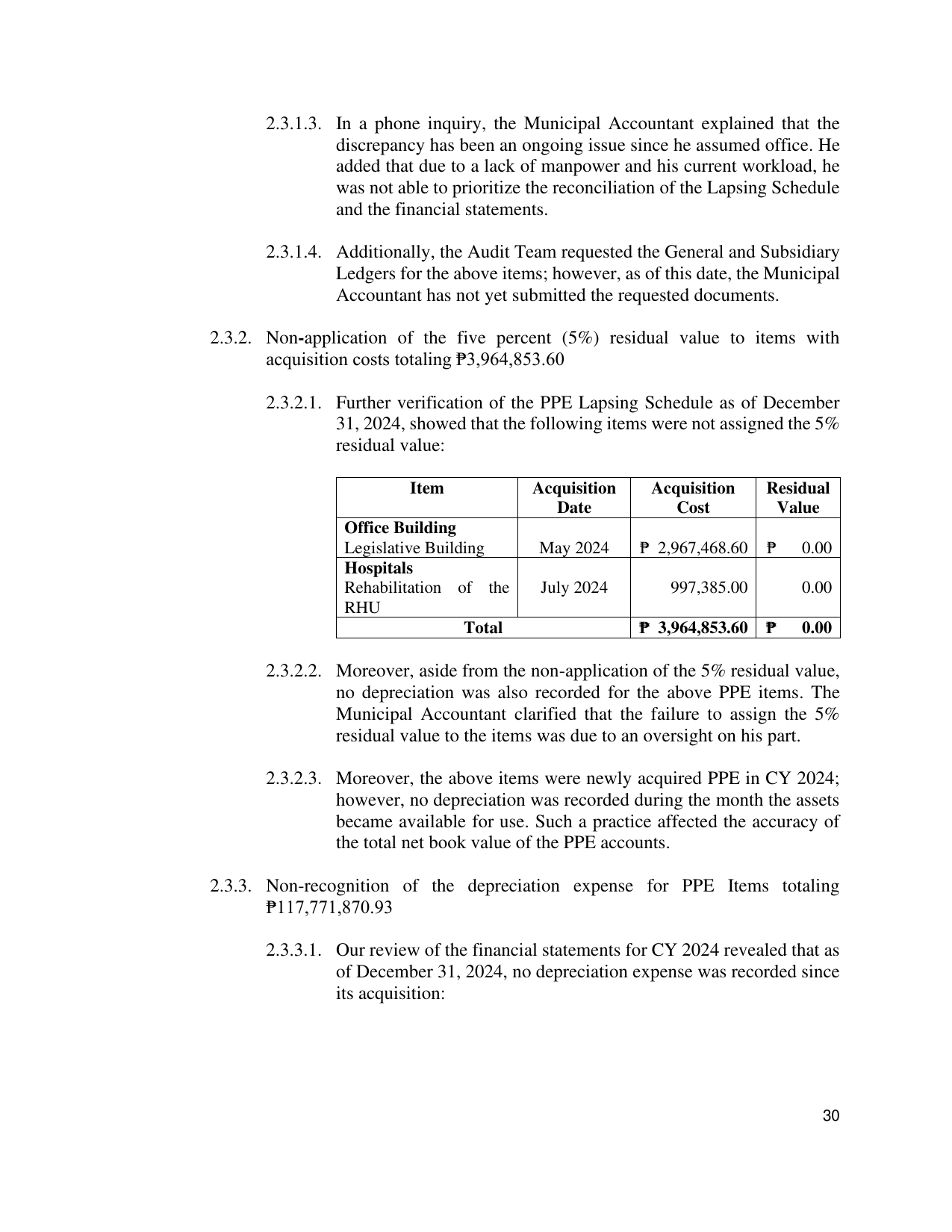

2.3.2. Non-application of the five percent (5%) residual value to items with

acquisition costs totaling ₱3,964,853.60

2.3.2.1. Further verification of the PPE Lapsing Schedule as of December

31, 2024, showed that the following items were not assigned the 5%

residual value:

Item Acquisition Acquisition Residual

Date Cost Value

Office Building

Legislative Building May 2024 ₱ 2,967,468.60 ₱ 0.00

Hospitals

Rehabilitation of the July 2024 997,385.00 0.00

RHU

Total ₱ 3,964,853.60 ₱ 0.00

2.3.2.2. Moreover, aside from the non-application of the 5% residual value,

no depreciation was also recorded for the above PPE items. The

Municipal Accountant clarified that the failure to assign the 5%

residual value to the items was due to an oversight on his part.

2.3.2.3. Moreover, the above items were newly acquired PPE in CY 2024;

however, no depreciation was recorded during the month the assets

became available for use. Such a practice affected the accuracy of

the total net book value of the PPE accounts.

2.3.3. Non-recognition of the depreciation expense for PPE Items totaling

₱117,771,870.93

2.3.3.1. Our review of the financial statements for CY 2024 revealed that as

of December 31, 2024, no depreciation expense was recorded since

its acquisition:

30