PAG 6 A residual value equivalent to at least five percent (5%) of the cost

shall be adopted unless a more appropriate percentage is determined

by the agency based on their operation.”

2.3. The audit of depreciable PPE accounts with a total recorded cost of ₱338,950,421.93

and a total accumulated depreciation of ₱43,885,945.58 as of December 31, 2024,

showed that the reported net book value of the PPE account of ₱295,064,476.35 for

the same period could not be relied upon due to the following:

2.3.1. Discrepancy between the PPE Lapsing Schedule and the Financial Statements

amounting to ₱170,982,037.93

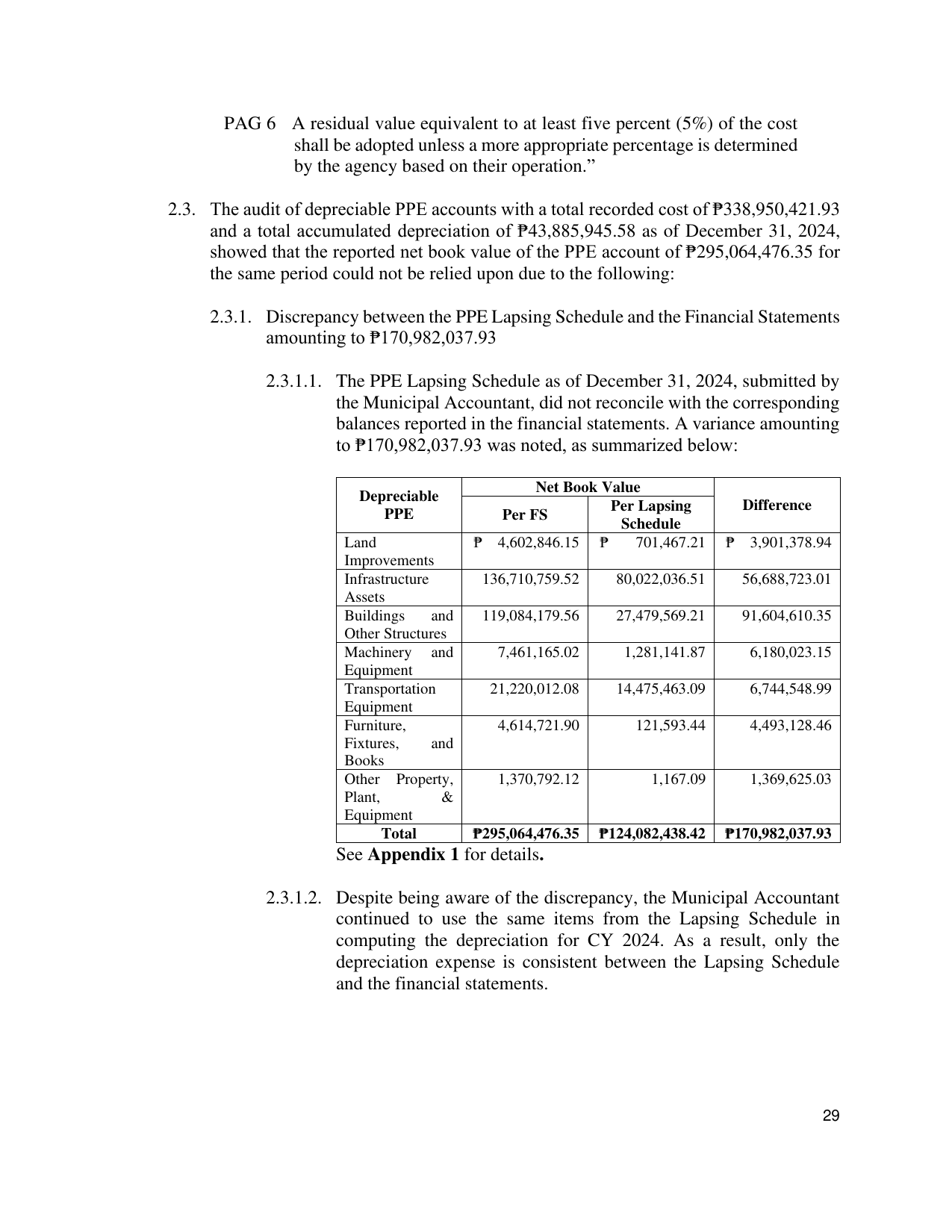

2.3.1.1. The PPE Lapsing Schedule as of December 31, 2024, submitted by

the Municipal Accountant, did not reconcile with the corresponding

balances reported in the financial statements. A variance amounting

to ₱170,982,037.93 was noted, as summarized below:

Net Book Value

Depreciable

Per Lapsing Difference

PPE Per FS

Schedule

Land ₱ 4,602,846.15 ₱ 701,467.21 ₱ 3,901,378.94

Improvements

Infrastructure 136,710,759.52 80,022,036.51 56,688,723.01

Assets

Buildings and 119,084,179.56 27,479,569.21 91,604,610.35

Other Structures

Machinery and 7,461,165.02 1,281,141.87 6,180,023.15

Equipment

Transportation 21,220,012.08 14,475,463.09 6,744,548.99

Equipment

Furniture, 4,614,721.90 121,593.44 4,493,128.46

Fixtures, and

Books

Other Property, 1,370,792.12 1,167.09 1,369,625.03

Plant, &

Equipment

Total ₱295,064,476.35 ₱124,082,438.42 ₱170,982,037.93

See Appendix 1 for details.

2.3.1.2. Despite being aware of the discrepancy, the Municipal Accountant

continued to use the same items from the Lapsing Schedule in

computing the depreciation for CY 2024. As a result, only the

depreciation expense is consistent between the Lapsing Schedule

and the financial statements.

29