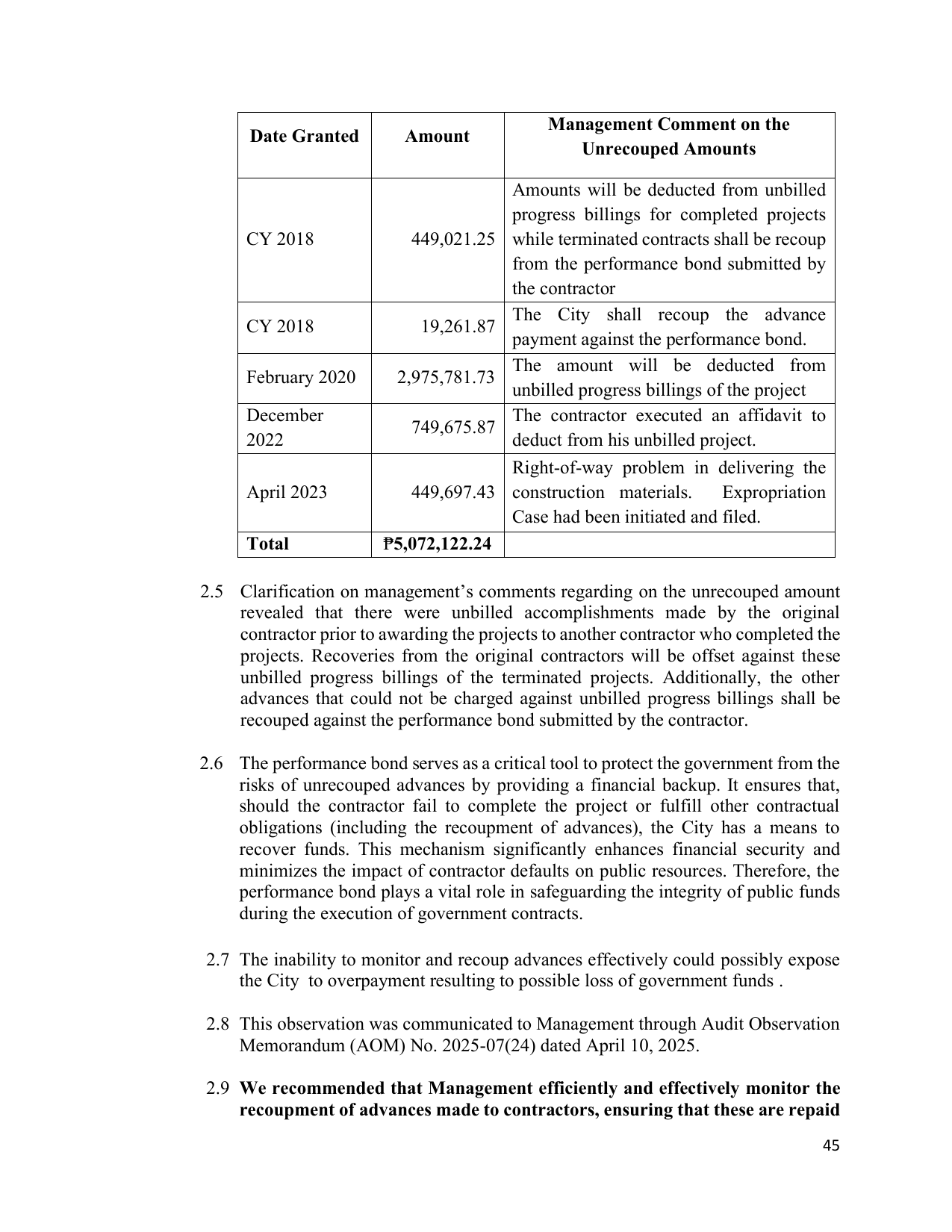

Management Comment on the

Date Granted Amount

Unrecouped Amounts

Amounts will be deducted from unbilled

progress billings for completed projects

CY 2018 449,021.25 while terminated contracts shall be recoup

from the performance bond submitted by

the contractor

The City shall recoup the advance

CY 2018 19,261.87

payment against the performance bond.

The amount will be deducted from

February 2020 2,975,781.73

unbilled progress billings of the project

December The contractor executed an affidavit to

749,675.87

2022 deduct from his unbilled project.

Right-of-way problem in delivering the

April 2023 449,697.43 construction materials. Expropriation

Case had been initiated and filed.

Total ₱5,072,122.24

2.5 Clarification on management’s comments regarding on the unrecouped amount

revealed that there were unbilled accomplishments made by the original

contractor prior to awarding the projects to another contractor who completed the

projects. Recoveries from the original contractors will be offset against these

unbilled progress billings of the terminated projects. Additionally, the other

advances that could not be charged against unbilled progress billings shall be

recouped against the performance bond submitted by the contractor.

2.6 The performance bond serves as a critical tool to protect the government from the

risks of unrecouped advances by providing a financial backup. It ensures that,

should the contractor fail to complete the project or fulfill other contractual

obligations (including the recoupment of advances), the City has a means to

recover funds. This mechanism significantly enhances financial security and

minimizes the impact of contractor defaults on public resources. Therefore, the

performance bond plays a vital role in safeguarding the integrity of public funds

during the execution of government contracts.

2.7 The inability to monitor and recoup advances effectively could possibly expose

the City to overpayment resulting to possible loss of government funds .

2.8 This observation was communicated to Management through Audit Observation

Memorandum (AOM) No. 2025-07(24) dated April 10, 2025.

2.9 We recommended that Management efficiently and effectively monitor the

recoupment of advances made to contractors, ensuring that these are repaid

45