5.5 Based on the age of the items in the CIP account, as seen in the previous table,

projects remained classified as In Progress for more than 10 years.

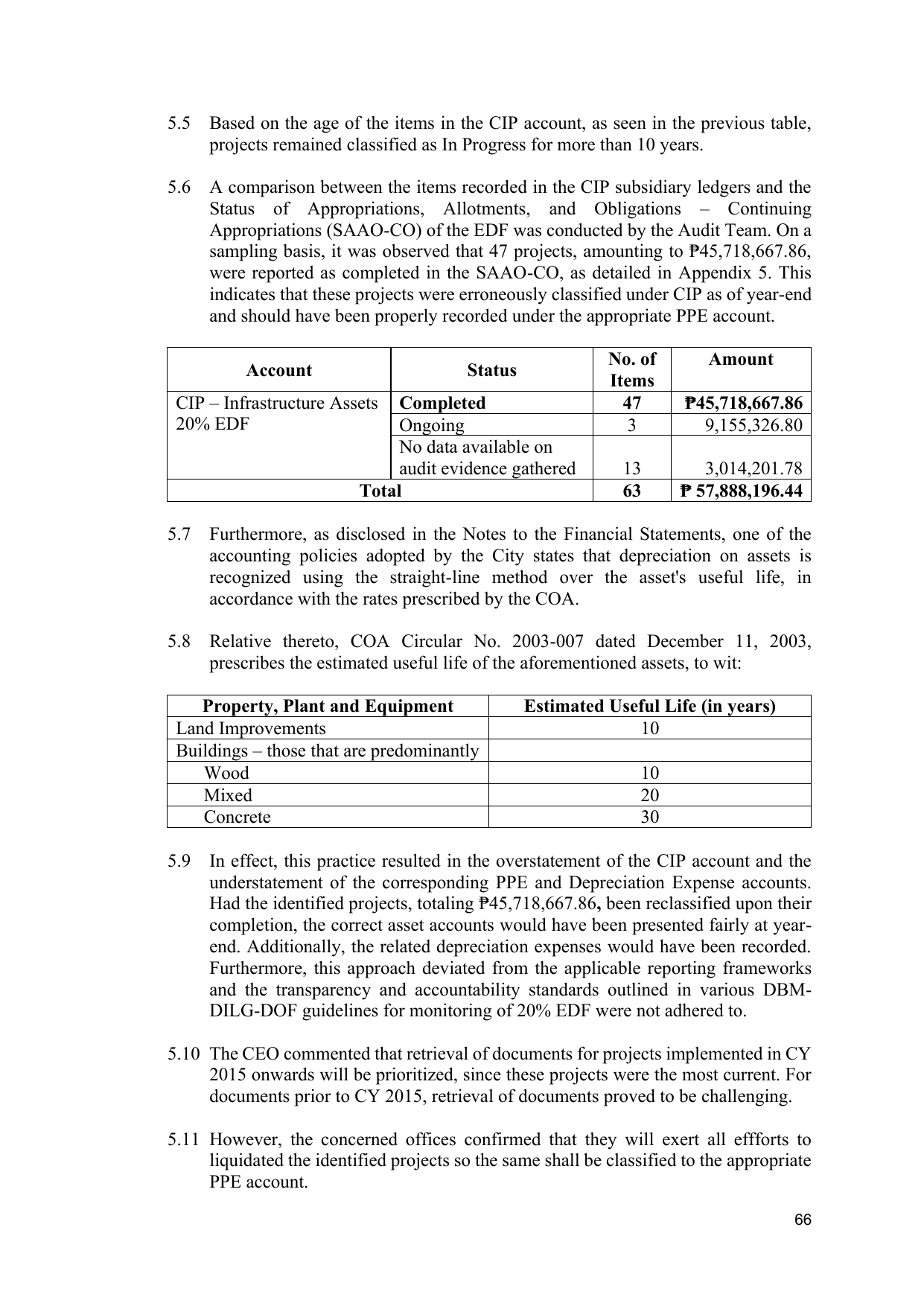

5.6 A comparison between the items recorded in the CIP subsidiary ledgers and the

Status of Appropriations, Allotments, and Obligations – Continuing

Appropriations (SAAO-CO) of the EDF was conducted by the Audit Team. On a

sampling basis, it was observed that 47 projects, amounting to ₱45,718,667.86,

were reported as completed in the SAAO-CO, as detailed in Appendix 5. This

indicates that these projects were erroneously classified under CIP as of year-end

and should have been properly recorded under the appropriate PPE account.

No. of Amount

Account Status

Items

CIP – Infrastructure Assets Completed 47 ₱45,718,667.86

20% EDF Ongoing 3 9,155,326.80

No data available on

audit evidence gathered 13 3,014,201.78

Total 63 ₱ 57,888,196.44

5.7 Furthermore, as disclosed in the Notes to the Financial Statements, one of the

accounting policies adopted by the City states that depreciation on assets is

recognized using the straight-line method over the asset's useful life, in

accordance with the rates prescribed by the COA.

5.8 Relative thereto, COA Circular No. 2003-007 dated December 11, 2003,

prescribes the estimated useful life of the aforementioned assets, to wit:

Property, Plant and Equipment Estimated Useful Life (in years)

Land Improvements 10

Buildings – those that are predominantly

Wood 10

Mixed 20

Concrete 30

5.9 In effect, this practice resulted in the overstatement of the CIP account and the

understatement of the corresponding PPE and Depreciation Expense accounts.

Had the identified projects, totaling ₱45,718,667.86, been reclassified upon their

completion, the correct asset accounts would have been presented fairly at year-

end. Additionally, the related depreciation expenses would have been recorded.

Furthermore, this approach deviated from the applicable reporting frameworks

and the transparency and accountability standards outlined in various DBM-

DILG-DOF guidelines for monitoring of 20% EDF were not adhered to.

5.10 The CEO commented that retrieval of documents for projects implemented in CY

2015 onwards will be prioritized, since these projects were the most current. For

documents prior to CY 2015, retrieval of documents proved to be challenging.

5.11 However, the concerned offices confirmed that they will exert all effforts to

liquidated the identified projects so the same shall be classified to the appropriate

PPE account.

66