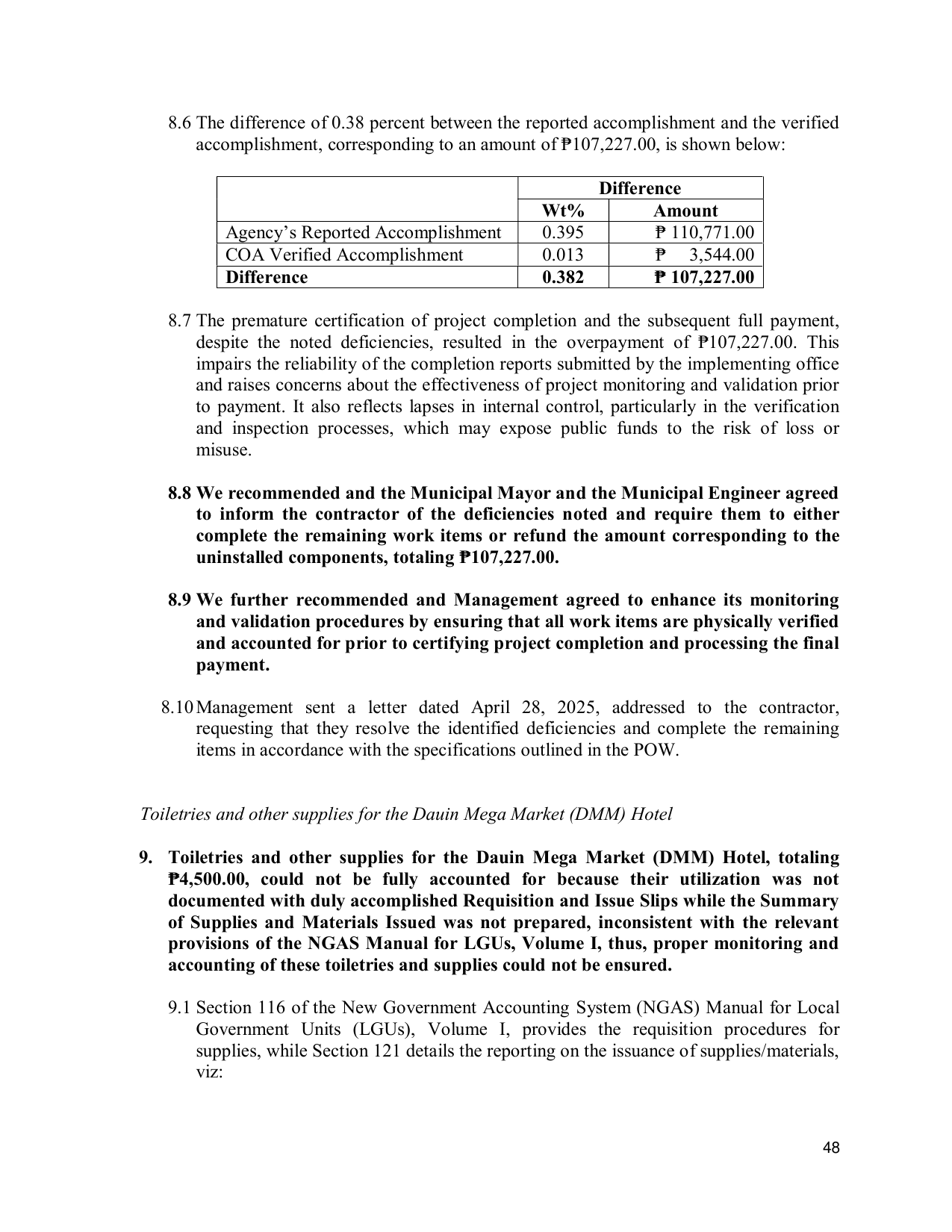

8.6 The difference of 0.38 percent between the reported accomplishment and the verified

accomplishment, corresponding to an amount of ₱107,227.00, is shown below:

Difference

Wt% Amount

Agency’s Reported Accomplishment 0.395 ₱ 110,771.00

COA Verified Accomplishment 0.013 ₱ 3,544.00

Difference 0.382 ₱ 107,227.00

8.7 The premature certification of project completion and the subsequent full payment,

despite the noted deficiencies, resulted in the overpayment of ₱107,227.00. This

impairs the reliability of the completion reports submitted by the implementing office

and raises concerns about the effectiveness of project monitoring and validation prior

to payment. It also reflects lapses in internal control, particularly in the verification

and inspection processes, which may expose public funds to the risk of loss or

misuse.

8.8 We recommended and the Municipal Mayor and the Municipal Engineer agreed

to inform the contractor of the deficiencies noted and require them to either

complete the remaining work items or refund the amount corresponding to the

uninstalled components, totaling ₱107,227.00.

8.9 We further recommended and Management agreed to enhance its monitoring

and validation procedures by ensuring that all work items are physically verified

and accounted for prior to certifying project completion and processing the final

payment.

8.10 Management sent a letter dated April 28, 2025, addressed to the contractor,

requesting that they resolve the identified deficiencies and complete the remaining

items in accordance with the specifications outlined in the POW.

Toiletries and other supplies for the Dauin Mega Market (DMM) Hotel

9. Toiletries and other supplies for the Dauin Mega Market (DMM) Hotel, totaling

₱4,500.00, could not be fully accounted for because their utilization was not

documented with duly accomplished Requisition and Issue Slips while the Summary

of Supplies and Materials Issued was not prepared, inconsistent with the relevant

provisions of the NGAS Manual for LGUs, Volume I, thus, proper monitoring and

accounting of these toiletries and supplies could not be ensured.

9.1 Section 116 of the New Government Accounting System (NGAS) Manual for Local

Government Units (LGUs), Volume I, provides the requisition procedures for

supplies, while Section 121 details the reporting on the issuance of supplies/materials,

viz:

48