Ref. Audit Observations Audit Recommendations Status of Implementation

governing the release of PDAF funds,

hence, their validity, legality and

propriety are in question.

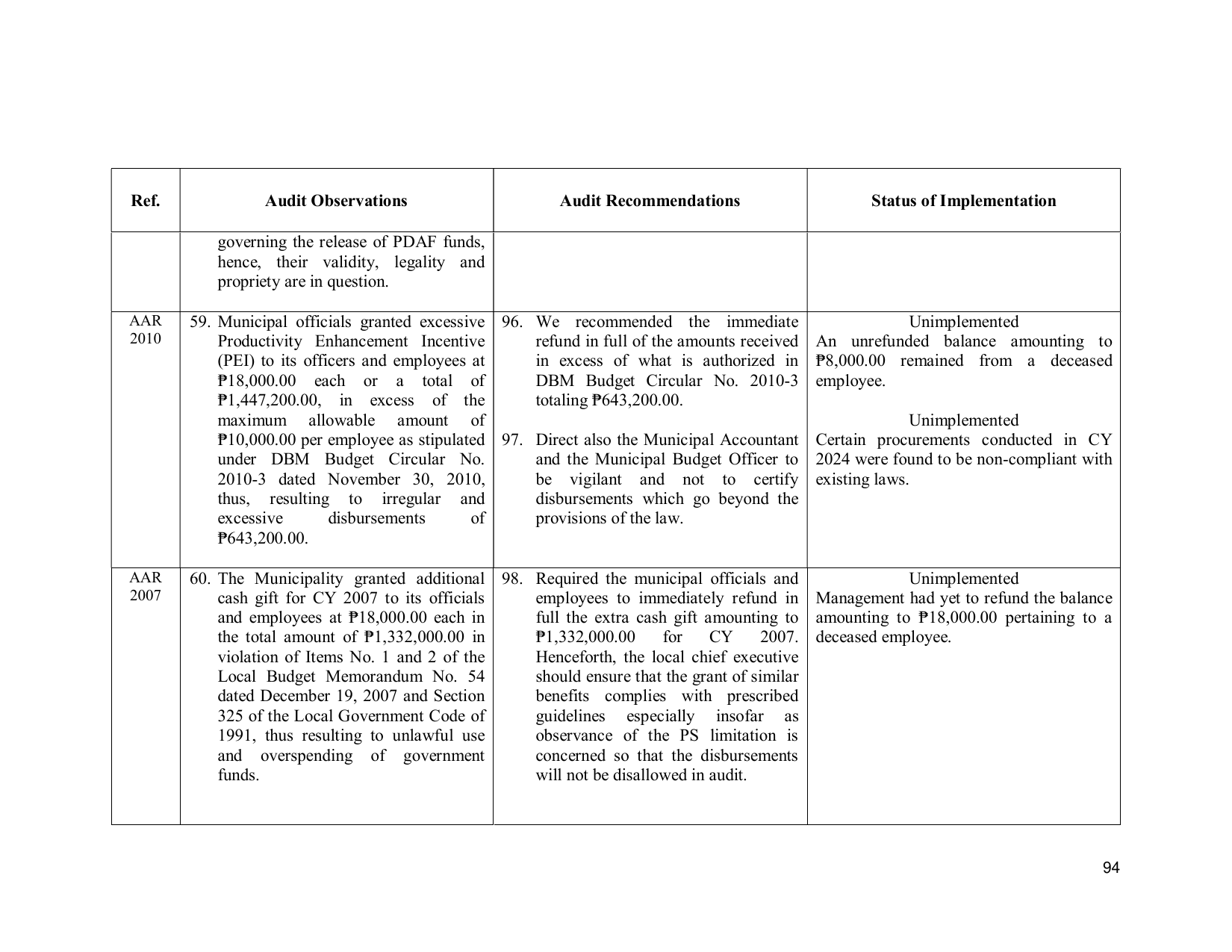

AAR 59. Municipal officials granted excessive 96. We recommended the immediate Unimplemented

2010 Productivity Enhancement Incentive refund in full of the amounts received An unrefunded balance amounting to

(PEI) to its officers and employees at in excess of what is authorized in ₱8,000.00 remained from a deceased

₱18,000.00 each or a total of DBM Budget Circular No. 2010-3 employee.

₱1,447,200.00, in excess of the totaling ₱643,200.00.

maximum allowable amount of Unimplemented

₱10,000.00 per employee as stipulated 97. Direct also the Municipal Accountant Certain procurements conducted in CY

under DBM Budget Circular No. and the Municipal Budget Officer to 2024 were found to be non-compliant with

2010-3 dated November 30, 2010, be vigilant and not to certify existing laws.

thus, resulting to irregular and disbursements which go beyond the

excessive disbursements of provisions of the law.

₱643,200.00.

AAR 60. The Municipality granted additional 98. Required the municipal officials and Unimplemented

2007 cash gift for CY 2007 to its officials employees to immediately refund in Management had yet to refund the balance

and employees at ₱18,000.00 each in full the extra cash gift amounting to amounting to ₱18,000.00 pertaining to a

the total amount of ₱1,332,000.00 in ₱1,332,000.00 for CY 2007. deceased employee.

violation of Items No. 1 and 2 of the Henceforth, the local chief executive

Local Budget Memorandum No. 54 should ensure that the grant of similar

dated December 19, 2007 and Section benefits complies with prescribed

325 of the Local Government Code of guidelines especially insofar as

1991, thus resulting to unlawful use observance of the PS limitation is

and overspending of government concerned so that the disbursements

funds. will not be disallowed in audit.

94