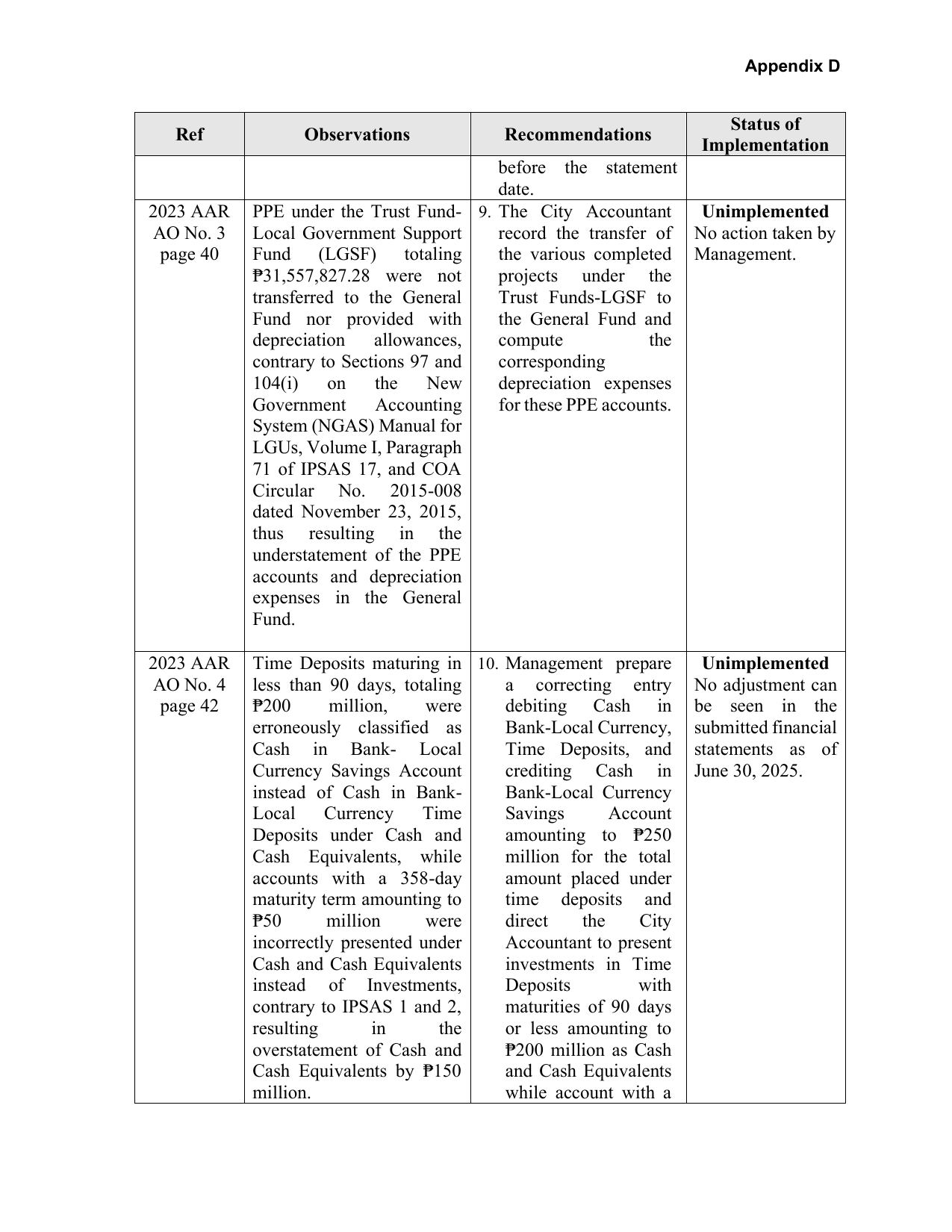

Appendix D

Status of

Ref Observations Recommendations

Implementation

before the statement

date.

2023 AAR PPE under the Trust Fund- 9. The City Accountant Unimplemented

AO No. 3 Local Government Support record the transfer of No action taken by

page 40 Fund (LGSF) totaling the various completed Management.

₱31,557,827.28 were not projects under the

transferred to the General Trust Funds-LGSF to

Fund nor provided with the General Fund and

depreciation allowances, compute the

contrary to Sections 97 and corresponding

104(i) on the New depreciation expenses

Government Accounting for these PPE accounts.

System (NGAS) Manual for

LGUs, Volume I, Paragraph

71 of IPSAS 17, and COA

Circular No. 2015-008

dated November 23, 2015,

thus resulting in the

understatement of the PPE

accounts and depreciation

expenses in the General

Fund.

2023 AAR Time Deposits maturing in 10. Management prepare Unimplemented

AO No. 4 less than 90 days, totaling a correcting entry No adjustment can

page 42 ₱200 million, were debiting Cash in be seen in the

erroneously classified as Bank-Local Currency, submitted financial

Cash in Bank- Local Time Deposits, and statements as of

Currency Savings Account crediting Cash in June 30, 2025.

instead of Cash in Bank- Bank-Local Currency

Local Currency Time Savings Account

Deposits under Cash and amounting to ₱250

Cash Equivalents, while million for the total

accounts with a 358-day amount placed under

maturity term amounting to time deposits and

₱50 million were direct the City

incorrectly presented under Accountant to present

Cash and Cash Equivalents investments in Time

instead of Investments, Deposits with

contrary to IPSAS 1 and 2, maturities of 90 days

resulting in the or less amounting to

overstatement of Cash and ₱200 million as Cash

Cash Equivalents by ₱150 and Cash Equivalents

million. while account with a