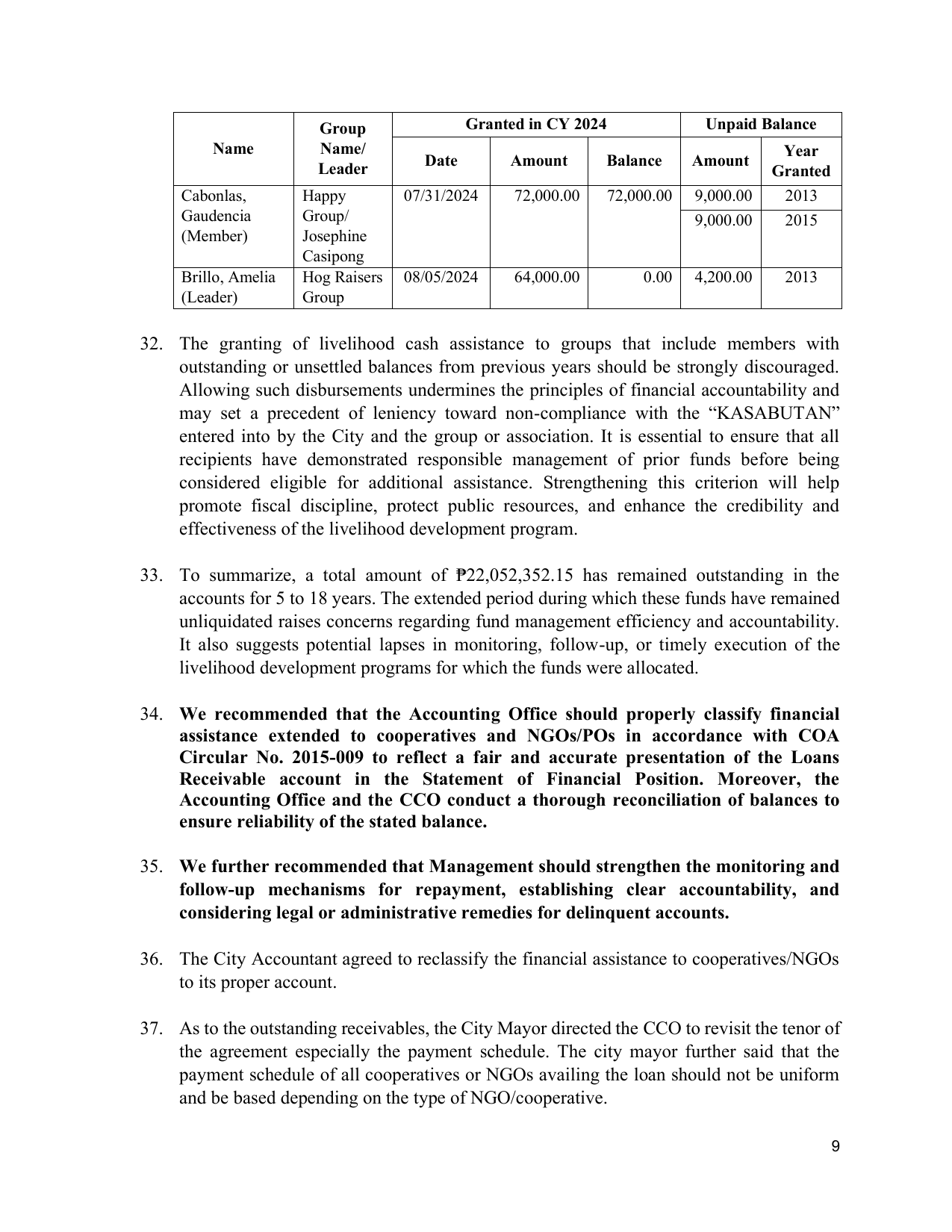

Group Granted in CY 2024 Unpaid Balance

Name Name/ Year

Leader Date Amount Balance Amount

Granted

Cabonlas, Happy 07/31/2024 72,000.00 72,000.00 9,000.00 2013

Gaudencia Group/ 9,000.00 2015

(Member) Josephine

Casipong

Brillo, Amelia Hog Raisers 08/05/2024 64,000.00 0.00 4,200.00 2013

(Leader) Group

32. The granting of livelihood cash assistance to groups that include members with

outstanding or unsettled balances from previous years should be strongly discouraged.

Allowing such disbursements undermines the principles of financial accountability and

may set a precedent of leniency toward non-compliance with the “KASABUTAN”

entered into by the City and the group or association. It is essential to ensure that all

recipients have demonstrated responsible management of prior funds before being

considered eligible for additional assistance. Strengthening this criterion will help

promote fiscal discipline, protect public resources, and enhance the credibility and

effectiveness of the livelihood development program.

33. To summarize, a total amount of ₱22,052,352.15 has remained outstanding in the

accounts for 5 to 18 years. The extended period during which these funds have remained

unliquidated raises concerns regarding fund management efficiency and accountability.

It also suggests potential lapses in monitoring, follow-up, or timely execution of the

livelihood development programs for which the funds were allocated.

34. We recommended that the Accounting Office should properly classify financial

assistance extended to cooperatives and NGOs/POs in accordance with COA

Circular No. 2015-009 to reflect a fair and accurate presentation of the Loans

Receivable account in the Statement of Financial Position. Moreover, the

Accounting Office and the CCO conduct a thorough reconciliation of balances to

ensure reliability of the stated balance.

35. We further recommended that Management should strengthen the monitoring and

follow-up mechanisms for repayment, establishing clear accountability, and

considering legal or administrative remedies for delinquent accounts.

36. The City Accountant agreed to reclassify the financial assistance to cooperatives/NGOs

to its proper account.

37. As to the outstanding receivables, the City Mayor directed the CCO to revisit the tenor of

the agreement especially the payment schedule. The city mayor further said that the

payment schedule of all cooperatives or NGOs availing the loan should not be uniform

and be based depending on the type of NGO/cooperative.

9