limitations, including the accessibility of the project location and availability

of equipment and materials, during the planning stage.

8.10 Management explained that the City Engineer, in coordination with the City

Planning Coordinator, has already evaluated and considered the feasibility of each

project. In fact, they have recommended projects for closure and reversion. They

have also addressed issues related to the implementation of the 20 percent DF and

other projects during the CY 2025 budget planning.

Funds that are not considered idle were placed into time deposit accounts – ₱366 million

9. The City Government placed a total of ₱385 million into four time deposit

accounts, of which ₱366 million represents the cash back-up of its current and

continuing capital outlay appropriations under the General Fund, leaving only

₱19 million as idle funds, contrary to Section 22 of COA Circular 92-382, thus

tying up funds necessary for the timely implementation of projects and activities.

9.1 Accounting and Auditing Rules and Regulations designed to implement the

provisions of the Local Government Code of 1991 under COA Circular No. 92-

382 dated July 3, 1992, provides specific guidelines regarding bank depository

accounts such as time deposit of funds. Section 22 thereof, defines “idle funds” as

those which are in excess of normal operating requirements, which means the level

of funds which an entity can freely invest in government securities and/or fixed

term deposits after considering provisions for coverage of regular and recurring

expenses. Unremitted national collections and funds set aside for payment of

obligations to government corporations/cooperatives shall not form part of idle

funds.

9.2 Moreover, the Department of Finance (DOF) clarified the definition of idle funds

in DOF Department Order No. 071-2018 dated December 13, 2018, stating that

“idle funds in excess of normal operating requirements” shall generally mean the

level of funds which the can be freely invested after considering provisions for

coverage of the following: regular and recurring expenses and local counterpart

commitments for capital expenditures with the current fiscal year. In the case of

LGUs, it also includes those excess funds, after considering unremitted national

collections and funds set aside for payments of obligations.

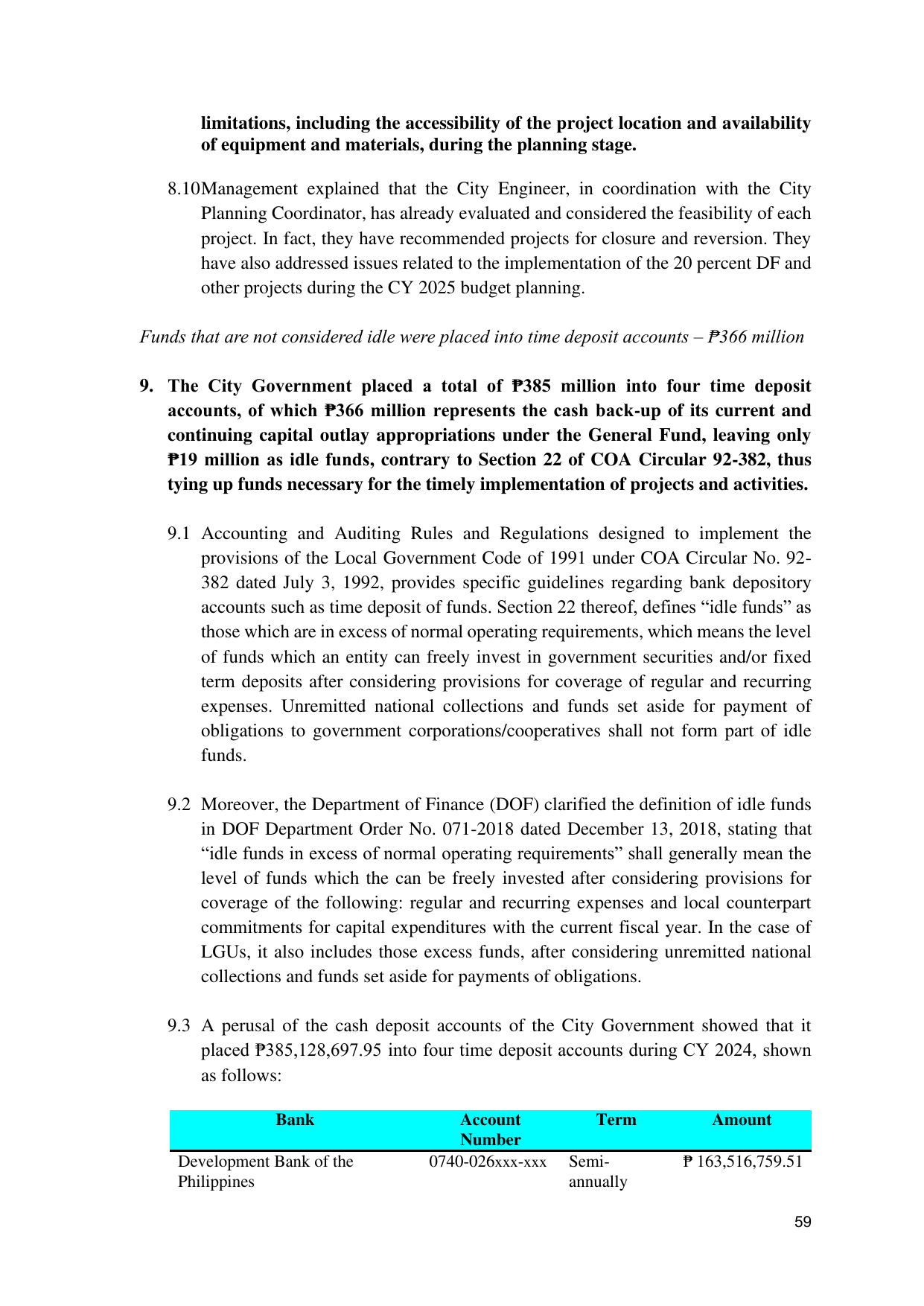

9.3 A perusal of the cash deposit accounts of the City Government showed that it

placed ₱385,128,697.95 into four time deposit accounts during CY 2024, shown

as follows:

Bank Account Term Amount

Number

Development Bank of the 0740-026xxx-xxx Semi- ₱ 163,516,759.51

Philippines annually

59