2.9 The City Accountant explained that this has been the practice of the City

Government. He confirmed that some inventories were expensed immediately,

especially those recorded in the Other Supplies and Materials expenses as these

were immediately issued to end-users, particularly meals and snacks. He assured

that appropriate RIS would be issued for these inventories to recognize them as

expenses.

Misclassification of accounts –₱15,807,069.14

3. Expenditures incurred for travel and gatherings such as consultative meetings

totaling ₱15,751,263.14 and cash advances relating to travel and intelligence

purposes amounting to ₱55,806.00, were misclassified to other expense and

receivable accounts, respectively, that do not reflect the true nature of their

purpose, inconsistent with COA Circular No. 2015-009, dated December 1, 2015,

thereby affecting the usefulness of financial information available for users of

financial statements, especially in the budgeting and decision-making process of

Management.

3.1 Paragraph 15 of the International Public Sector Accounting Standards (IPSAS) 1

clarifies that the objectives of a general-purpose financial statements are to provide

information about the financial position, financial performance, and cash flows of

an entity that is useful to users in making and evaluating decisions about the

allocation of resources. In the public sector, more specifically, the purpose of

financial reporting is to mainly provide information useful in decision making, and

to demonstrate accountability of the government agency.

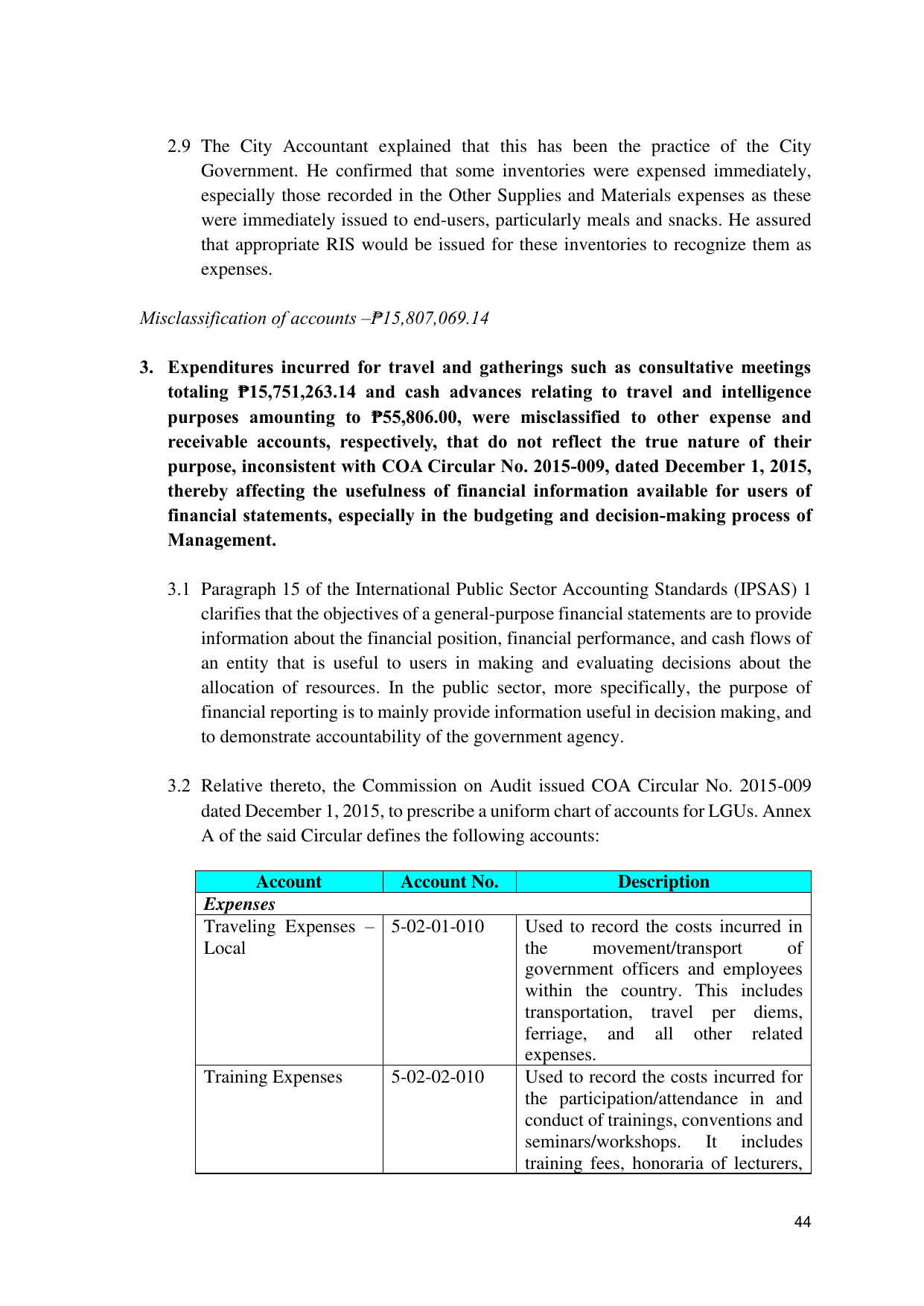

3.2 Relative thereto, the Commission on Audit issued COA Circular No. 2015-009

dated December 1, 2015, to prescribe a uniform chart of accounts for LGUs. Annex

A of the said Circular defines the following accounts:

Account Account No. Description

Expenses

Traveling Expenses – 5-02-01-010 Used to record the costs incurred in

Local the movement/transport of

government officers and employees

within the country. This includes

transportation, travel per diems,

ferriage, and all other related

expenses.

Training Expenses 5-02-02-010 Used to record the costs incurred for

the participation/attendance in and

conduct of trainings, conventions and

seminars/workshops. It includes

training fees, honoraria of lecturers,

44