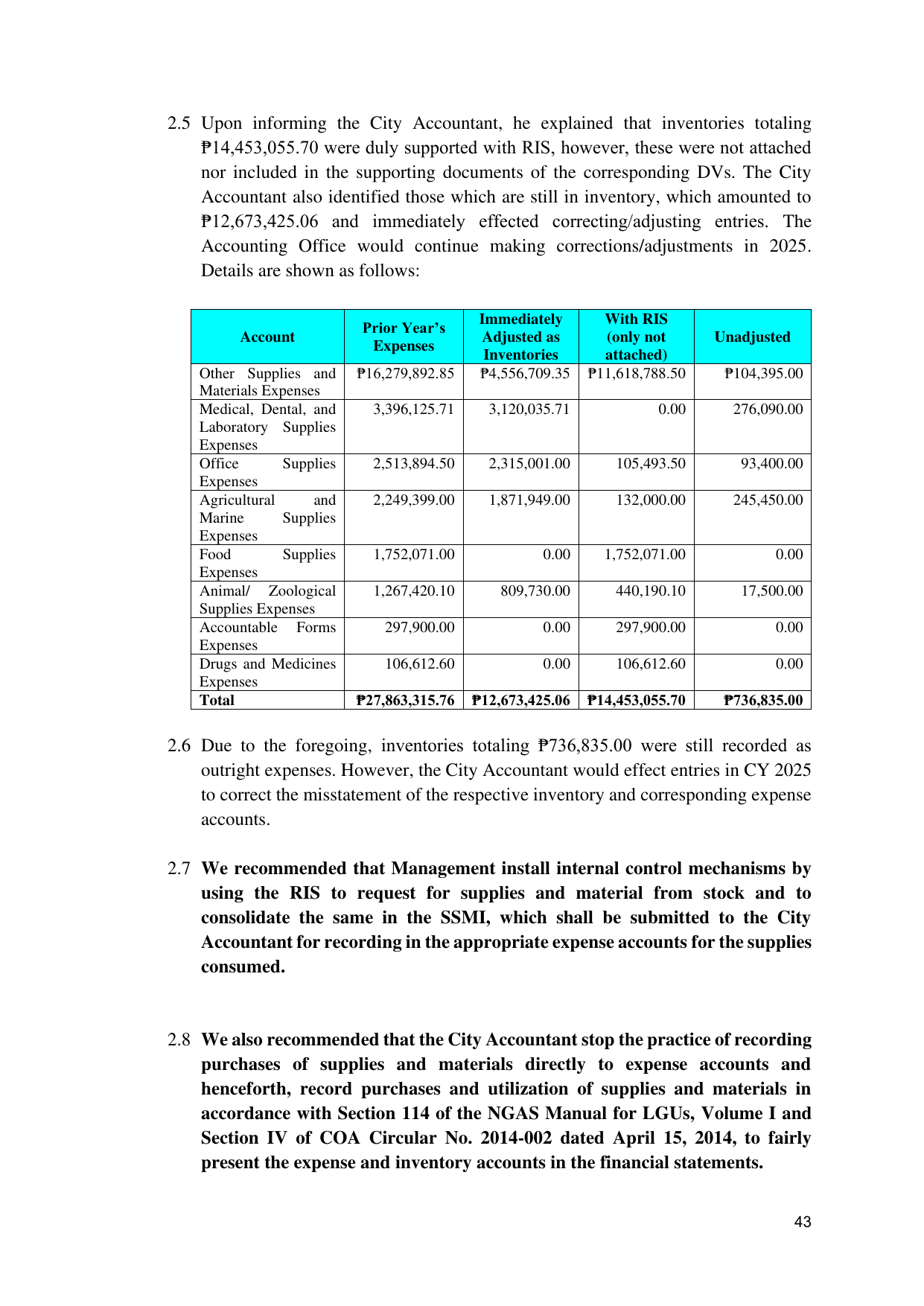

2.5 Upon informing the City Accountant, he explained that inventories totaling

₱14,453,055.70 were duly supported with RIS, however, these were not attached

nor included in the supporting documents of the corresponding DVs. The City

Accountant also identified those which are still in inventory, which amounted to

₱12,673,425.06 and immediately effected correcting/adjusting entries. The

Accounting Office would continue making corrections/adjustments in 2025.

Details are shown as follows:

Immediately With RIS

Prior Year’s

Account Adjusted as (only not Unadjusted

Expenses

Inventories attached)

Other Supplies and ₱16,279,892.85 ₱4,556,709.35 ₱11,618,788.50 ₱104,395.00

Materials Expenses

Medical, Dental, and 3,396,125.71 3,120,035.71 0.00 276,090.00

Laboratory Supplies

Expenses

Office Supplies 2,513,894.50 2,315,001.00 105,493.50 93,400.00

Expenses

Agricultural and 2,249,399.00 1,871,949.00 132,000.00 245,450.00

Marine Supplies

Expenses

Food Supplies 1,752,071.00 0.00 1,752,071.00 0.00

Expenses

Animal/ Zoological 1,267,420.10 809,730.00 440,190.10 17,500.00

Supplies Expenses

Accountable Forms 297,900.00 0.00 297,900.00 0.00

Expenses

Drugs and Medicines 106,612.60 0.00 106,612.60 0.00

Expenses

Total ₱27,863,315.76 ₱12,673,425.06 ₱14,453,055.70 ₱736,835.00

2.6 Due to the foregoing, inventories totaling ₱736,835.00 were still recorded as

outright expenses. However, the City Accountant would effect entries in CY 2025

to correct the misstatement of the respective inventory and corresponding expense

accounts.

2.7 We recommended that Management install internal control mechanisms by

using the RIS to request for supplies and material from stock and to

consolidate the same in the SSMI, which shall be submitted to the City

Accountant for recording in the appropriate expense accounts for the supplies

consumed.

2.8 We also recommended that the City Accountant stop the practice of recording

purchases of supplies and materials directly to expense accounts and

henceforth, record purchases and utilization of supplies and materials in

accordance with Section 114 of the NGAS Manual for LGUs, Volume I and

Section IV of COA Circular No. 2014-002 dated April 15, 2014, to fairly

present the expense and inventory accounts in the financial statements.

43