Inventories were recognized as expense upon receipt - ₱14,179,441.45

5. Purchases of inventories totaling ₱14,179,441.45 were recognized as expense

instead of inventory upon receipt contrary to Section 114 of the New Government

Accounting System (NGAS) Manual for Local Government Units (LGUs), Volume

I, thus, eliminating the required accounting of the receipt and utilization

established through the use of Requisitions and Issue Slips (RIS) and Summary of

Supplies and Materials Issued (SSMI), which could result in the misstatement of

inventory and expense accounts at the end of the year.

5.1 Section 114 of the NGAS Manual for LGUs, Volume I, provides that,

5.1.1 “Purchases of supplies and materials for stock, regardless of whether or not

they are consumed within the accounting period, shall be recorded as

inventory following the perpetual inventory method. Under the perpetual

inventory method, an inventory account is maintained in the General Ledger

on a current basis. In addition, detailed inventory records are maintained for

each inventory item. Regular purchases shall be coursed thru the inventory

account and issuances thereof shall be recorded as they take place, except

those purchased out of the petty cash fund which shall be for immediate use

and for stock in which case shall be charged immediately to the appropriate

expense accounts. x x x.” [Underscoring supplied]

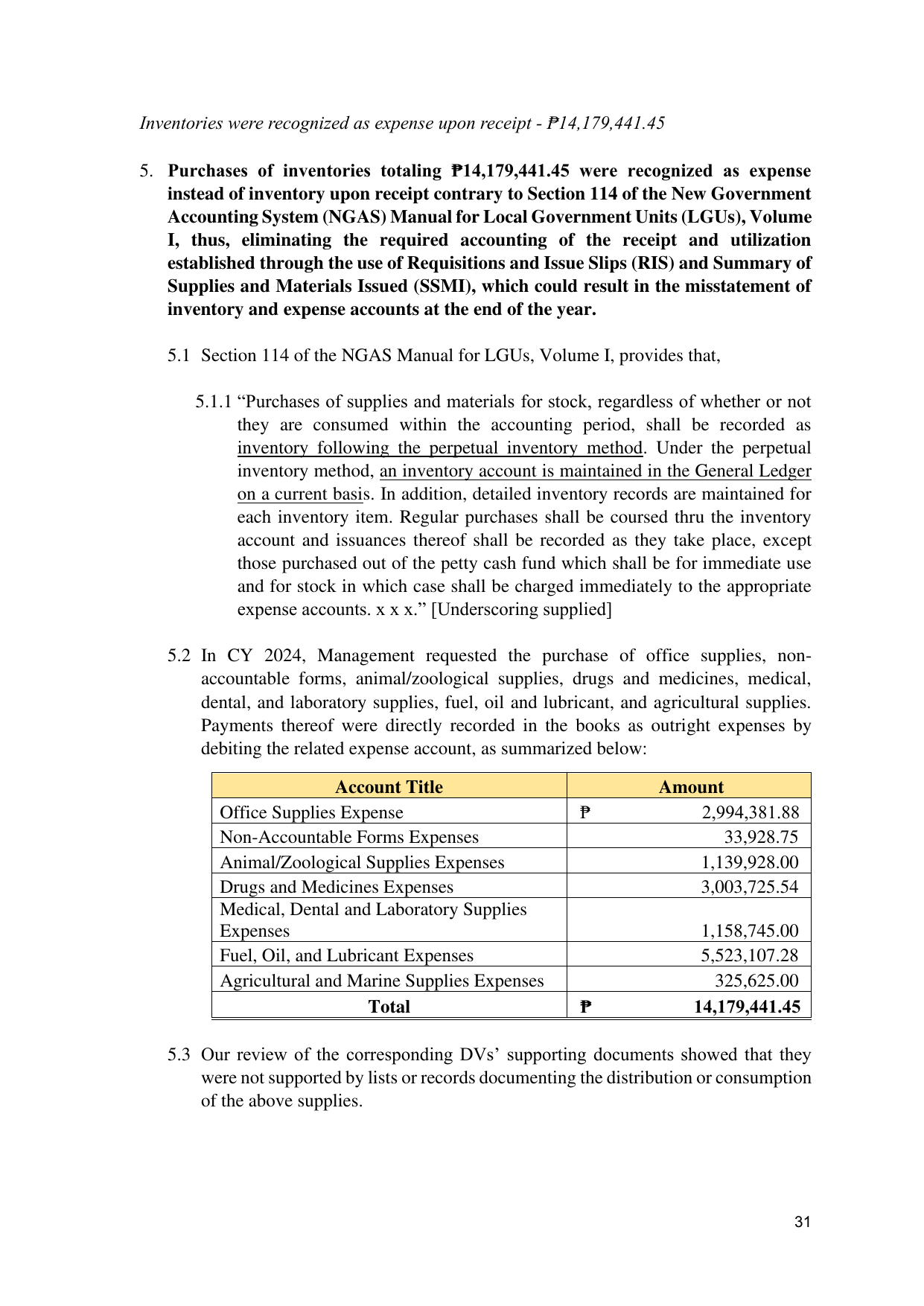

5.2 In CY 2024, Management requested the purchase of office supplies, non-

accountable forms, animal/zoological supplies, drugs and medicines, medical,

dental, and laboratory supplies, fuel, oil and lubricant, and agricultural supplies.

Payments thereof were directly recorded in the books as outright expenses by

debiting the related expense account, as summarized below:

Account Title Amount

Office Supplies Expense ₱ 2,994,381.88

Non-Accountable Forms Expenses 33,928.75

Animal/Zoological Supplies Expenses 1,139,928.00

Drugs and Medicines Expenses 3,003,725.54

Medical, Dental and Laboratory Supplies

Expenses 1,158,745.00

Fuel, Oil, and Lubricant Expenses 5,523,107.28

Agricultural and Marine Supplies Expenses 325,625.00

Total ₱ 14,179,441.45

5.3 Our review of the corresponding DVs’ supporting documents showed that they

were not supported by lists or records documenting the distribution or consumption

of the above supplies.

31