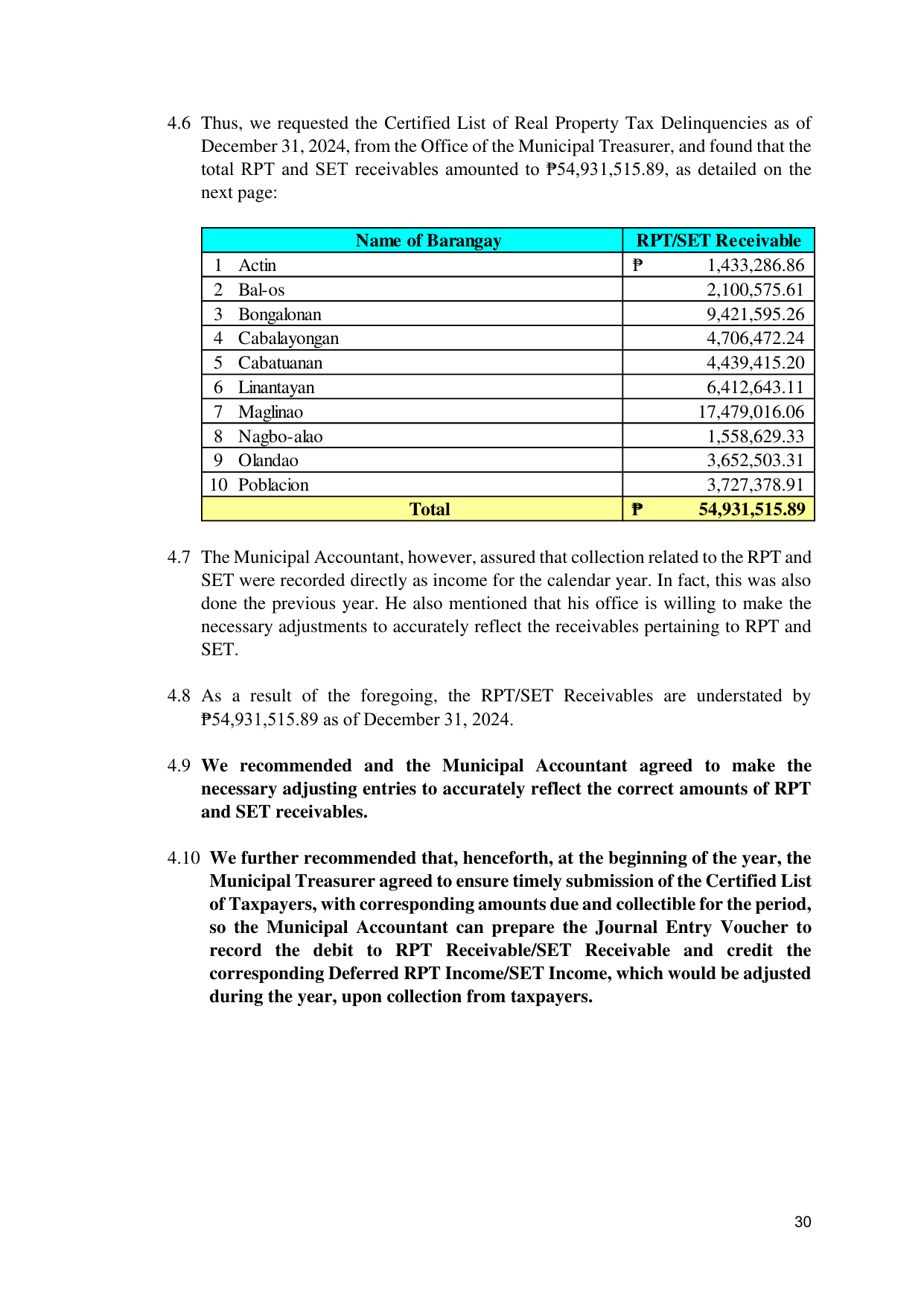

4.6 Thus, we requested the Certified List of Real Property Tax Delinquencies as of

December 31, 2024, from the Office of the Municipal Treasurer, and found that the

total RPT and SET receivables amounted to ₱54,931,515.89, as detailed on the

next page:

Name of Barangay RPT/SET Receivable

1 Actin ₱ 1,433,286.86

2 Bal-os 2,100,575.61

3 Bongalonan 9,421,595.26

4 Cabalayongan 4,706,472.24

5 Cabatuanan 4,439,415.20

6 Linantayan 6,412,643.11

7 Maglinao 17,479,016.06

8 Nagbo-alao 1,558,629.33

9 Olandao 3,652,503.31

10 Poblacion 3,727,378.91

Total ₱ 54,931,515.89

4.7 The Municipal Accountant, however, assured that collection related to the RPT and

SET were recorded directly as income for the calendar year. In fact, this was also

done the previous year. He also mentioned that his office is willing to make the

necessary adjustments to accurately reflect the receivables pertaining to RPT and

SET.

4.8 As a result of the foregoing, the RPT/SET Receivables are understated by

₱54,931,515.89 as of December 31, 2024.

4.9 We recommended and the Municipal Accountant agreed to make the

necessary adjusting entries to accurately reflect the correct amounts of RPT

and SET receivables.

4.10 We further recommended that, henceforth, at the beginning of the year, the

Municipal Treasurer agreed to ensure timely submission of the Certified List

of Taxpayers, with corresponding amounts due and collectible for the period,

so the Municipal Accountant can prepare the Journal Entry Voucher to

record the debit to RPT Receivable/SET Receivable and credit the

corresponding Deferred RPT Income/SET Income, which would be adjusted

during the year, upon collection from taxpayers.

30