Circular No. 2015-008, dated November 23, 2015 provides that “After recognition,

road networks shall be carried at its cost less any accumulated depreciation and

any accumulated impairment losses.”

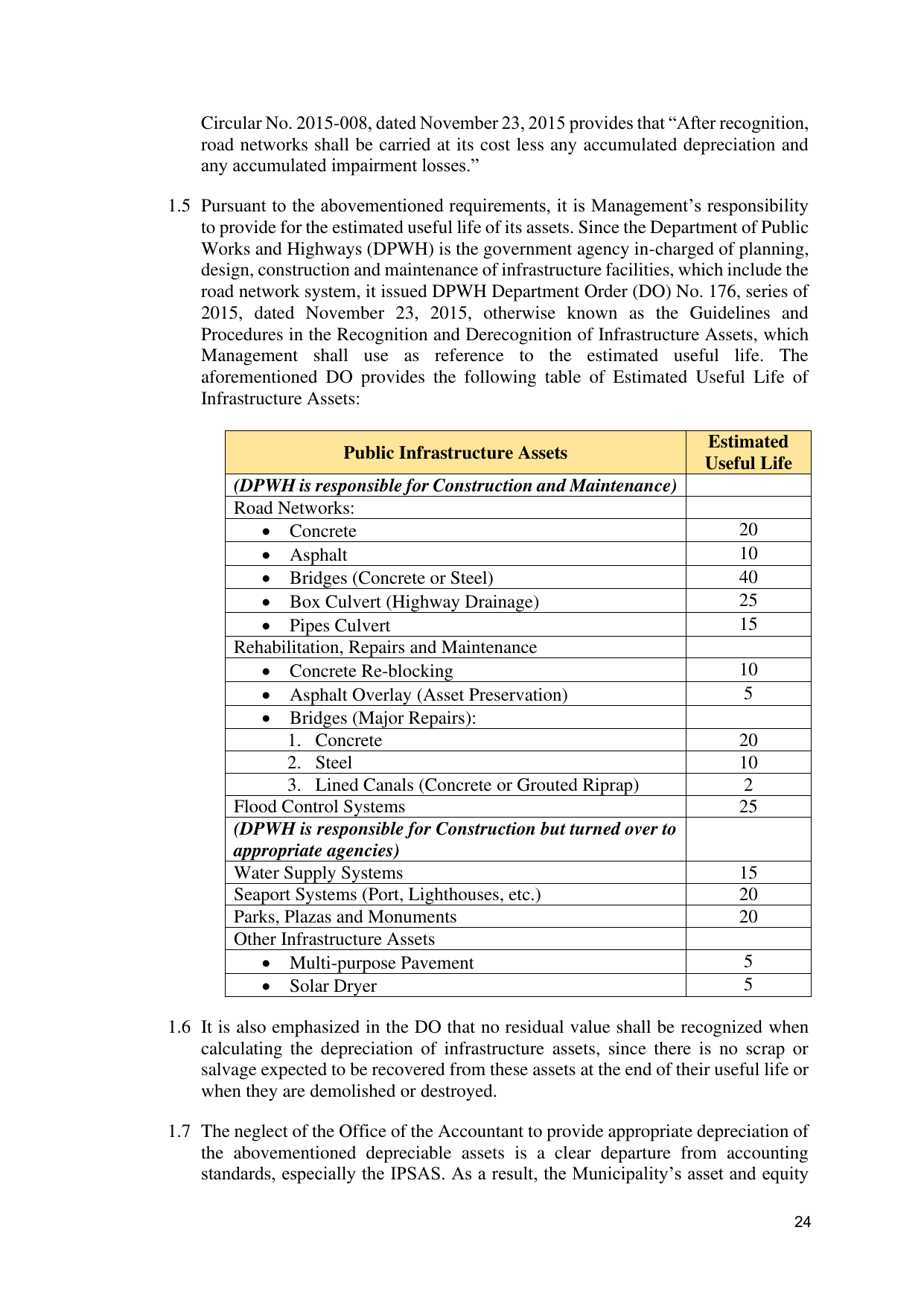

1.5 Pursuant to the abovementioned requirements, it is Management’s responsibility

to provide for the estimated useful life of its assets. Since the Department of Public

Works and Highways (DPWH) is the government agency in-charged of planning,

design, construction and maintenance of infrastructure facilities, which include the

road network system, it issued DPWH Department Order (DO) No. 176, series of

2015, dated November 23, 2015, otherwise known as the Guidelines and

Procedures in the Recognition and Derecognition of Infrastructure Assets, which

Management shall use as reference to the estimated useful life. The

aforementioned DO provides the following table of Estimated Useful Life of

Infrastructure Assets:

Estimated

Public Infrastructure Assets

Useful Life

(DPWH is responsible for Construction and Maintenance)

Road Networks:

• Concrete 20

• Asphalt 10

• Bridges (Concrete or Steel) 40

• Box Culvert (Highway Drainage) 25

• Pipes Culvert 15

Rehabilitation, Repairs and Maintenance

• Concrete Re-blocking 10

• Asphalt Overlay (Asset Preservation) 5

• Bridges (Major Repairs):

1. Concrete 20

2. Steel 10

3. Lined Canals (Concrete or Grouted Riprap) 2

Flood Control Systems 25

(DPWH is responsible for Construction but turned over to

appropriate agencies)

Water Supply Systems 15

Seaport Systems (Port, Lighthouses, etc.) 20

Parks, Plazas and Monuments 20

Other Infrastructure Assets

• Multi-purpose Pavement 5

• Solar Dryer 5

1.6 It is also emphasized in the DO that no residual value shall be recognized when

calculating the depreciation of infrastructure assets, since there is no scrap or

salvage expected to be recovered from these assets at the end of their useful life or

when they are demolished or destroyed.

1.7 The neglect of the Office of the Accountant to provide appropriate depreciation of

the abovementioned depreciable assets is a clear departure from accounting

standards, especially the IPSAS. As a result, the Municipality’s asset and equity

24