FINANCIAL AUDIT

No depreciation for some PPE items - ₱133,995,806.25

1. Items of Property, Plant, and Equipment (PPE) with a total cost of

₱133,995,806.25 were not provided with depreciation contrary to Paragraph 26

of the International Public Sector Accounting Standard (IPSAS) 45, hence, the

asset and equity accounts were overstated by the amount of depreciation that

should have been applied to these assets.

1.1 The subsequent measurement of property, plant, and equipment is provided in

IPSAS 45. Paragraph 26 thereof states that after recognition, an item of property,

plant, and equipment shall be carried at its historical cost, less any accumulated

depreciation and any accumulated impairment losses. Moreover, paragraph 41 of

the same IPSAS requires that each part of an item of PPE with a cost or value that

is significant in relation to the total cost or value of the item shall be depreciated

separately.

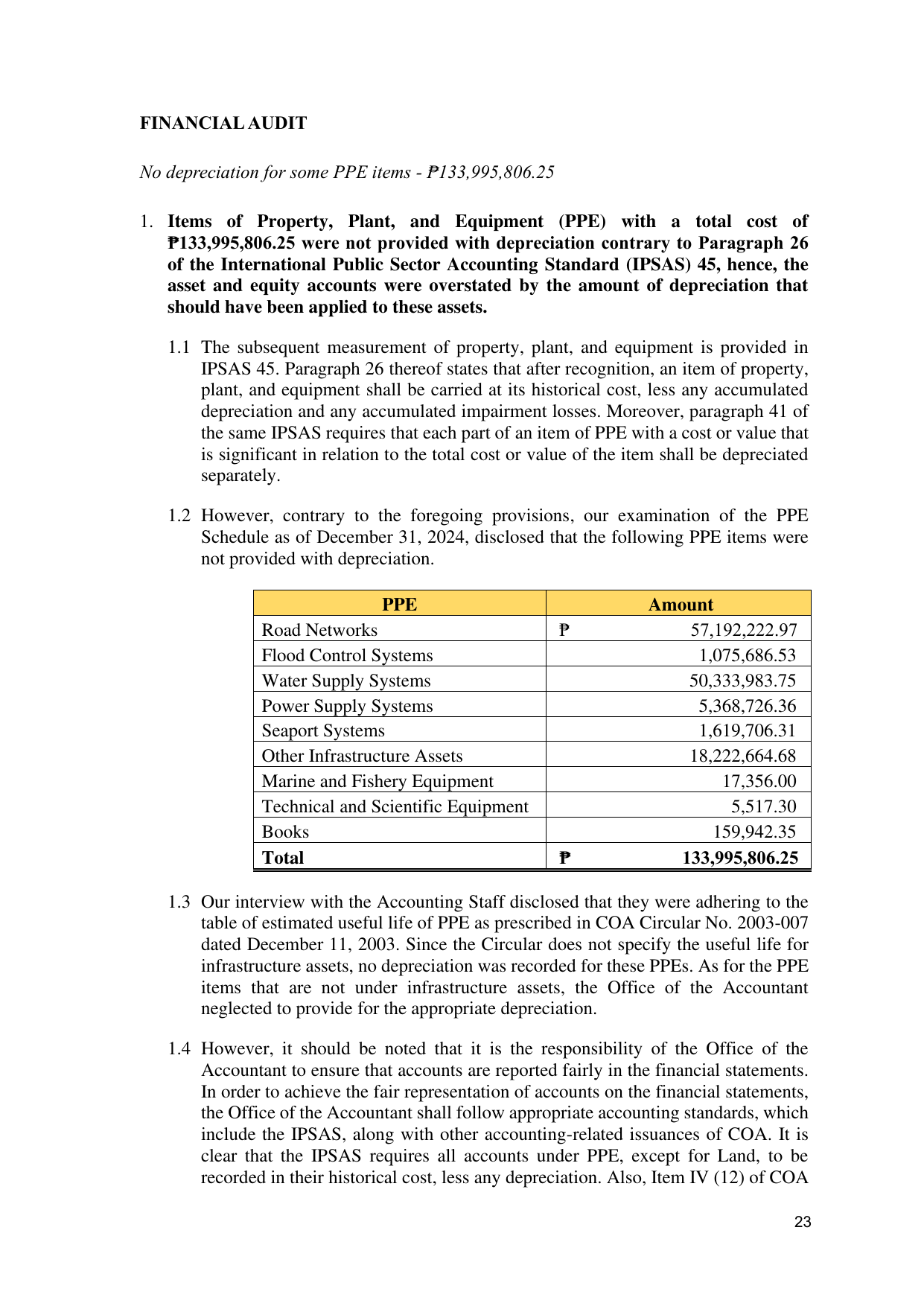

1.2 However, contrary to the foregoing provisions, our examination of the PPE

Schedule as of December 31, 2024, disclosed that the following PPE items were

not provided with depreciation.

PPE Amount

Road Networks ₱ 57,192,222.97

Flood Control Systems 1,075,686.53

Water Supply Systems 50,333,983.75

Power Supply Systems 5,368,726.36

Seaport Systems 1,619,706.31

Other Infrastructure Assets 18,222,664.68

Marine and Fishery Equipment 17,356.00

Technical and Scientific Equipment 5,517.30

Books 159,942.35

Total ₱ 133,995,806.25

1.3 Our interview with the Accounting Staff disclosed that they were adhering to the

table of estimated useful life of PPE as prescribed in COA Circular No. 2003-007

dated December 11, 2003. Since the Circular does not specify the useful life for

infrastructure assets, no depreciation was recorded for these PPEs. As for the PPE

items that are not under infrastructure assets, the Office of the Accountant

neglected to provide for the appropriate depreciation.

1.4 However, it should be noted that it is the responsibility of the Office of the

Accountant to ensure that accounts are reported fairly in the financial statements.

In order to achieve the fair representation of accounts on the financial statements,

the Office of the Accountant shall follow appropriate accounting standards, which

include the IPSAS, along with other accounting-related issuances of COA. It is

clear that the IPSAS requires all accounts under PPE, except for Land, to be

recorded in their historical cost, less any depreciation. Also, Item IV (12) of COA

23