Status of

Ref. Observation Recommendations Implementation / Results

of Validation

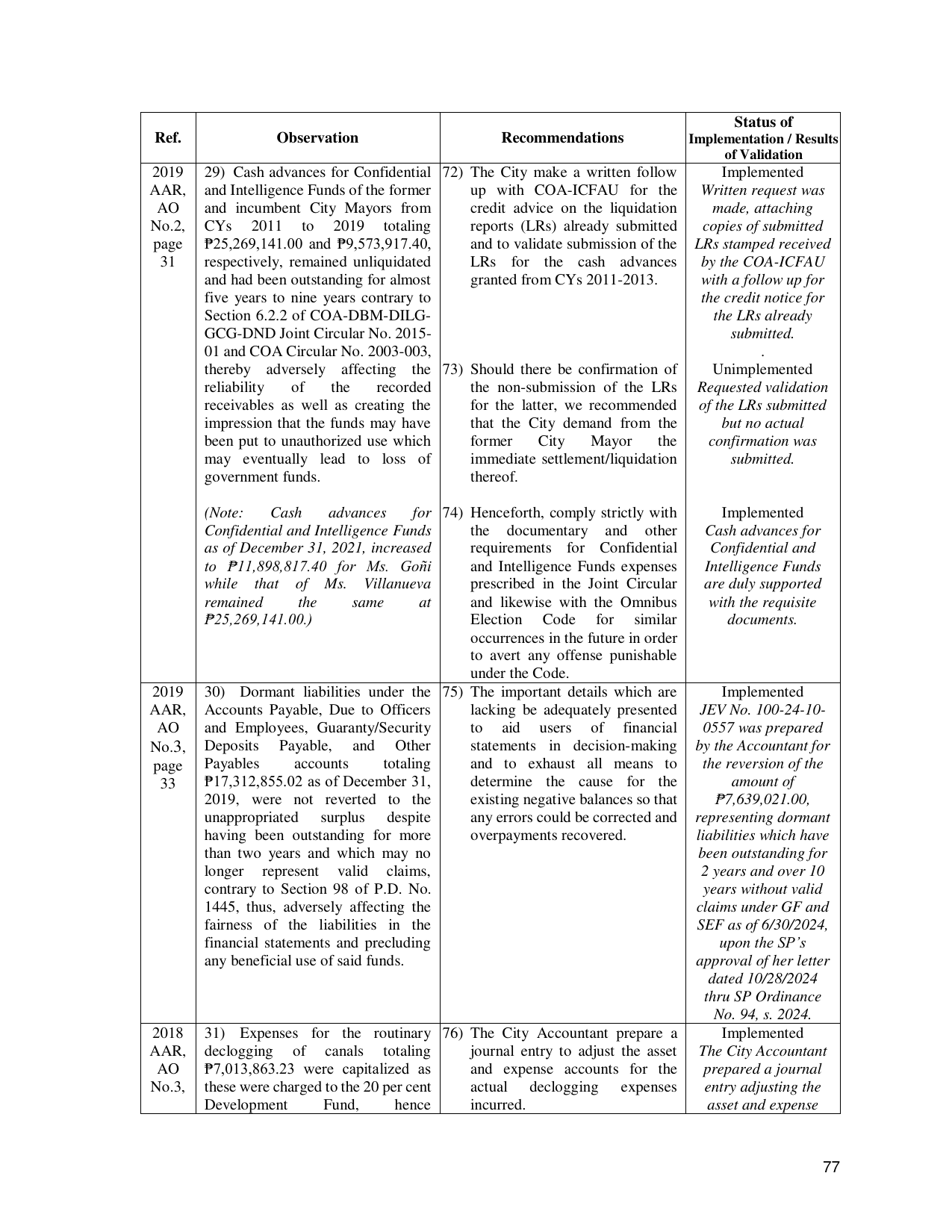

2019 29) Cash advances for Confidential 72) The City make a written follow Implemented

AAR, and Intelligence Funds of the former up with COA-ICFAU for the Written request was

AO and incumbent City Mayors from credit advice on the liquidation made, attaching

No.2, CYs 2011 to 2019 totaling reports (LRs) already submitted copies of submitted

page ₱25,269,141.00 and ₱9,573,917.40, and to validate submission of the LRs stamped received

31 respectively, remained unliquidated LRs for the cash advances by the COA-ICFAU

and had been outstanding for almost granted from CYs 2011-2013. with a follow up for

five years to nine years contrary to the credit notice for

Section 6.2.2 of COA-DBM-DILG- the LRs already

GCG-DND Joint Circular No. 2015- submitted.

01 and COA Circular No. 2003-003, .

thereby adversely affecting the 73) Should there be confirmation of Unimplemented

reliability of the recorded the non-submission of the LRs Requested validation

receivables as well as creating the for the latter, we recommended of the LRs submitted

impression that the funds may have that the City demand from the but no actual

been put to unauthorized use which former City Mayor the confirmation was

may eventually lead to loss of immediate settlement/liquidation submitted.

government funds. thereof.

(Note: Cash advances for 74) Henceforth, comply strictly with Implemented

Confidential and Intelligence Funds the documentary and other Cash advances for

as of December 31, 2021, increased requirements for Confidential Confidential and

to ₱11,898,817.40 for Ms. Goñi and Intelligence Funds expenses Intelligence Funds

while that of Ms. Villanueva prescribed in the Joint Circular are duly supported

remained the same at and likewise with the Omnibus with the requisite

₱25,269,141.00.) Election Code for similar documents.

occurrences in the future in order

to avert any offense punishable

under the Code.

2019 30) Dormant liabilities under the 75) The important details which are Implemented

AAR, Accounts Payable, Due to Officers lacking be adequately presented JEV No. 100-24-10-

AO and Employees, Guaranty/Security to aid users of financial 0557 was prepared

No.3, Deposits Payable, and Other statements in decision-making by the Accountant for

page Payables accounts totaling and to exhaust all means to the reversion of the

33 ₱17,312,855.02 as of December 31, determine the cause for the amount of

2019, were not reverted to the existing negative balances so that ₱7,639,021.00,

unappropriated surplus despite any errors could be corrected and representing dormant

having been outstanding for more overpayments recovered. liabilities which have

than two years and which may no been outstanding for

longer represent valid claims, 2 years and over 10

contrary to Section 98 of P.D. No. years without valid

1445, thus, adversely affecting the claims under GF and

fairness of the liabilities in the SEF as of 6/30/2024,

financial statements and precluding upon the SP’s

any beneficial use of said funds. approval of her letter

dated 10/28/2024

thru SP Ordinance

No. 94, s. 2024.

2018 31) Expenses for the routinary 76) The City Accountant prepare a Implemented

AAR, declogging of canals totaling journal entry to adjust the asset The City Accountant

AO ₱7,013,863.23 were capitalized as and expense accounts for the prepared a journal

No.3, these were charged to the 20 per cent actual declogging expenses entry adjusting the

Development Fund, hence incurred. asset and expense

77