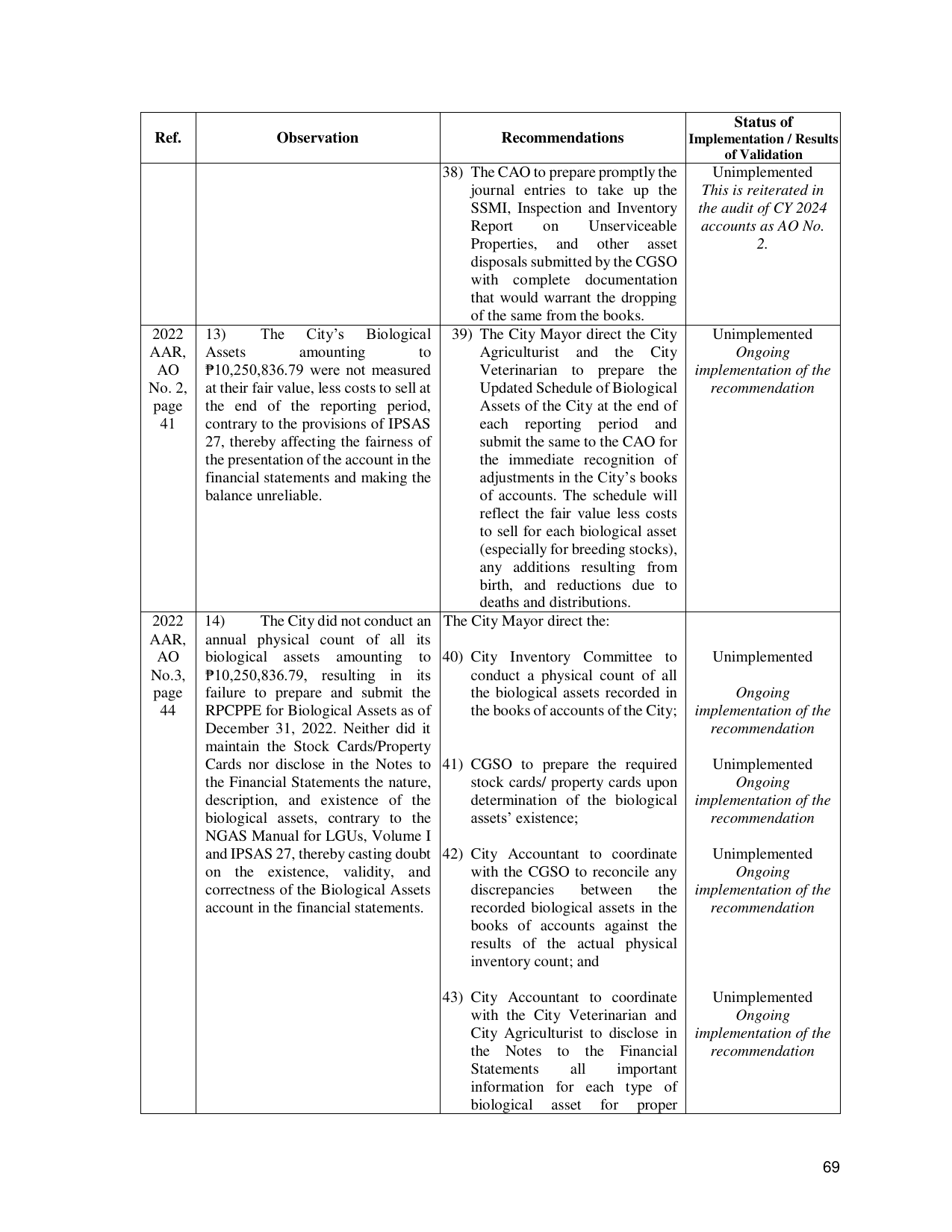

Status of

Ref. Observation Recommendations Implementation / Results

of Validation

38) The CAO to prepare promptly the Unimplemented

journal entries to take up the This is reiterated in

SSMI, Inspection and Inventory the audit of CY 2024

Report on Unserviceable accounts as AO No.

Properties, and other asset 2.

disposals submitted by the CGSO

with complete documentation

that would warrant the dropping

of the same from the books.

2022 13) The City’s Biological 39) The City Mayor direct the City Unimplemented

AAR, Assets amounting to Agriculturist and the City Ongoing

AO ₱10,250,836.79 were not measured Veterinarian to prepare the implementation of the

No. 2, at their fair value, less costs to sell at Updated Schedule of Biological recommendation

page the end of the reporting period, Assets of the City at the end of

41 contrary to the provisions of IPSAS each reporting period and

27, thereby affecting the fairness of submit the same to the CAO for

the presentation of the account in the the immediate recognition of

financial statements and making the adjustments in the City’s books

balance unreliable. of accounts. The schedule will

reflect the fair value less costs

to sell for each biological asset

(especially for breeding stocks),

any additions resulting from

birth, and reductions due to

deaths and distributions.

2022 14) The City did not conduct an The City Mayor direct the:

AAR, annual physical count of all its

AO biological assets amounting to 40) City Inventory Committee to Unimplemented

No.3, ₱10,250,836.79, resulting in its conduct a physical count of all

page failure to prepare and submit the the biological assets recorded in Ongoing

44 RPCPPE for Biological Assets as of the books of accounts of the City; implementation of the

December 31, 2022. Neither did it recommendation

maintain the Stock Cards/Property

Cards nor disclose in the Notes to 41) CGSO to prepare the required Unimplemented

the Financial Statements the nature, stock cards/ property cards upon Ongoing

description, and existence of the determination of the biological implementation of the

biological assets, contrary to the assets’ existence; recommendation

NGAS Manual for LGUs, Volume I

and IPSAS 27, thereby casting doubt 42) City Accountant to coordinate Unimplemented

on the existence, validity, and with the CGSO to reconcile any Ongoing

correctness of the Biological Assets discrepancies between the implementation of the

account in the financial statements. recorded biological assets in the recommendation

books of accounts against the

results of the actual physical

inventory count; and

43) City Accountant to coordinate Unimplemented

with the City Veterinarian and Ongoing

City Agriculturist to disclose in implementation of the

the Notes to the Financial recommendation

Statements all important

information for each type of

biological asset for proper

69