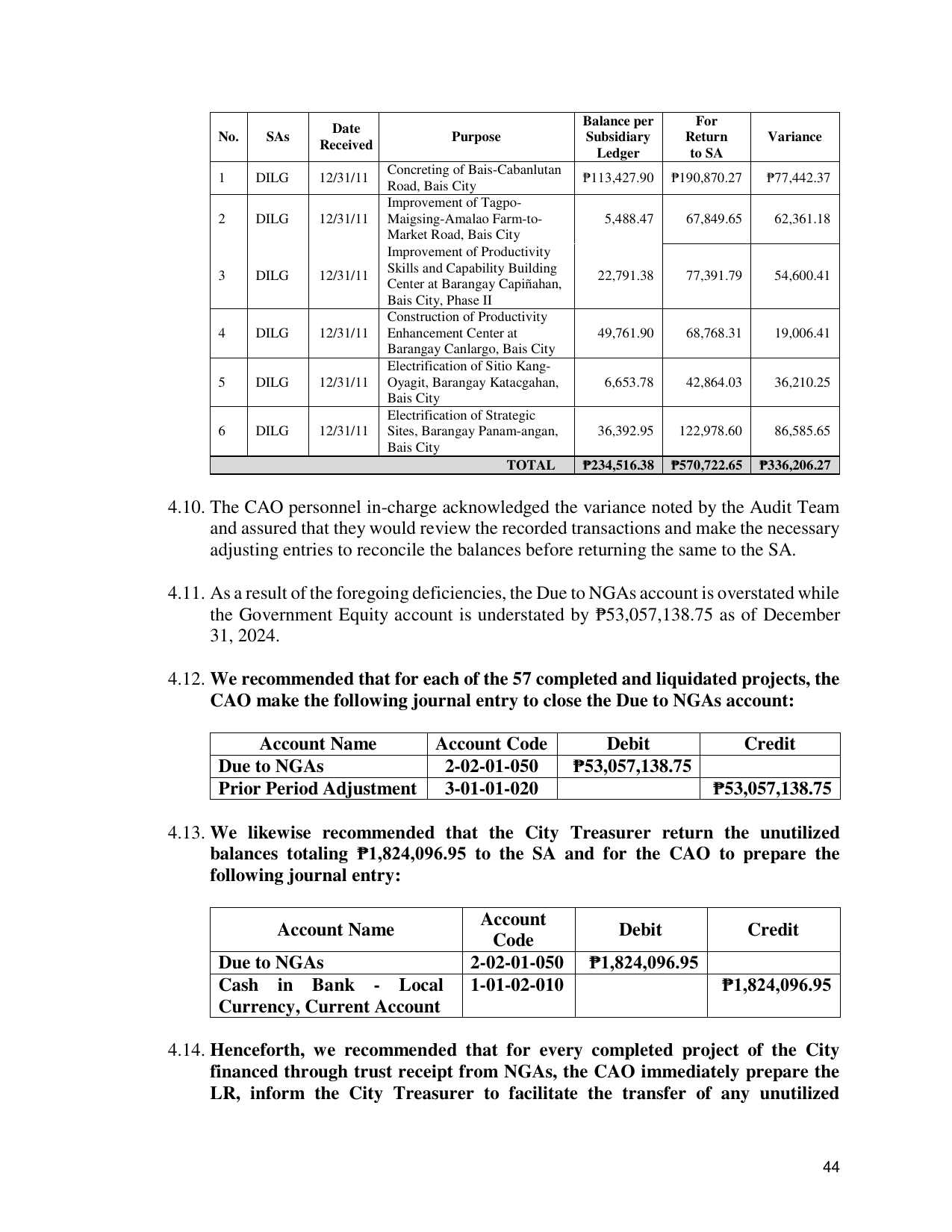

Balance per For

Date

No. SAs Purpose Subsidiary Return Variance

Received

Ledger to SA

Concreting of Bais-Cabanlutan

1 DILG 12/31/11 ₱113,427.90 ₱190,870.27 ₱77,442.37

Road, Bais City

Improvement of Tagpo-

2 DILG 12/31/11 Maigsing-Amalao Farm-to- 5,488.47 67,849.65 62,361.18

Market Road, Bais City

Improvement of Productivity

Skills and Capability Building

3 DILG 12/31/11 22,791.38 77,391.79 54,600.41

Center at Barangay Capiñahan,

Bais City, Phase II

Construction of Productivity

4 DILG 12/31/11 Enhancement Center at 49,761.90 68,768.31 19,006.41

Barangay Canlargo, Bais City

Electrification of Sitio Kang-

5 DILG 12/31/11 Oyagit, Barangay Katacgahan, 6,653.78 42,864.03 36,210.25

Bais City

Electrification of Strategic

6 DILG 12/31/11 Sites, Barangay Panam-angan, 36,392.95 122,978.60 86,585.65

Bais City

TOTAL ₱234,516.38 ₱570,722.65 ₱336,206.27

4.10. The CAO personnel in-charge acknowledged the variance noted by the Audit Team

and assured that they would review the recorded transactions and make the necessary

adjusting entries to reconcile the balances before returning the same to the SA.

4.11. As a result of the foregoing deficiencies, the Due to NGAs account is overstated while

the Government Equity account is understated by ₱53,057,138.75 as of December

31, 2024.

4.12. We recommended that for each of the 57 completed and liquidated projects, the

CAO make the following journal entry to close the Due to NGAs account:

Account Name Account Code Debit Credit

Due to NGAs 2-02-01-050 ₱53,057,138.75

Prior Period Adjustment 3-01-01-020 ₱53,057,138.75

4.13. We likewise recommended that the City Treasurer return the unutilized

balances totaling ₱1,824,096.95 to the SA and for the CAO to prepare the

following journal entry:

Account

Account Name Debit Credit

Code

Due to NGAs 2-02-01-050 ₱1,824,096.95

Cash in Bank - Local 1-01-02-010 ₱1,824,096.95

Currency, Current Account

4.14. Henceforth, we recommended that for every completed project of the City

financed through trust receipt from NGAs, the CAO immediately prepare the

LR, inform the City Treasurer to facilitate the transfer of any unutilized

44