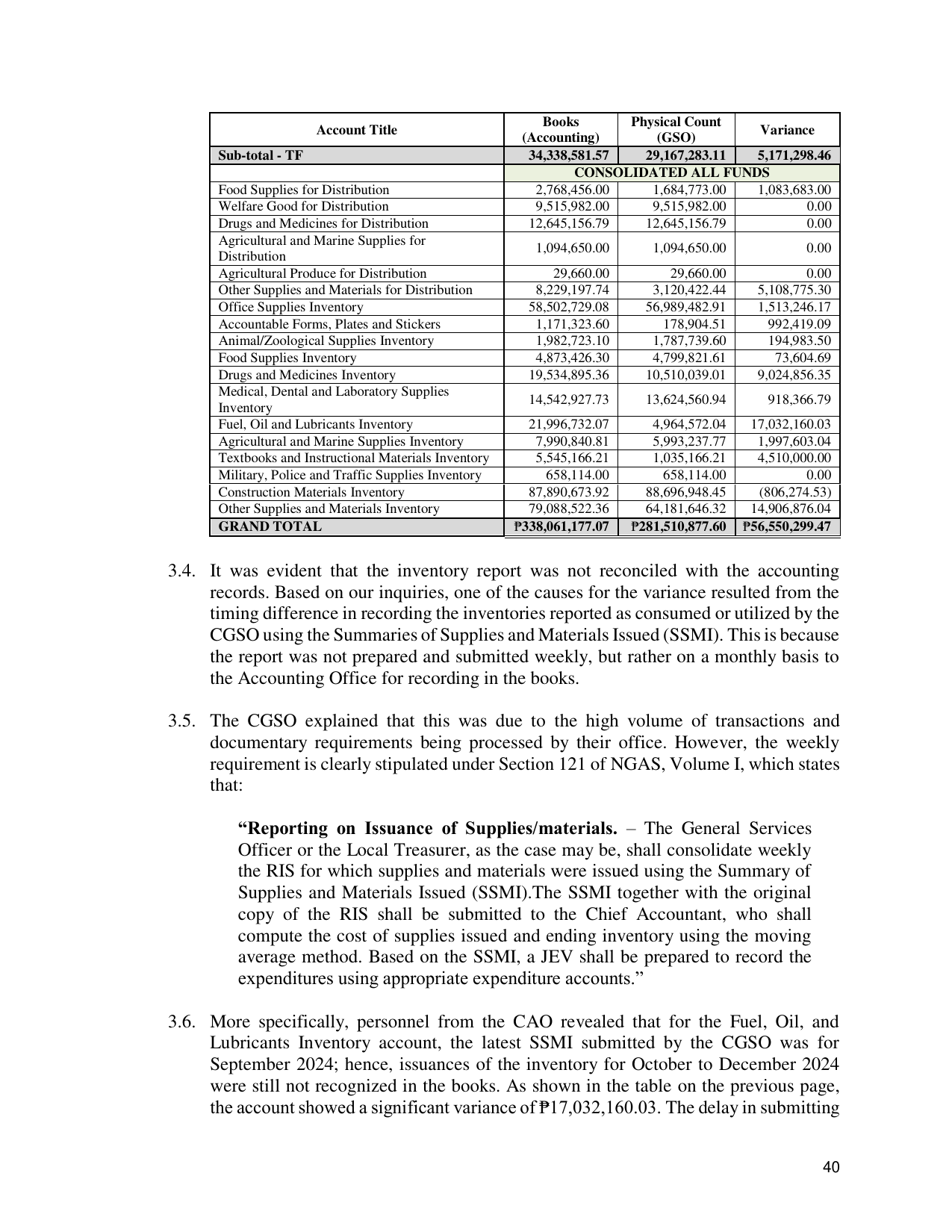

Books Physical Count

Account Title Variance

(Accounting) (GSO)

Sub-total - TF 34,338,581.57 29,167,283.11 5,171,298.46

CONSOLIDATED ALL FUNDS

Food Supplies for Distribution 2,768,456.00 1,684,773.00 1,083,683.00

Welfare Good for Distribution 9,515,982.00 9,515,982.00 0.00

Drugs and Medicines for Distribution 12,645,156.79 12,645,156.79 0.00

Agricultural and Marine Supplies for

1,094,650.00 1,094,650.00 0.00

Distribution

Agricultural Produce for Distribution 29,660.00 29,660.00 0.00

Other Supplies and Materials for Distribution 8,229,197.74 3,120,422.44 5,108,775.30

Office Supplies Inventory 58,502,729.08 56,989,482.91 1,513,246.17

Accountable Forms, Plates and Stickers 1,171,323.60 178,904.51 992,419.09

Animal/Zoological Supplies Inventory 1,982,723.10 1,787,739.60 194,983.50

Food Supplies Inventory 4,873,426.30 4,799,821.61 73,604.69

Drugs and Medicines Inventory 19,534,895.36 10,510,039.01 9,024,856.35

Medical, Dental and Laboratory Supplies

14,542,927.73 13,624,560.94 918,366.79

Inventory

Fuel, Oil and Lubricants Inventory 21,996,732.07 4,964,572.04 17,032,160.03

Agricultural and Marine Supplies Inventory 7,990,840.81 5,993,237.77 1,997,603.04

Textbooks and Instructional Materials Inventory 5,545,166.21 1,035,166.21 4,510,000.00

Military, Police and Traffic Supplies Inventory 658,114.00 658,114.00 0.00

Construction Materials Inventory 87,890,673.92 88,696,948.45 (806,274.53)

Other Supplies and Materials Inventory 79,088,522.36 64,181,646.32 14,906,876.04

GRAND TOTAL ₱338,061,177.07 ₱281,510,877.60 ₱56,550,299.47

3.4. It was evident that the inventory report was not reconciled with the accounting

records. Based on our inquiries, one of the causes for the variance resulted from the

timing difference in recording the inventories reported as consumed or utilized by the

CGSO using the Summaries of Supplies and Materials Issued (SSMI). This is because

the report was not prepared and submitted weekly, but rather on a monthly basis to

the Accounting Office for recording in the books.

3.5. The CGSO explained that this was due to the high volume of transactions and

documentary requirements being processed by their office. However, the weekly

requirement is clearly stipulated under Section 121 of NGAS, Volume I, which states

that:

“Reporting on Issuance of Supplies/materials. – The General Services

Officer or the Local Treasurer, as the case may be, shall consolidate weekly

the RIS for which supplies and materials were issued using the Summary of

Supplies and Materials Issued (SSMI).The SSMI together with the original

copy of the RIS shall be submitted to the Chief Accountant, who shall

compute the cost of supplies issued and ending inventory using the moving

average method. Based on the SSMI, a JEV shall be prepared to record the

expenditures using appropriate expenditure accounts.”

3.6. More specifically, personnel from the CAO revealed that for the Fuel, Oil, and

Lubricants Inventory account, the latest SSMI submitted by the CGSO was for

September 2024; hence, issuances of the inventory for October to December 2024

were still not recognized in the books. As shown in the table on the previous page,

the account showed a significant variance of ₱17,032,160.03. The delay in submitting

40