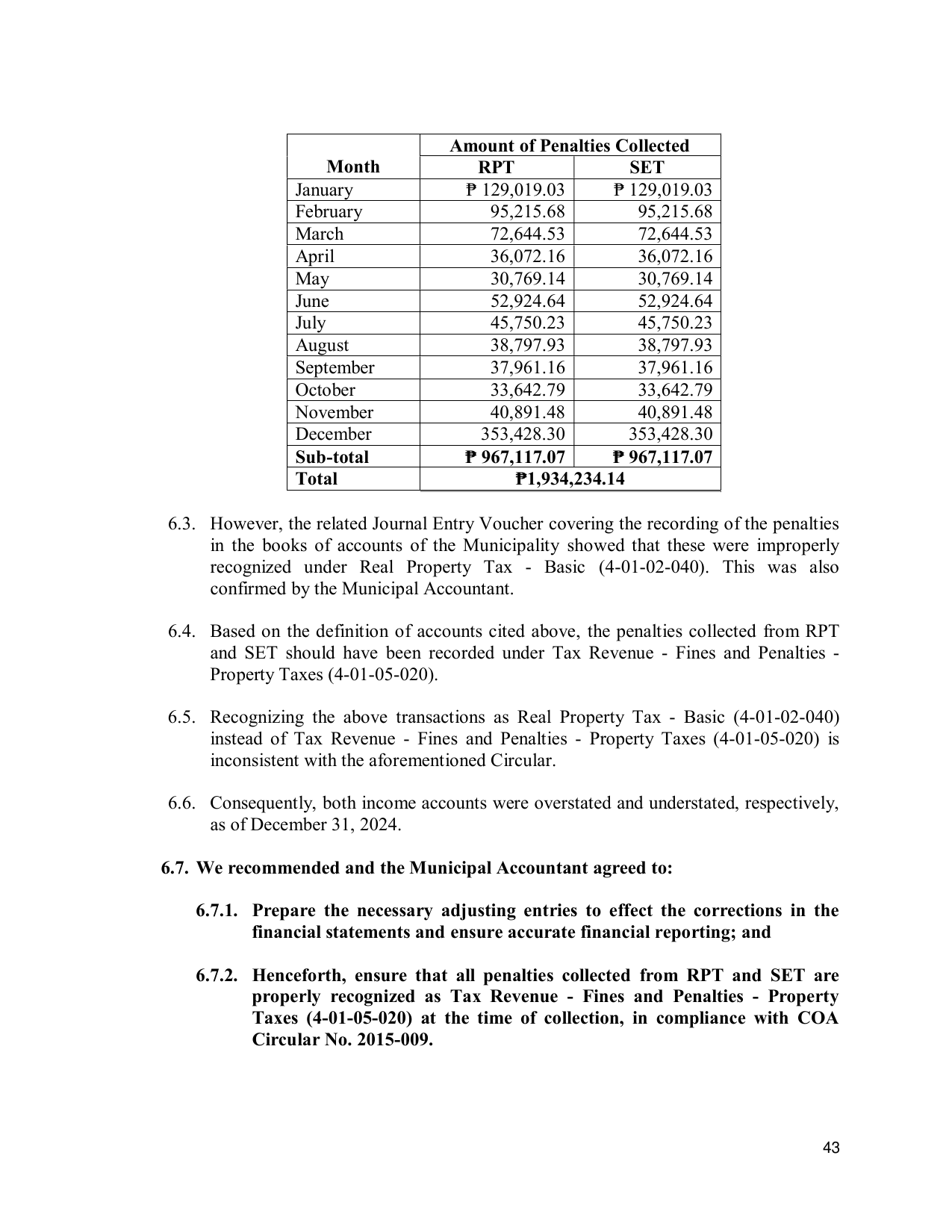

Amount of Penalties Collected

Month RPT SET

January ₱ 129,019.03 ₱ 129,019.03

February 95,215.68 95,215.68

March 72,644.53 72,644.53

April 36,072.16 36,072.16

May 30,769.14 30,769.14

June 52,924.64 52,924.64

July 45,750.23 45,750.23

August 38,797.93 38,797.93

September 37,961.16 37,961.16

October 33,642.79 33,642.79

November 40,891.48 40,891.48

December 353,428.30 353,428.30

Sub-total ₱ 967,117.07 ₱ 967,117.07

Total ₱1,934,234.14

6.3. However, the related Journal Entry Voucher covering the recording of the penalties

in the books of accounts of the Municipality showed that these were improperly

recognized under Real Property Tax - Basic (4-01-02-040). This was also

confirmed by the Municipal Accountant.

6.4. Based on the definition of accounts cited above, the penalties collected from RPT

and SET should have been recorded under Tax Revenue - Fines and Penalties -

Property Taxes (4-01-05-020).

6.5. Recognizing the above transactions as Real Property Tax - Basic (4-01-02-040)

instead of Tax Revenue - Fines and Penalties - Property Taxes (4-01-05-020) is

inconsistent with the aforementioned Circular.

6.6. Consequently, both income accounts were overstated and understated, respectively,

as of December 31, 2024.

6.7. We recommended and the Municipal Accountant agreed to:

6.7.1. Prepare the necessary adjusting entries to effect the corrections in the

financial statements and ensure accurate financial reporting; and

6.7.2. Henceforth, ensure that all penalties collected from RPT and SET are

properly recognized as Tax Revenue - Fines and Penalties - Property

Taxes (4-01-05-020) at the time of collection, in compliance with COA

Circular No. 2015-009.

43