Erroneous Recording of RPT Penalties

6. Inconsistent with COA Circular No. 2015-009, penalties from Real Property Tax

(RPT) and Special Education Tax (SET) collections totaling ₱1,934,234.14 in CY

2024 were erroneously recorded in the books of accounts as Real Property Tax -

Basic (4-01-02-040) instead of Tax Revenue - Fines and Penalties - Property Taxes

(4-01-05-020), hence, both income accounts were overstated and understated,

respectively, as of December 31, 2024.

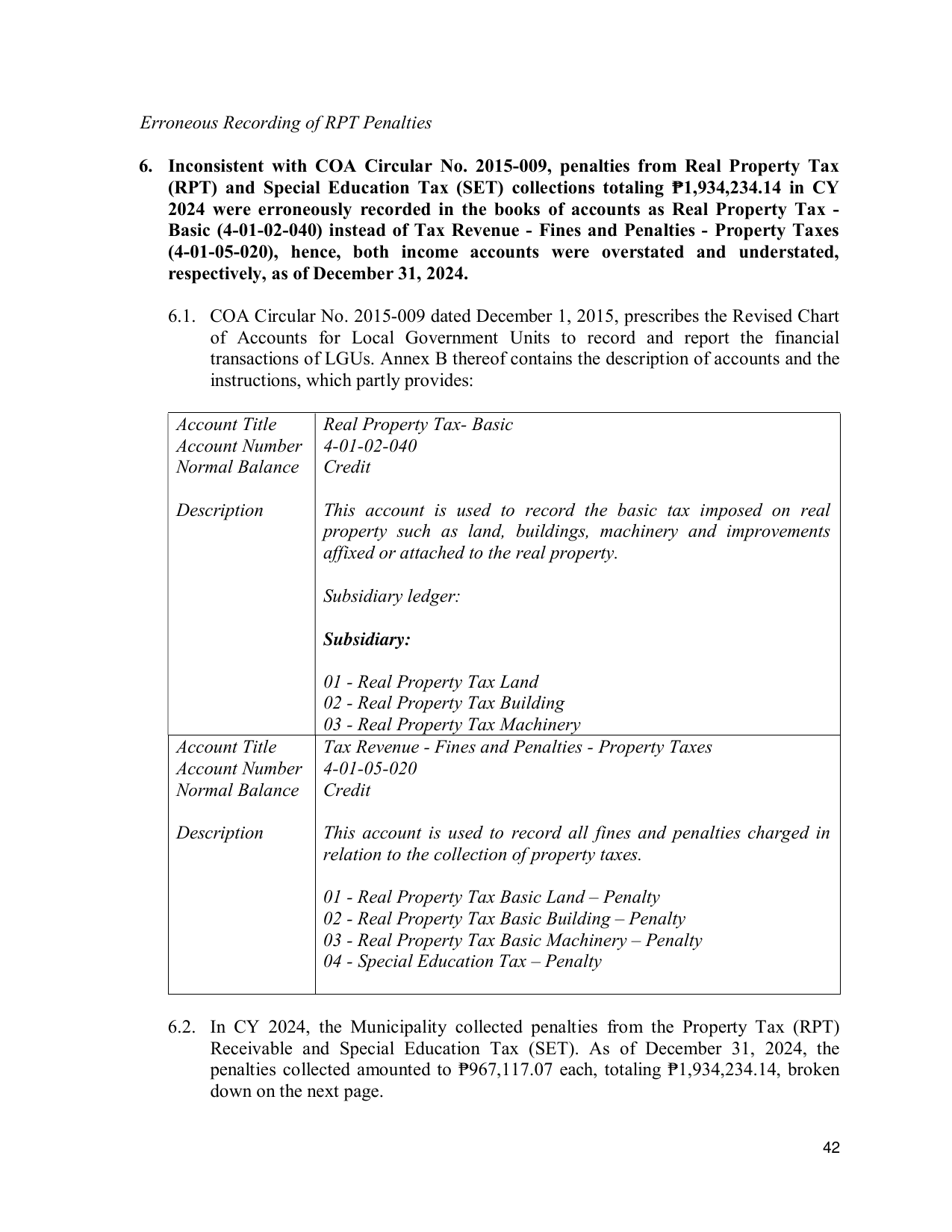

6.1. COA Circular No. 2015-009 dated December 1, 2015, prescribes the Revised Chart

of Accounts for Local Government Units to record and report the financial

transactions of LGUs. Annex B thereof contains the description of accounts and the

instructions, which partly provides:

Account Title Real Property Tax- Basic

Account Number 4-01-02-040

Normal Balance Credit

Description This account is used to record the basic tax imposed on real

property such as land, buildings, machinery and improvements

affixed or attached to the real property.

Subsidiary ledger:

Subsidiary:

01 - Real Property Tax Land

02 - Real Property Tax Building

03 - Real Property Tax Machinery

Account Title Tax Revenue - Fines and Penalties - Property Taxes

Account Number 4-01-05-020

Normal Balance Credit

Description This account is used to record all fines and penalties charged in

relation to the collection of property taxes.

01 - Real Property Tax Basic Land – Penalty

02 - Real Property Tax Basic Building – Penalty

03 - Real Property Tax Basic Machinery – Penalty

04 - Special Education Tax – Penalty

6.2. In CY 2024, the Municipality collected penalties from the Property Tax (RPT)

Receivable and Special Education Tax (SET). As of December 31, 2024, the

penalties collected amounted to ₱967,117.07 each, totaling ₱1,934,234.14, broken

down on the next page.

42