Ref.

Audit Observations Audit Recommendations Status of Implementation

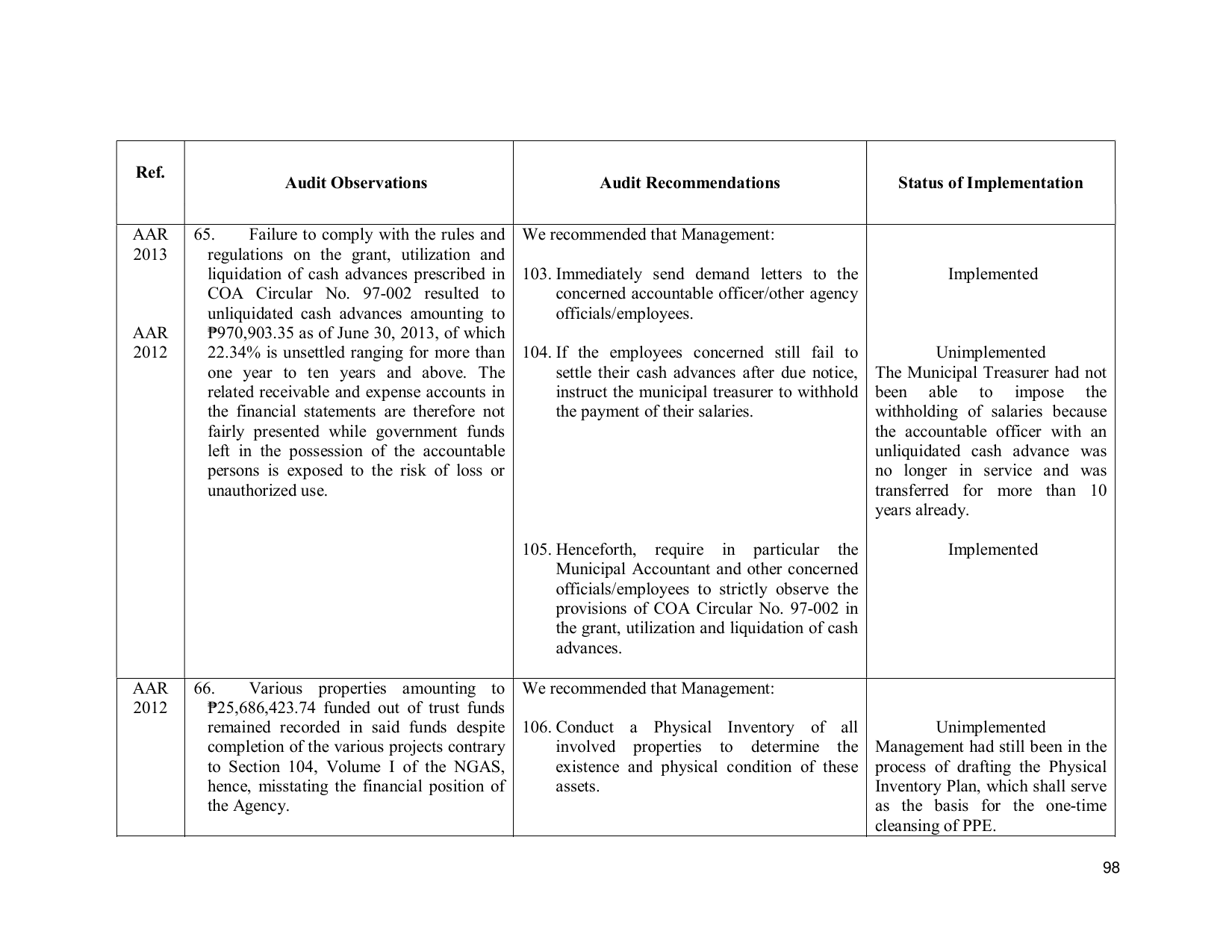

AAR 65. Failure to comply with the rules and We recommended that Management:

2013 regulations on the grant, utilization and

liquidation of cash advances prescribed in 103. Immediately send demand letters to the Implemented

COA Circular No. 97-002 resulted to concerned accountable officer/other agency

unliquidated cash advances amounting to officials/employees.

AAR ₱970,903.35 as of June 30, 2013, of which

2012 22.34% is unsettled ranging for more than 104. If the employees concerned still fail to Unimplemented

one year to ten years and above. The settle their cash advances after due notice, The Municipal Treasurer had not

related receivable and expense accounts in instruct the municipal treasurer to withhold been able to impose the

the financial statements are therefore not the payment of their salaries. withholding of salaries because

fairly presented while government funds the accountable officer with an

left in the possession of the accountable unliquidated cash advance was

persons is exposed to the risk of loss or no longer in service and was

unauthorized use. transferred for more than 10

years already.

105. Henceforth, require in particular the Implemented

Municipal Accountant and other concerned

officials/employees to strictly observe the

provisions of COA Circular No. 97-002 in

the grant, utilization and liquidation of cash

advances.

AAR 66. Various properties amounting to We recommended that Management:

2012 ₱25,686,423.74 funded out of trust funds

remained recorded in said funds despite 106. Conduct a Physical Inventory of all Unimplemented

completion of the various projects contrary involved properties to determine the Management had still been in the

to Section 104, Volume I of the NGAS, existence and physical condition of these process of drafting the Physical

hence, misstating the financial position of assets. Inventory Plan, which shall serve

the Agency. as the basis for the one-time

cleansing of PPE.

98