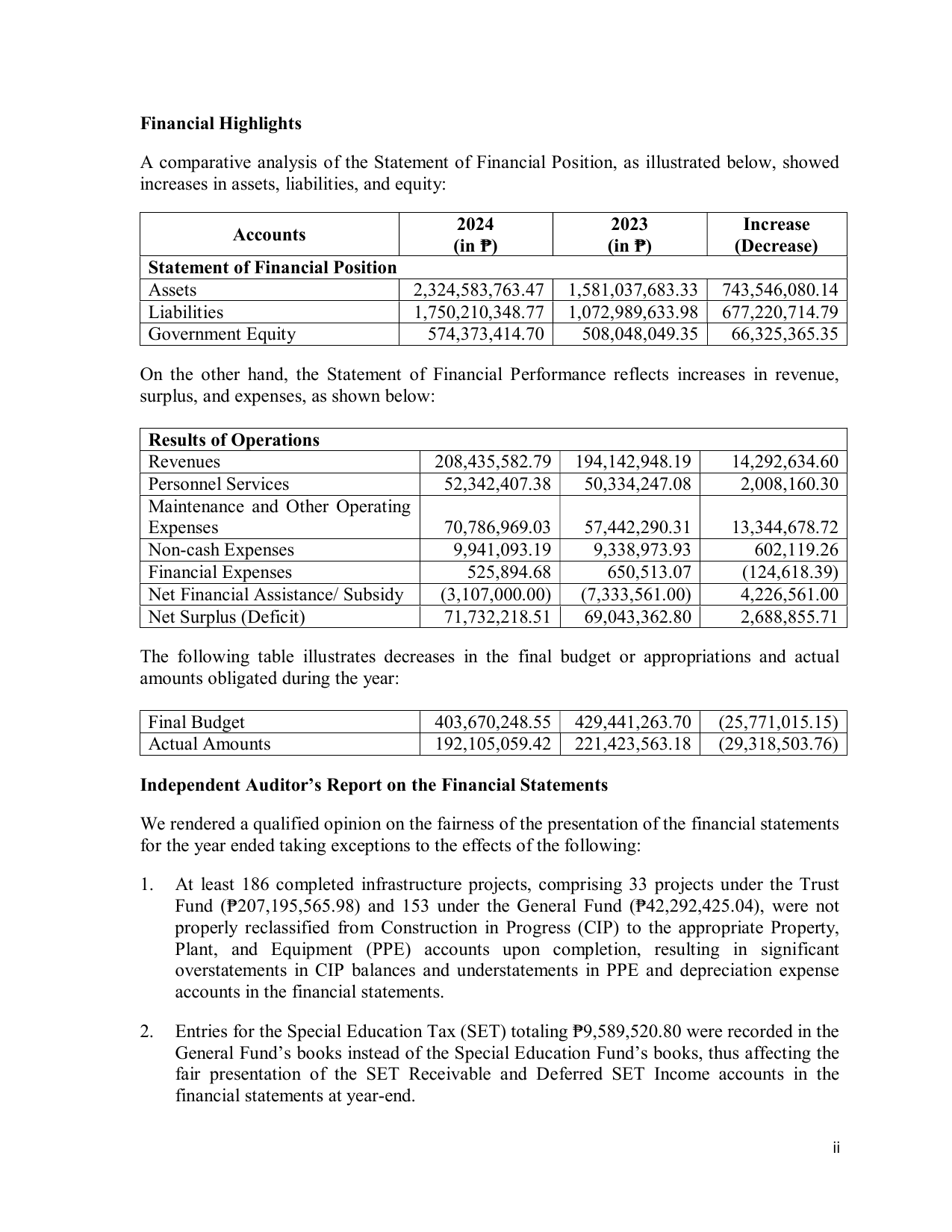

Financial Highlights

A comparative analysis of the Statement of Financial Position, as illustrated below, showed

increases in assets, liabilities, and equity:

2024 2023 Increase

Accounts

(in ₱) (in ₱) (Decrease)

Statement of Financial Position

Assets 2,324,583,763.47 1,581,037,683.33 743,546,080.14

Liabilities 1,750,210,348.77 1,072,989,633.98 677,220,714.79

Government Equity 574,373,414.70 508,048,049.35 66,325,365.35

On the other hand, the Statement of Financial Performance reflects increases in revenue,

surplus, and expenses, as shown below:

Results of Operations

Revenues 208,435,582.79 194,142,948.19 14,292,634.60

Personnel Services 52,342,407.38 50,334,247.08 2,008,160.30

Maintenance and Other Operating

Expenses 70,786,969.03 57,442,290.31 13,344,678.72

Non-cash Expenses 9,941,093.19 9,338,973.93 602,119.26

Financial Expenses 525,894.68 650,513.07 (124,618.39)

Net Financial Assistance/ Subsidy (3,107,000.00) (7,333,561.00) 4,226,561.00

Net Surplus (Deficit) 71,732,218.51 69,043,362.80 2,688,855.71

The following table illustrates decreases in the final budget or appropriations and actual

amounts obligated during the year:

Final Budget 403,670,248.55 429,441,263.70 (25,771,015.15)

Actual Amounts 192,105,059.42 221,423,563.18 (29,318,503.76)

Independent Auditor’s Report on the Financial Statements

We rendered a qualified opinion on the fairness of the presentation of the financial statements

for the year ended taking exceptions to the effects of the following:

1. At least 186 completed infrastructure projects, comprising 33 projects under the Trust

Fund (₱207,195,565.98) and 153 under the General Fund (₱42,292,425.04), were not

properly reclassified from Construction in Progress (CIP) to the appropriate Property,

Plant, and Equipment (PPE) accounts upon completion, resulting in significant

overstatements in CIP balances and understatements in PPE and depreciation expense

accounts in the financial statements.

2. Entries for the Special Education Tax (SET) totaling ₱9,589,520.80 were recorded in the

General Fund’s books instead of the Special Education Fund’s books, thus affecting the

fair presentation of the SET Receivable and Deferred SET Income accounts in the

financial statements at year-end.

ii