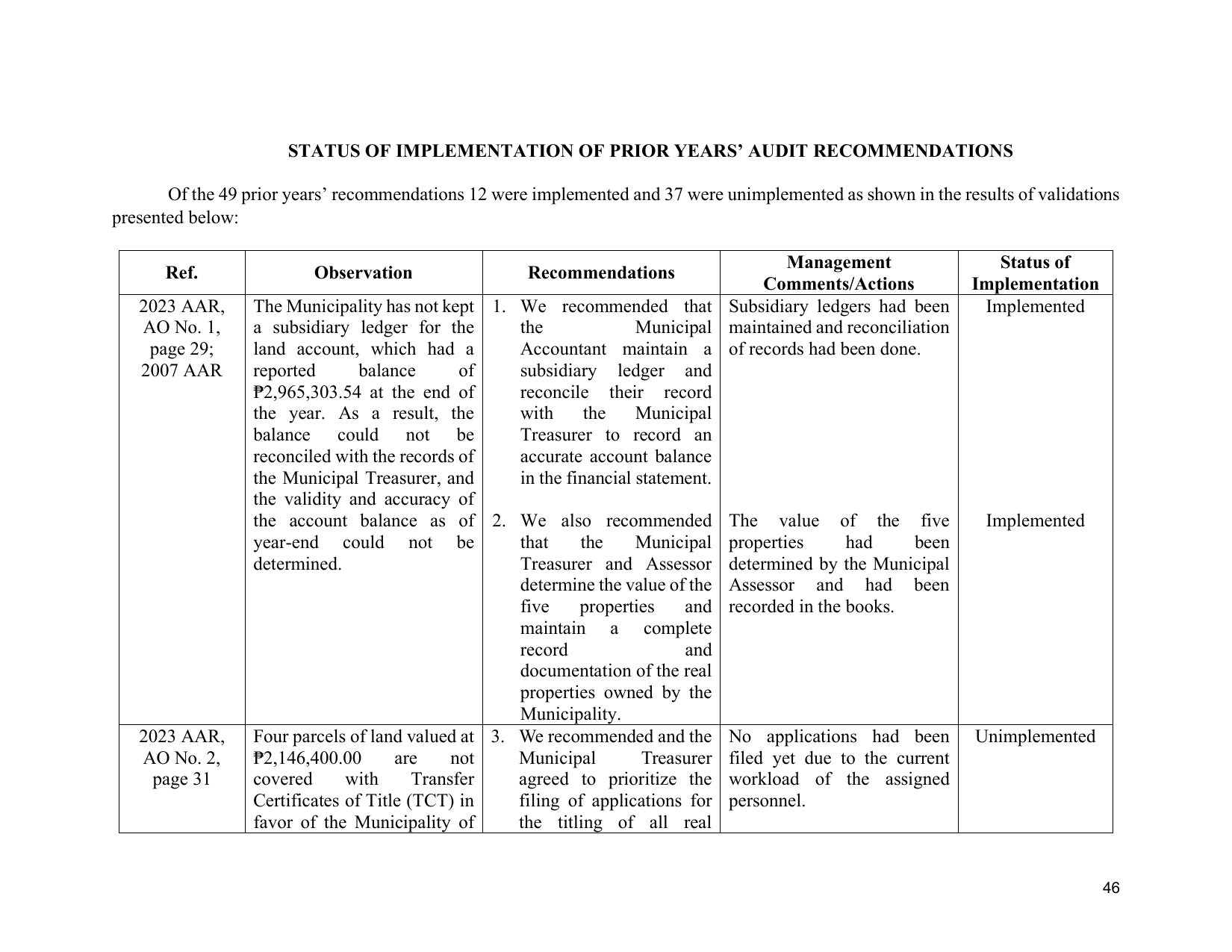

STATUS OF IMPLEMENTATION OF PRIOR YEARS’ AUDIT RECOMMENDATIONS

Of the 49 prior years’ recommendations 12 were implemented and 37 were unimplemented as shown in the results of validations

presented below:

Management Status of

Ref. Observation Recommendations

Comments/Actions Implementation

2023 AAR, The Municipality has not kept 1. We recommended that Subsidiary ledgers had been Implemented

AO No. 1, a subsidiary ledger for the the Municipal maintained and reconciliation

page 29; land account, which had a Accountant maintain a of records had been done.

2007 AAR reported balance of subsidiary ledger and

₱2,965,303.54 at the end of reconcile their record

the year. As a result, the with the Municipal

balance could not be Treasurer to record an

reconciled with the records of accurate account balance

the Municipal Treasurer, and in the financial statement.

the validity and accuracy of

the account balance as of 2. We also recommended The value of the five Implemented

year-end could not be that the Municipal properties had been

determined. Treasurer and Assessor determined by the Municipal

determine the value of the Assessor and had been

five properties and recorded in the books.

maintain a complete

record and

documentation of the real

properties owned by the

Municipality.

2023 AAR, Four parcels of land valued at 3. We recommended and the No applications had been Unimplemented

AO No. 2, ₱2,146,400.00 are not Municipal Treasurer filed yet due to the current

page 31 covered with Transfer agreed to prioritize the workload of the assigned

Certificates of Title (TCT) in filing of applications for personnel.

favor of the Municipality of the titling of all real

46