Section 124. Inventory of Supplies or Property.- The local chief executive

shall require periodic physical inventory of supplies or property. Physical

count of inventory items by type shall be conducted semestrally and

reported in the Report of the Physical Count of Inventories (RPCI). This

shall be submitted to the Auditor concerned not later than July 31, and

January 31 of each year for the first and second semesters, respectively.”

2.2. Our review of the financial statements revealed that as of December 31, 2024, the

Municipality’s Accountable Forms, Plates, and Stickers account had a balance of

₱1,074,559.30, while the related Accountable Forms Expense account reflected only

₱510.00. Given the Municipality's daily use of various accountable forms, the

minimal expense recorded for the whole year appears unusual and warrants further

investigation.

2.3. Our inquiry with the Municipal Accountant disclosed that the Accountable Forms,

Plates, and Stickers inventory account comprises various accountable forms utilized

by different municipal offices. These include community tax certificates for

individuals/corporations, accountable forms used in the regular business of the LGU

(AF 51, AF 56 etc), bank checks, cash tickets and amusement tickets used by the

Municipal Treasurer's Office, as well as birth, death, and marriage certificates among

others issued by the Municipal Civil Registrar’s Office.

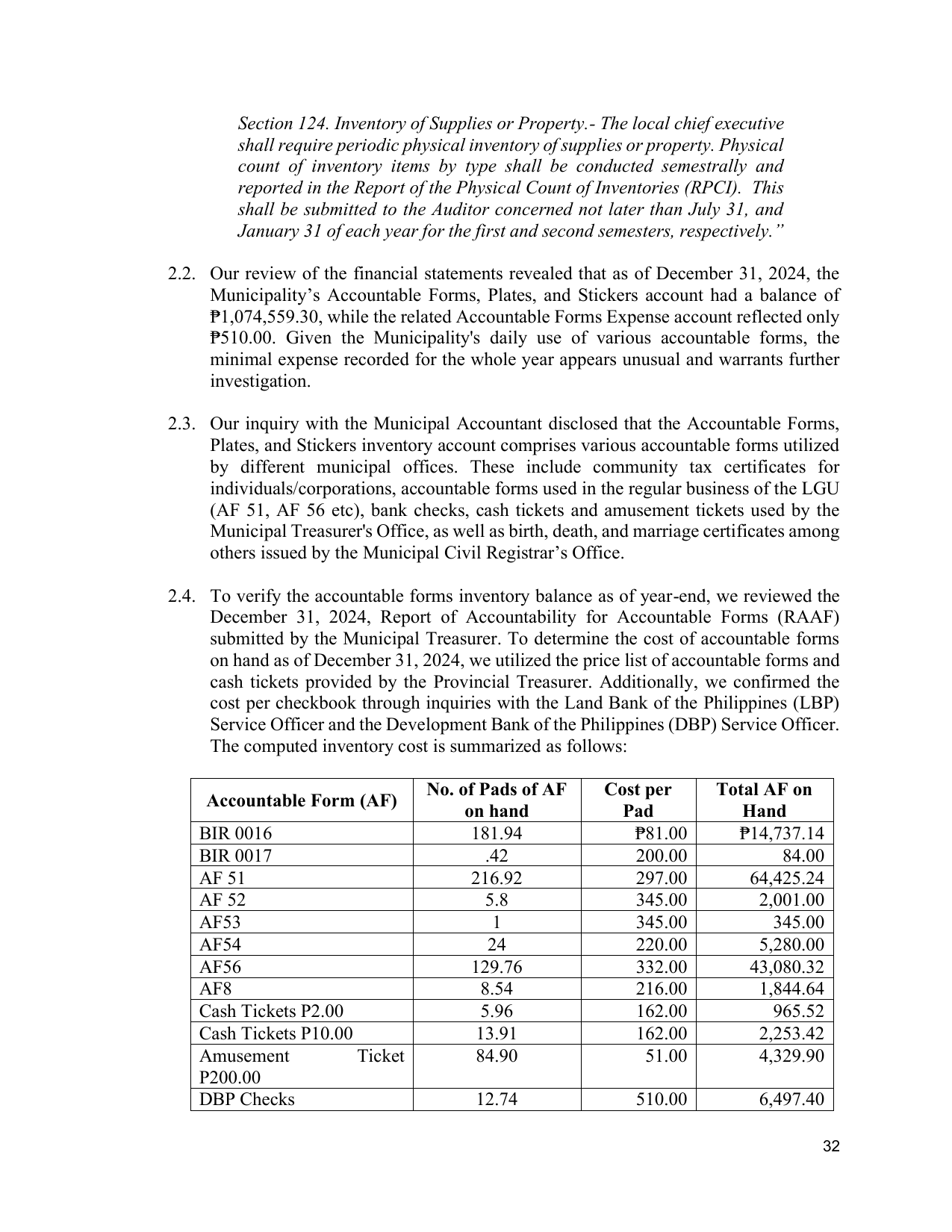

2.4. To verify the accountable forms inventory balance as of year-end, we reviewed the

December 31, 2024, Report of Accountability for Accountable Forms (RAAF)

submitted by the Municipal Treasurer. To determine the cost of accountable forms

on hand as of December 31, 2024, we utilized the price list of accountable forms and

cash tickets provided by the Provincial Treasurer. Additionally, we confirmed the

cost per checkbook through inquiries with the Land Bank of the Philippines (LBP)

Service Officer and the Development Bank of the Philippines (DBP) Service Officer.

The computed inventory cost is summarized as follows:

No. of Pads of AF Cost per Total AF on

Accountable Form (AF)

on hand Pad Hand

BIR 0016 181.94 ₱81.00 ₱14,737.14

BIR 0017 .42 200.00 84.00

AF 51 216.92 297.00 64,425.24

AF 52 5.8 345.00 2,001.00

AF53 1 345.00 345.00

AF54 24 220.00 5,280.00

AF56 129.76 332.00 43,080.32

AF8 8.54 216.00 1,844.64

Cash Tickets P2.00 5.96 162.00 965.52

Cash Tickets P10.00 13.91 162.00 2,253.42

Amusement Ticket 84.90 51.00 4,329.90

P200.00

DBP Checks 12.74 510.00 6,497.40

32