Annex A

Status of Implementation/

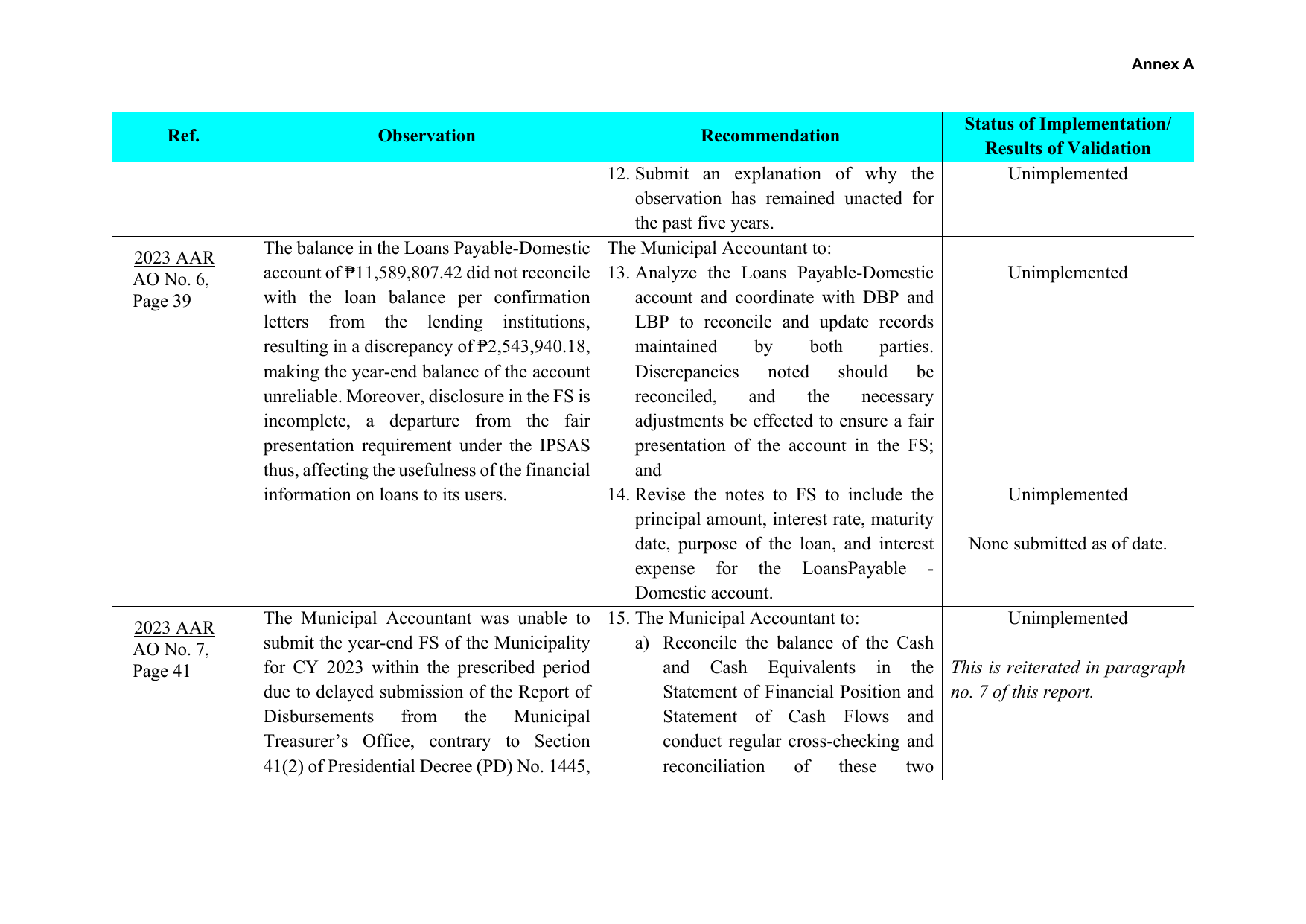

Ref. Observation Recommendation

Results of Validation

12. Submit an explanation of why the Unimplemented

observation has remained unacted for

the past five years.

The balance in the Loans Payable-Domestic The Municipal Accountant to:

2023 AAR

AO No. 6, account of ₱11,589,807.42 did not reconcile 13. Analyze the Loans Payable-Domestic Unimplemented

Page 39 with the loan balance per confirmation account and coordinate with DBP and

letters from the lending institutions, LBP to reconcile and update records

resulting in a discrepancy of ₱2,543,940.18, maintained by both parties.

making the year-end balance of the account Discrepancies noted should be

unreliable. Moreover, disclosure in the FS is reconciled, and the necessary

incomplete, a departure from the fair adjustments be effected to ensure a fair

presentation requirement under the IPSAS presentation of the account in the FS;

thus, affecting the usefulness of the financial and

information on loans to its users. 14. Revise the notes to FS to include the Unimplemented

principal amount, interest rate, maturity

date, purpose of the loan, and interest None submitted as of date.

expense for the LoansPayable -

Domestic account.

The Municipal Accountant was unable to 15. The Municipal Accountant to: Unimplemented

2023 AAR

AO No. 7, submit the year-end FS of the Municipality a) Reconcile the balance of the Cash

Page 41 for CY 2023 within the prescribed period and Cash Equivalents in the This is reiterated in paragraph

due to delayed submission of the Report of Statement of Financial Position and no. 7 of this report.

Disbursements from the Municipal Statement of Cash Flows and

Treasurer’s Office, contrary to Section conduct regular cross-checking and

41(2) of Presidential Decree (PD) No. 1445, reconciliation of these two