Annex A

Status of Implementation/

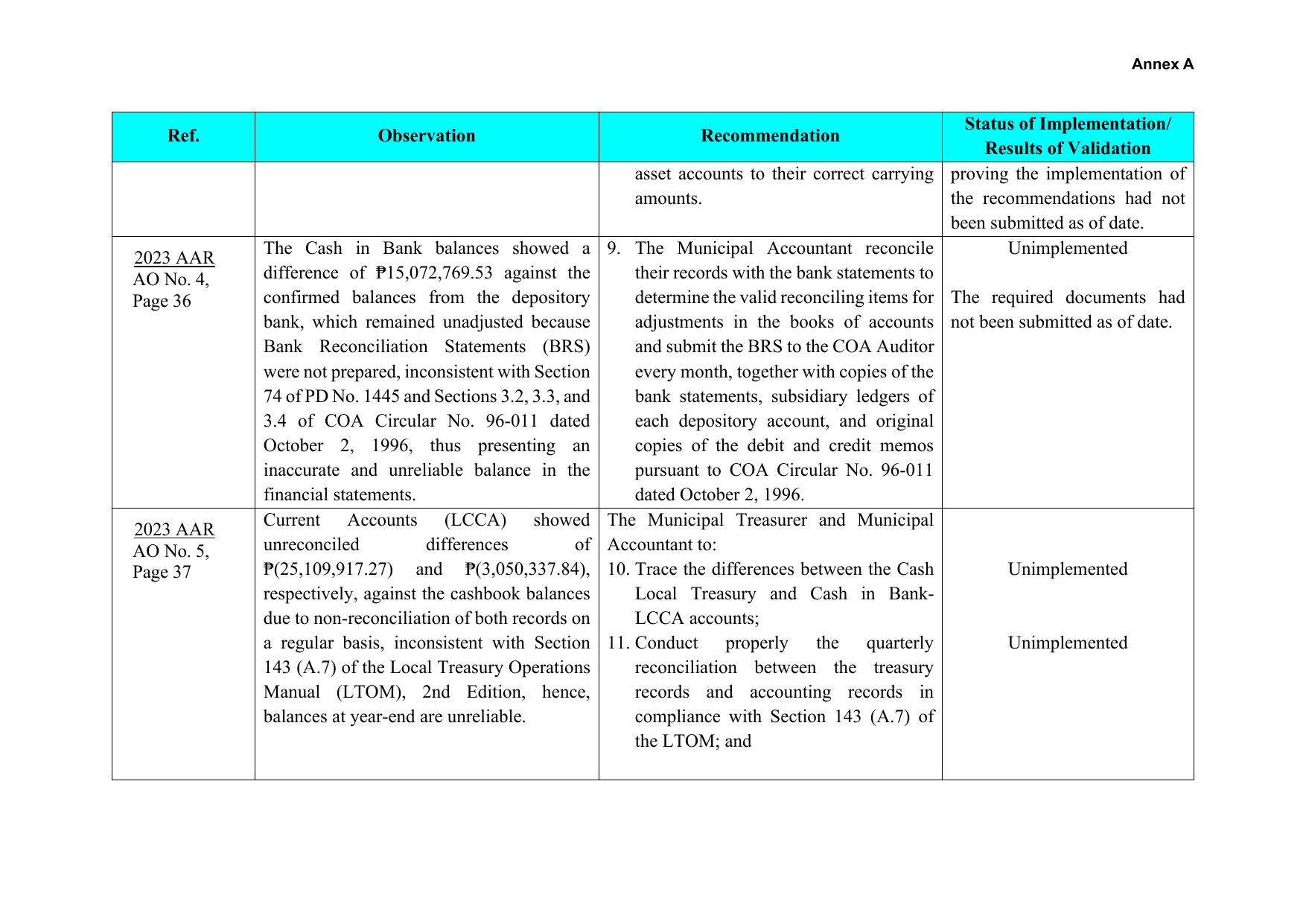

Ref. Observation Recommendation

Results of Validation

asset accounts to their correct carrying proving the implementation of

amounts. the recommendations had not

been submitted as of date.

The Cash in Bank balances showed a 9. The Municipal Accountant reconcile Unimplemented

2023 AAR

AO No. 4, difference of ₱15,072,769.53 against the their records with the bank statements to

Page 36 confirmed balances from the depository determine the valid reconciling items for The required documents had

bank, which remained unadjusted because adjustments in the books of accounts not been submitted as of date.

Bank Reconciliation Statements (BRS) and submit the BRS to the COA Auditor

were not prepared, inconsistent with Section every month, together with copies of the

74 of PD No. 1445 and Sections 3.2, 3.3, and bank statements, subsidiary ledgers of

3.4 of COA Circular No. 96-011 dated each depository account, and original

October 2, 1996, thus presenting an copies of the debit and credit memos

inaccurate and unreliable balance in the pursuant to COA Circular No. 96-011

financial statements. dated October 2, 1996.

Current Accounts (LCCA) showed The Municipal Treasurer and Municipal

2023 AAR

AO No. 5, unreconciled differences of Accountant to:

Page 37 ₱(25,109,917.27) and ₱(3,050,337.84), 10. Trace the differences between the Cash Unimplemented

respectively, against the cashbook balances Local Treasury and Cash in Bank-

due to non-reconciliation of both records on LCCA accounts;

a regular basis, inconsistent with Section 11. Conduct properly the quarterly Unimplemented

143 (A.7) of the Local Treasury Operations reconciliation between the treasury

Manual (LTOM), 2nd Edition, hence, records and accounting records in

balances at year-end are unreliable. compliance with Section 143 (A.7) of

the LTOM; and