We also recommended that henceforth, the specific duties, functions, and expected

outputs be incorporated in the individual contracts of services and that these personnel

be required to submit monthly accomplishment reports aligned with the respective

duties, functions and expected outputs to establish the necessity of their services.

Furthermore, we reiterated our recommendation that Management discontinue the use

of any government official’s name in government programs and desist from charging

to government funds any expenses related to programs that include the initials or

surname of any government personality.

4. Appropriations in the 20% Development Fund (DF) amounting to ₱11,500,000.00

for the Electrification Program in various barangays were utilized to procure

service wires for distribution to barangays at a cost of ₱11,495,167.80, without

securing the required separate Sanggunian authorization, as mandated for lump

sum appropriations under Section 22(c) of Republic Act (RA) No. 7160.

We recommended that the Provincial Development Council, when endorsing programs,

projects and activities to the Sangguniang Panlalawigan for approval, specify the

particular projects to be funded as required under Article 454(d) of the Implementing

Rules and Regulations (IRR) of RA No. 7160. For appropriations that have been

presented in lump sum or generic terms, a separate SP appropriation

ordinance/resolution must be secured by the Local Chief Executive before utilizing the

funds, as required under Section 22(c) of RA No. 7160.

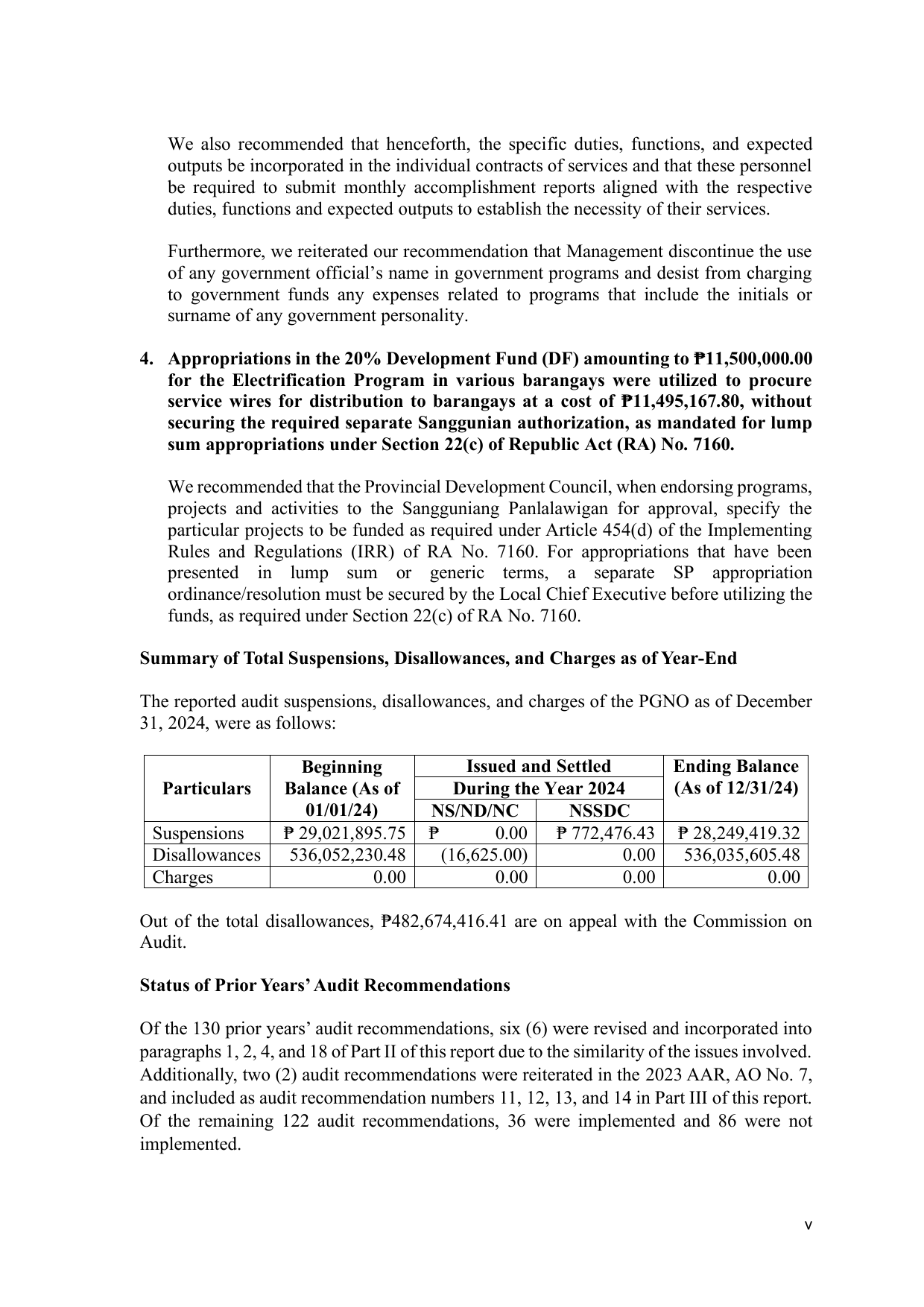

Summary of Total Suspensions, Disallowances, and Charges as of Year-End

The reported audit suspensions, disallowances, and charges of the PGNO as of December

31, 2024, were as follows:

Beginning Issued and Settled Ending Balance

Particulars Balance (As of During the Year 2024 (As of 12/31/24)

01/01/24) NS/ND/NC NSSDC

Suspensions ₱ 29,021,895.75 ₱ 0.00 ₱ 772,476.43 ₱ 28,249,419.32

Disallowances 536,052,230.48 (16,625.00) 0.00 536,035,605.48

Charges 0.00 0.00 0.00 0.00

Out of the total disallowances, ₱482,674,416.41 are on appeal with the Commission on

Audit.

Status of Prior Years’ Audit Recommendations

Of the 130 prior years’ audit recommendations, six (6) were revised and incorporated into

paragraphs 1, 2, 4, and 18 of Part II of this report due to the similarity of the issues involved.

Additionally, two (2) audit recommendations were reiterated in the 2023 AAR, AO No. 7,

and included as audit recommendation numbers 11, 12, 13, and 14 in Part III of this report.

Of the remaining 122 audit recommendations, 36 were implemented and 86 were not

implemented.

v