8.1 Section 59 of the NGAS Manual, Volume 2, states that the IIRUP shall serve as

basis for recording the derecognition of unserviceable properties from the books

of accounts, including those carried under Property, Plant and Equipment and

Inventory accounts.

8.2 Additionally, paragraph 83 of IPSAS 17 specifies that any gain or loss resulting

from the derecognition of an item of property, plant, and equipment should be

recognized in the surplus or deficit for the period in which the item is

derecognized.

8.3 Furthermore, under “Annex B” of COA Circular No. 2015-009 dated December

1, 2015, which prescribes the revised chart of accounts for local government

units, the Gain on sale of PPE account is designated for recording gains from

sale of government-owned PPE, while the Loss on sale of PPE account is used

to record losses incurred from such sales.

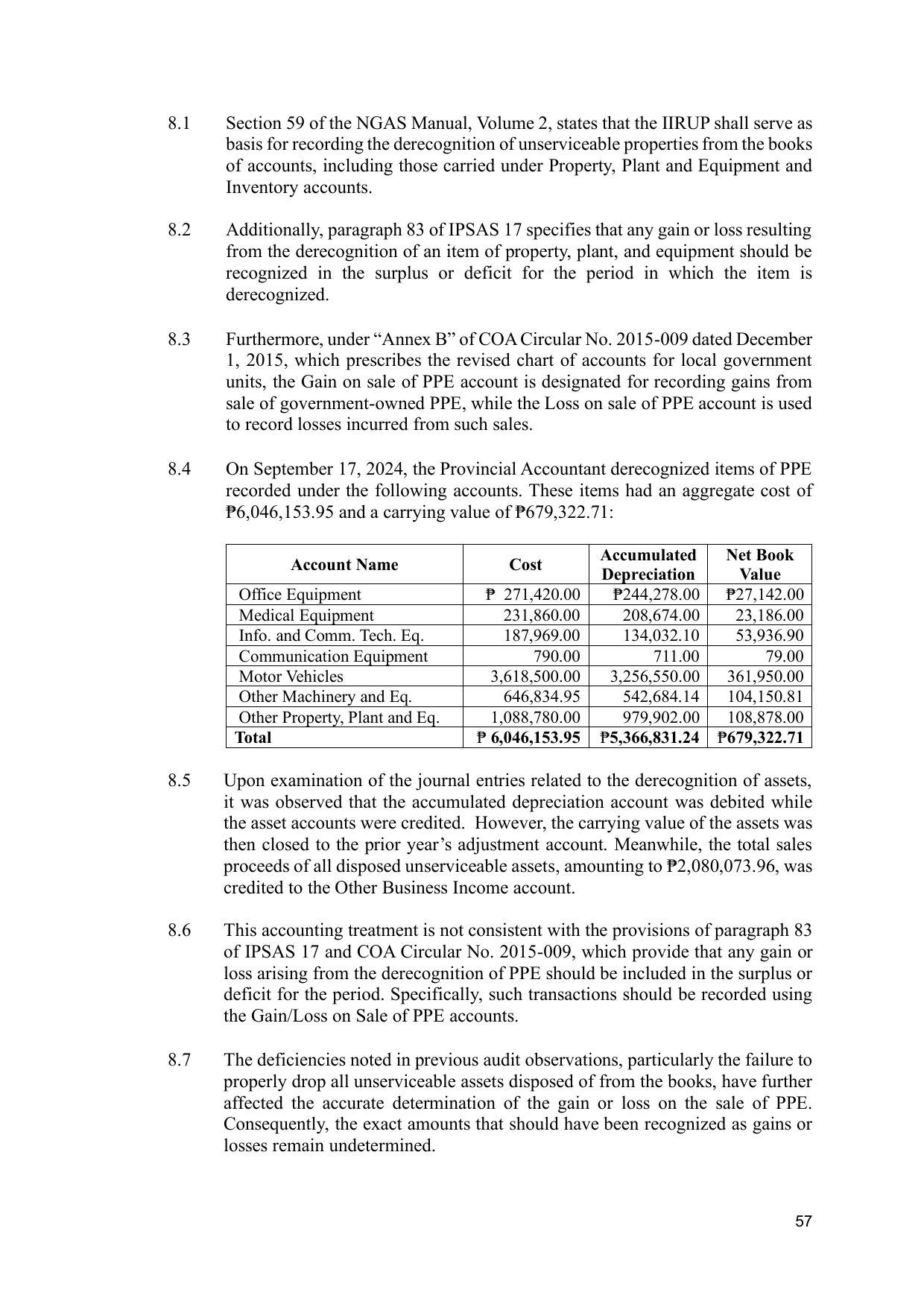

8.4 On September 17, 2024, the Provincial Accountant derecognized items of PPE

recorded under the following accounts. These items had an aggregate cost of

₱6,046,153.95 and a carrying value of ₱679,322.71:

Accumulated Net Book

Account Name Cost

Depreciation Value

Office Equipment ₱ 271,420.00 ₱244,278.00 ₱27,142.00

Medical Equipment 231,860.00 208,674.00 23,186.00

Info. and Comm. Tech. Eq. 187,969.00 134,032.10 53,936.90

Communication Equipment 790.00 711.00 79.00

Motor Vehicles 3,618,500.00 3,256,550.00 361,950.00

Other Machinery and Eq. 646,834.95 542,684.14 104,150.81

Other Property, Plant and Eq. 1,088,780.00 979,902.00 108,878.00

Total ₱ 6,046,153.95 ₱5,366,831.24 ₱679,322.71

8.5 Upon examination of the journal entries related to the derecognition of assets,

it was observed that the accumulated depreciation account was debited while

the asset accounts were credited. However, the carrying value of the assets was

then closed to the prior year’s adjustment account. Meanwhile, the total sales

proceeds of all disposed unserviceable assets, amounting to ₱2,080,073.96, was

credited to the Other Business Income account.

8.6 This accounting treatment is not consistent with the provisions of paragraph 83

of IPSAS 17 and COA Circular No. 2015-009, which provide that any gain or

loss arising from the derecognition of PPE should be included in the surplus or

deficit for the period. Specifically, such transactions should be recorded using

the Gain/Loss on Sale of PPE accounts.

8.7 The deficiencies noted in previous audit observations, particularly the failure to

properly drop all unserviceable assets disposed of from the books, have further

affected the accurate determination of the gain or loss on the sale of PPE.

Consequently, the exact amounts that should have been recognized as gains or

losses remain undetermined.

57