borrowing costs are capitalized when it is probable that they will result in future

economic benefits or service potential for the entity and when the costs can be

measured reliably.

6.4 The standard further states that the financial statements should disclose the

accounting policy adopted for borrowing costs and where an entity adopts the

allowed alternative treatment, that treatment shall be applied consistently to all

borrowing costs that are directly attributable to the acquisition, construction, or

production of all qualifying assets of the entity.

6.5 In line therewith, Note 3.9 of the Notes to the Financial Statements of the

Provincial Government for CY 2024 disclosed that borrowing costs are

capitalized against qualifying assets as part of property, plant and equipment.

Such borrowing costs are capitalized over the period during which the asset is

being acquired or constructed and borrowings have been incurred.

Capitalization ceases when the construction of the asset is complete.

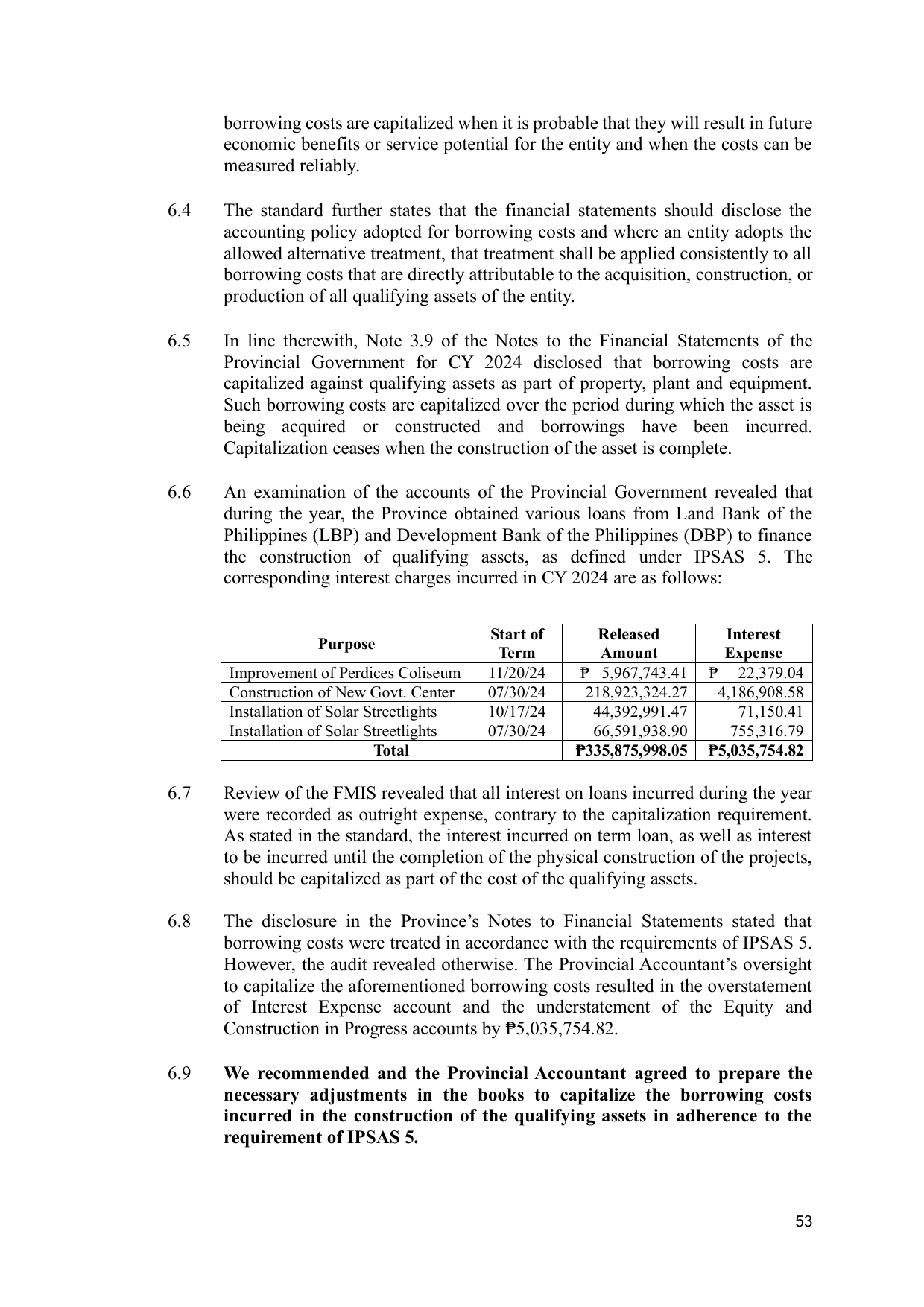

6.6 An examination of the accounts of the Provincial Government revealed that

during the year, the Province obtained various loans from Land Bank of the

Philippines (LBP) and Development Bank of the Philippines (DBP) to finance

the construction of qualifying assets, as defined under IPSAS 5. The

corresponding interest charges incurred in CY 2024 are as follows:

Start of Released Interest

Purpose

Term Amount Expense

Improvement of Perdices Coliseum 11/20/24 ₱ 5,967,743.41 ₱ 22,379.04

Construction of New Govt. Center 07/30/24 218,923,324.27 4,186,908.58

Installation of Solar Streetlights 10/17/24 44,392,991.47 71,150.41

Installation of Solar Streetlights 07/30/24 66,591,938.90 755,316.79

Total ₱335,875,998.05 ₱5,035,754.82

6.7 Review of the FMIS revealed that all interest on loans incurred during the year

were recorded as outright expense, contrary to the capitalization requirement.

As stated in the standard, the interest incurred on term loan, as well as interest

to be incurred until the completion of the physical construction of the projects,

should be capitalized as part of the cost of the qualifying assets.

6.8 The disclosure in the Province’s Notes to Financial Statements stated that

borrowing costs were treated in accordance with the requirements of IPSAS 5.

However, the audit revealed otherwise. The Provincial Accountant’s oversight

to capitalize the aforementioned borrowing costs resulted in the overstatement

of Interest Expense account and the understatement of the Equity and

Construction in Progress accounts by ₱5,035,754.82.

6.9 We recommended and the Provincial Accountant agreed to prepare the

necessary adjustments in the books to capitalize the borrowing costs

incurred in the construction of the qualifying assets in adherence to the

requirement of IPSAS 5.

53