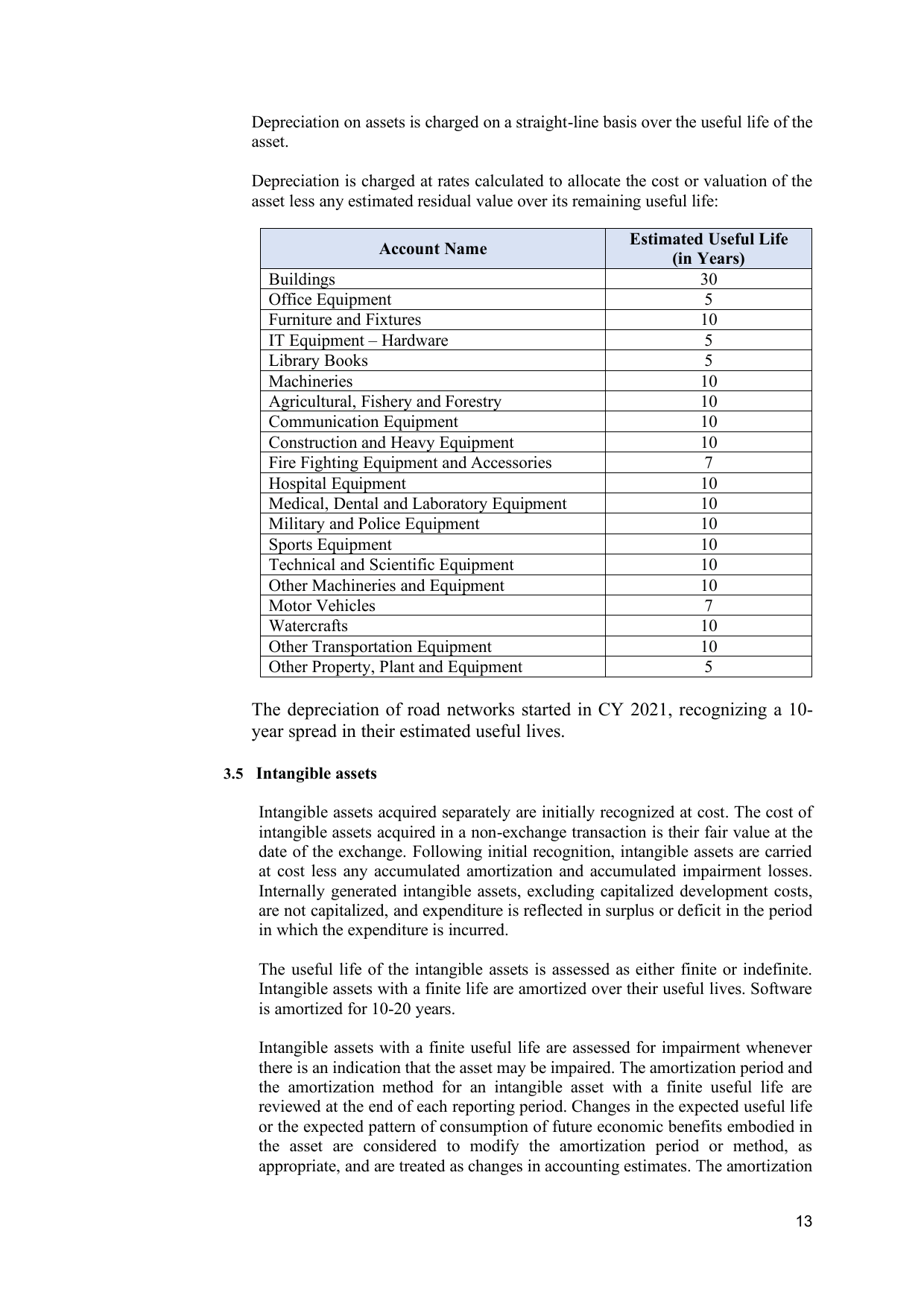

Depreciation on assets is charged on a straight-line basis over the useful life of the

asset.

Depreciation is charged at rates calculated to allocate the cost or valuation of the

asset less any estimated residual value over its remaining useful life:

Estimated Useful Life

Account Name

(in Years)

Buildings 30

Office Equipment 5

Furniture and Fixtures 10

IT Equipment – Hardware 5

Library Books 5

Machineries 10

Agricultural, Fishery and Forestry 10

Communication Equipment 10

Construction and Heavy Equipment 10

Fire Fighting Equipment and Accessories 7

Hospital Equipment 10

Medical, Dental and Laboratory Equipment 10

Military and Police Equipment 10

Sports Equipment 10

Technical and Scientific Equipment 10

Other Machineries and Equipment 10

Motor Vehicles 7

Watercrafts 10

Other Transportation Equipment 10

Other Property, Plant and Equipment 5

The depreciation of road networks started in CY 2021, recognizing a 10-

year spread in their estimated useful lives.

3.5 Intangible assets

Intangible assets acquired separately are initially recognized at cost. The cost of

intangible assets acquired in a non-exchange transaction is their fair value at the

date of the exchange. Following initial recognition, intangible assets are carried

at cost less any accumulated amortization and accumulated impairment losses.

Internally generated intangible assets, excluding capitalized development costs,

are not capitalized, and expenditure is reflected in surplus or deficit in the period

in which the expenditure is incurred.

The useful life of the intangible assets is assessed as either finite or indefinite.

Intangible assets with a finite life are amortized over their useful lives. Software

is amortized for 10-20 years.

Intangible assets with a finite useful life are assessed for impairment whenever

there is an indication that the asset may be impaired. The amortization period and

the amortization method for an intangible asset with a finite useful life are

reviewed at the end of each reporting period. Changes in the expected useful life

or the expected pattern of consumption of future economic benefits embodied in

the asset are considered to modify the amortization period or method, as

appropriate, and are treated as changes in accounting estimates. The amortization

13