Page 151 of 161

Ref. Status of

Audit Observations Audit Recommendations

Implementation

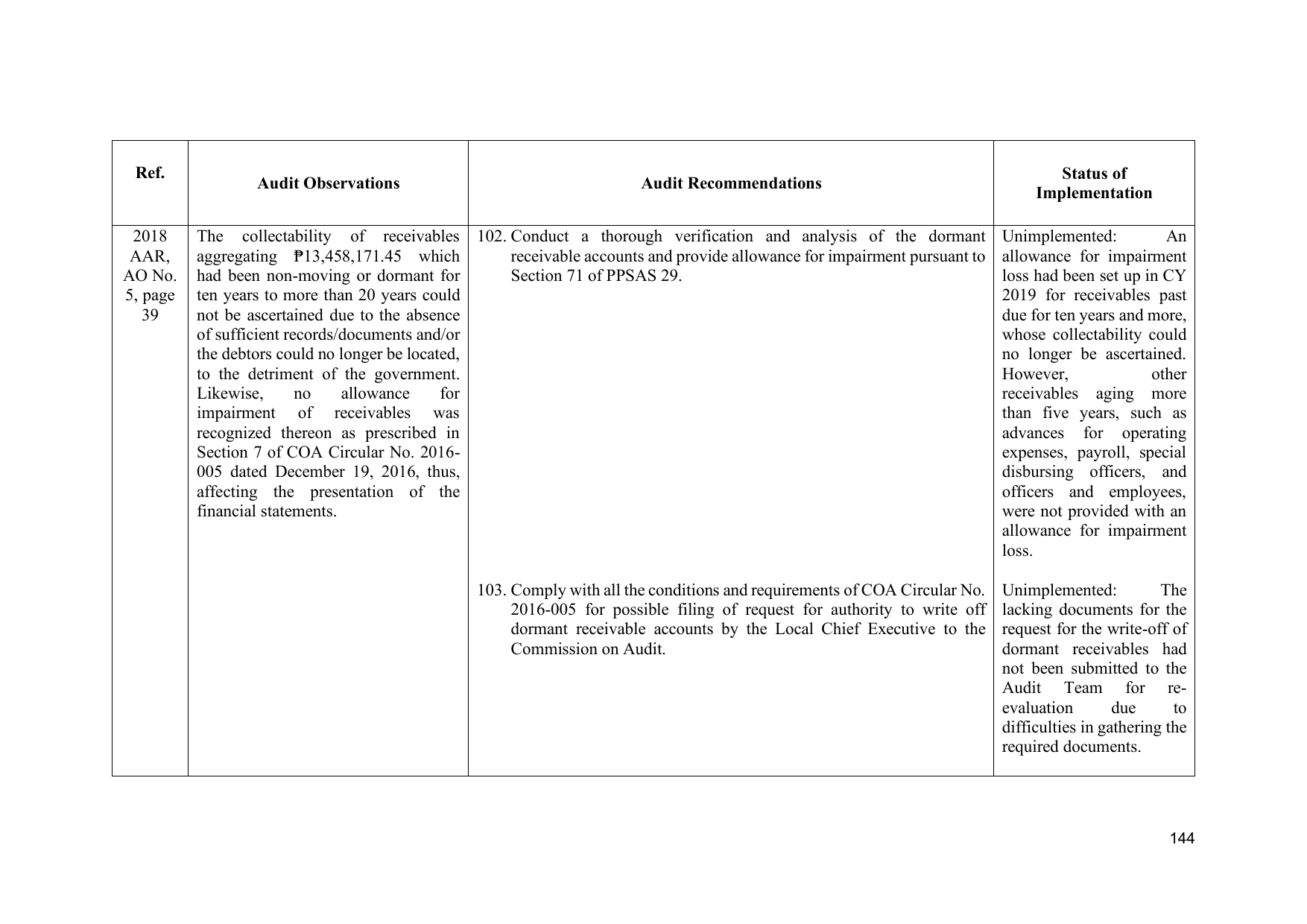

2018 The collectability of receivables 102. Conduct a thorough verification and analysis of the dormant Unimplemented: An

AAR, aggregating ₱13,458,171.45 which receivable accounts and provide allowance for impairment pursuant to allowance for impairment

AO No. had been non-moving or dormant for Section 71 of PPSAS 29. loss had been set up in CY

5, page ten years to more than 20 years could 2019 for receivables past

39 not be ascertained due to the absence due for ten years and more,

of sufficient records/documents and/or whose collectability could

the debtors could no longer be located, no longer be ascertained.

to the detriment of the government. However, other

Likewise, no allowance for receivables aging more

impairment of receivables was than five years, such as

recognized thereon as prescribed in advances for operating

Section 7 of COA Circular No. 2016- expenses, payroll, special

005 dated December 19, 2016, thus, disbursing officers, and

affecting the presentation of the officers and employees,

financial statements. were not provided with an

allowance for impairment

loss.

103. Comply with all the conditions and requirements of COA Circular No. Unimplemented: The

2016-005 for possible filing of request for authority to write off lacking documents for the

dormant receivable accounts by the Local Chief Executive to the request for the write-off of

Commission on Audit. dormant receivables had

not been submitted to the

Audit Team for re-

evaluation due to

difficulties in gathering the

required documents.

144