APMT — Page 11 of 90

AGENCY ACTION PLAN and STATUS of IMPLEMENTATION RESULTS of COA VALIDATION

Agency Action Plan (for Partially Implemented

and Not Implemented Recommendations) Reason for Actual

Status of Partial/Delay/ Action Date Status of

Audit Action Plan/ Target Implementation

Ref. Audit Observations Person/ Implemen- Non- Taken/Action Follow Implemen- Remarks

Recommendations Remarks Department Implementati Implementation, Date

Responsible tation to be Taken Up tation

on Date if applicable

From To From To

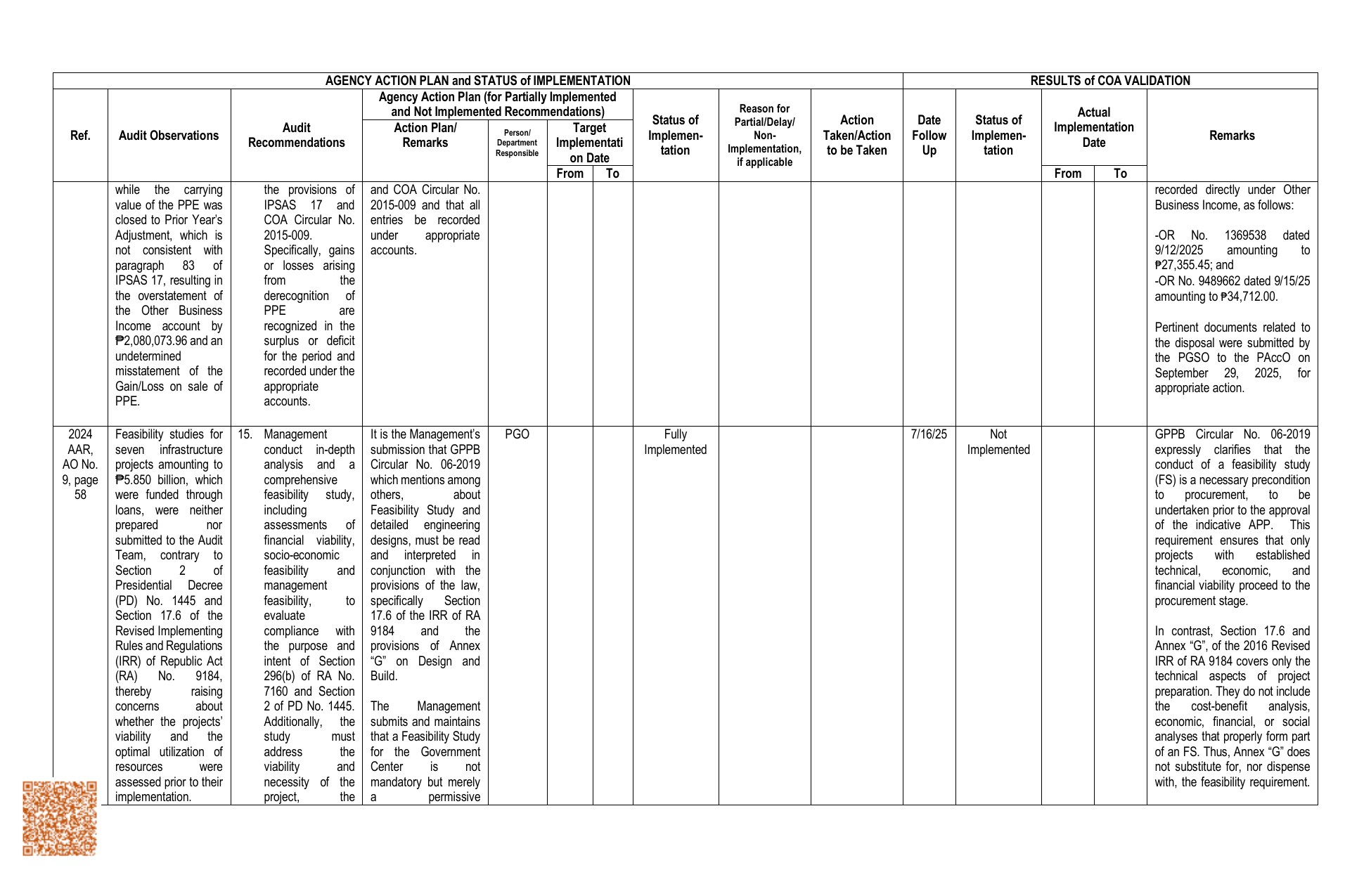

while the carrying the provisions of and COA Circular No. recorded directly under Other

value of the PPE was IPSAS 17 and 2015-009 and that all Business Income, as follows:

closed to Prior Year’s COA Circular No. entries be recorded

Adjustment, which is 2015-009. under appropriate -OR No. 1369538 dated

not consistent with Specifically, gains accounts. 9/12/2025 amounting to

paragraph 83 of or losses arising ₱27,355.45; and

IPSAS 17, resulting in from the -OR No. 9489662 dated 9/15/25

the overstatement of derecognition of amounting to ₱34,712.00.

the Other Business PPE are

Income account by recognized in the Pertinent documents related to

₱2,080,073.96 and an surplus or deficit the disposal were submitted by

undetermined for the period and the PGSO to the PAccO on

misstatement of the recorded under the September 29, 2025, for

Gain/Loss on sale of appropriate appropriate action.

PPE. accounts.

2024 Feasibility studies for 15. Management It is the Management’s PGO Fully 7/16/25 Not GPPB Circular No. 06-2019

AAR, seven infrastructure conduct in-depth submission that GPPB Implemented Implemented expressly clarifies that the

AO No. projects amounting to analysis and a Circular No. 06-2019 conduct of a feasibility study

9, page ₱5.850 billion, which comprehensive which mentions among (FS) is a necessary precondition

58 were funded through feasibility study, others, about to procurement, to be

loans, were neither including Feasibility Study and undertaken prior to the approval

prepared nor assessments of detailed engineering of the indicative APP. This

submitted to the Audit financial viability, designs, must be read requirement ensures that only

Team, contrary to socio-economic and interpreted in projects with established

Section 2 of feasibility and conjunction with the technical, economic, and

Presidential Decree management provisions of the law, financial viability proceed to the

(PD) No. 1445 and feasibility, to specifically Section procurement stage.

Section 17.6 of the evaluate 17.6 of the IRR of RA

Revised Implementing compliance with 9184 and the In contrast, Section 17.6 and

Rules and Regulations the purpose and provisions of Annex Annex “G”, of the 2016 Revised

(IRR) of Republic Act intent of Section “G” on Design and IRR of RA 9184 covers only the

(RA) No. 9184, 296(b) of RA No. Build. technical aspects of project

thereby raising 7160 and Section preparation. They do not include

concerns about 2 of PD No. 1445. The Management the cost-benefit analysis,

whether the projects’ Additionally, the submits and maintains economic, financial, or social

viability and the study must that a Feasibility Study analyses that properly form part

optimal utilization of address the for the Government of an FS. Thus, Annex “G” does

resources were viability and Center is not not substitute for, nor dispense

assessed prior to their necessity of the mandatory but merely with, the feasibility requirement.

implementation. project, the a permissive