Reason for

Agency Action Plan (for Partially Implemented and Not Implemented Stats nten Partial/Delay/No Action Taken/Action

Recommendations) i a ~ to be Taken

ee | ee een ne et ne ee | HO | Implementation, | od

if applicable

Audit Observations Audit Recommendations | Action Plan/ Target .

Remarks Implementation

This column shall be filled out by the Dee nent Date

agency, detailing the appropriate

course of action on the audit Responsible P|

observation identified. [irom [io |

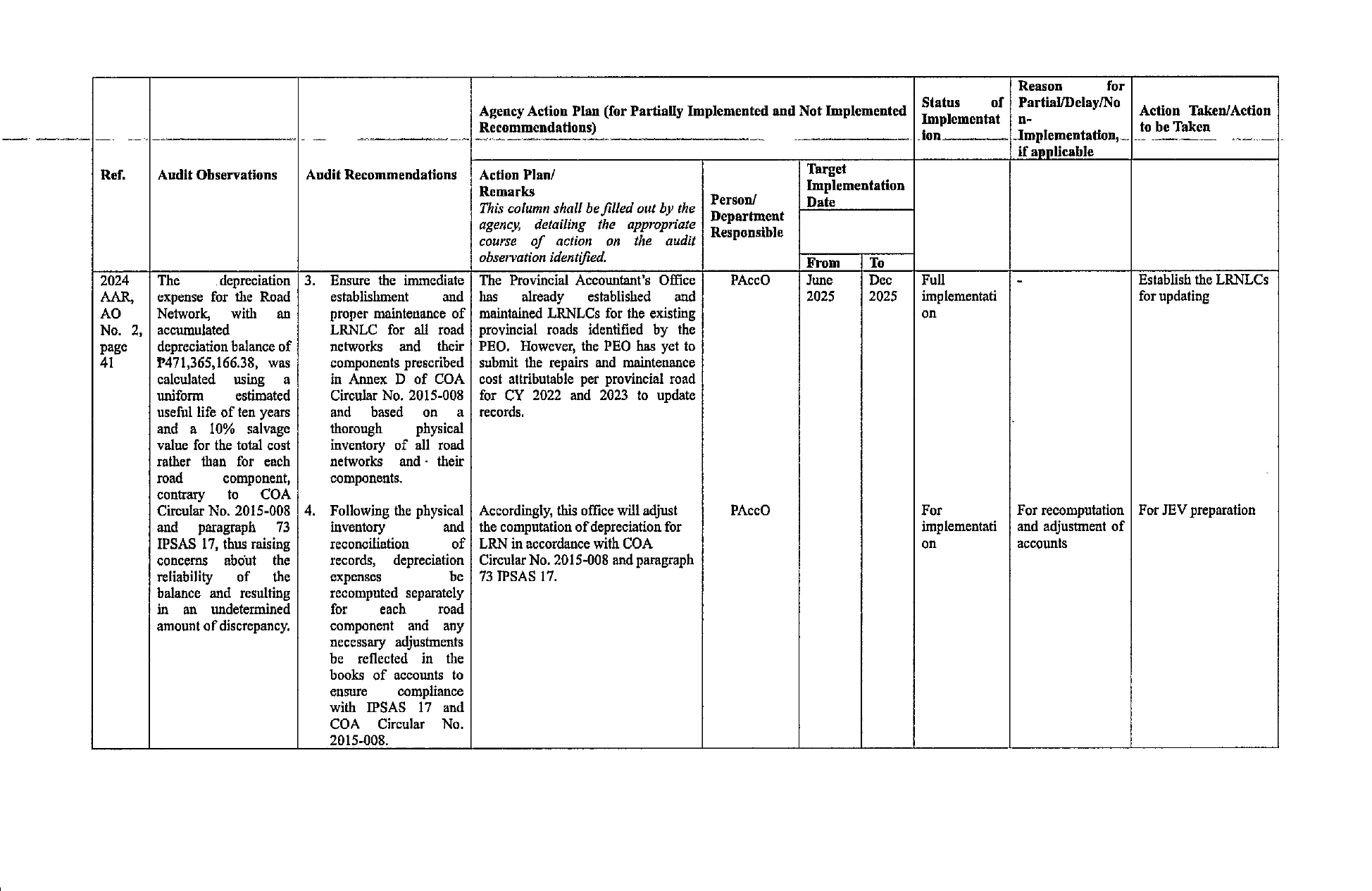

2024 | The depreciation | 3. Ensure the immediate | The Provincial Accountant’s Office PAccO June Dec Full - Establish the LRNLCs

AAR, | expense for the Road establishment and} has already — established = and 2025 2025 | implementati for updating

AO Network, with an proper maintenance of | maintained LRNLCs for the existing on

No. 2, | accumulated LRNLC for ali road | provincial roads identified by the

page depreciation balance of networks and their | PEO, However, the PEO has yet to

41 P471,365,166.38, was components prescribed | submit the repairs and maintenance

calculated using a in Annex D of COA | cost attributable per provincial road

uniform estimated Circular No. 2015-008 | for CY 2022 and 2023 to update

useful life of ten years and based on a| records.

and a 10% salvage thorough physical P

value for the total cost inventory of all road

rather than for each networks and- their

road component, components,

contrary to COA

Circular No. 2015-008 | 4. Following the physical | Accordingly, this office will adjust PAccO For For recomputation | For JEV preparation

and patagtraph 73 inventory and | the computation of depreciation for implementati | and adjustment of

IPSAS 17, thus raising reconciliation of | LRN in accordance with COA on accounts

concerns about the records, depreciation | Circular No. 2015-008 and paragraph

reliability of the expenses be | 73 IPSAS 17.

balance and resulting recomputed separately

in an undetermined for each, road

amount of discrepancy, component and any

necessary adjustments

be reflected in the

books of accounts to

ensure compliance

with IPSAS 17 and

COA Circular No.

2015-008.