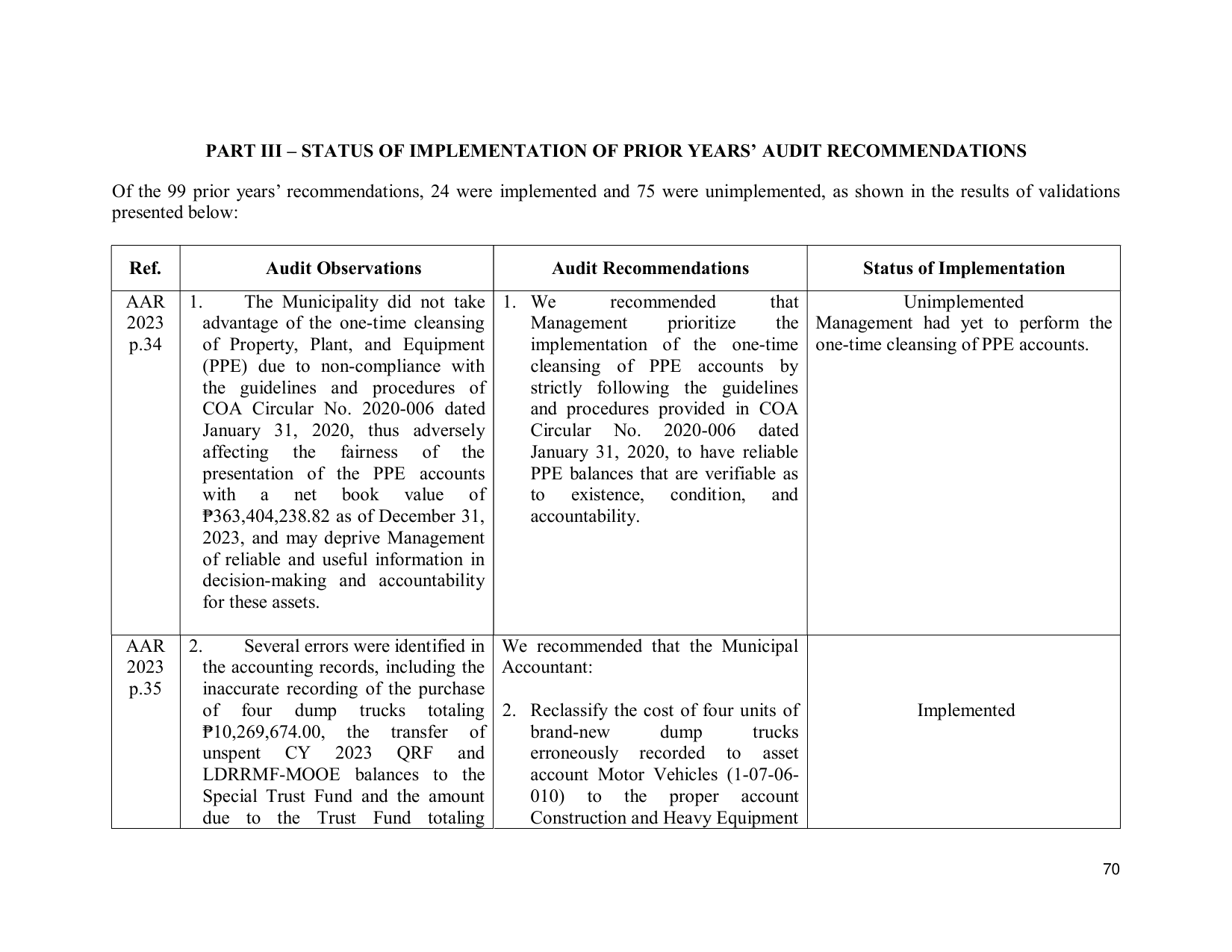

PART III – STATUS OF IMPLEMENTATION OF PRIOR YEARS’ AUDIT RECOMMENDATIONS

Of the 99 prior years’ recommendations, 24 were implemented and 75 were unimplemented, as shown in the results of validations

presented below:

Ref. Audit Observations Audit Recommendations Status of Implementation

AAR 1. The Municipality did not take 1. We recommended that Unimplemented

2023 advantage of the one-time cleansing Management prioritize the Management had yet to perform the

p.34 of Property, Plant, and Equipment implementation of the one-time one-time cleansing of PPE accounts.

(PPE) due to non-compliance with cleansing of PPE accounts by

the guidelines and procedures of strictly following the guidelines

COA Circular No. 2020-006 dated and procedures provided in COA

January 31, 2020, thus adversely Circular No. 2020-006 dated

affecting the fairness of the January 31, 2020, to have reliable

presentation of the PPE accounts PPE balances that are verifiable as

with a net book value of to existence, condition, and

₱363,404,238.82 as of December 31, accountability.

2023, and may deprive Management

of reliable and useful information in

decision-making and accountability

for these assets.

AAR 2. Several errors were identified in We recommended that the Municipal

2023 the accounting records, including the Accountant:

p.35 inaccurate recording of the purchase

of four dump trucks totaling 2. Reclassify the cost of four units of Implemented

₱10,269,674.00, the transfer of brand-new dump trucks

unspent CY 2023 QRF and erroneously recorded to asset

LDRRMF-MOOE balances to the account Motor Vehicles (1-07-06-

Special Trust Fund and the amount 010) to the proper account

due to the Trust Fund totaling Construction and Heavy Equipment

70