14.7 Inconsistent with the above requirements, Management was unable to submit a copy

of their Annual GPB and the corresponding GAD AR to the Audit Team within the

specified timeframe.

14.8 The inability to furnish the Audit Team with the required documents within the

specified timeframe compromised the timely evaluation of the Municipality’s GAD

implementation and responsiveness, as intended under the applicable regulations.

14.9 We recommended and Management agreed to submit the GPB and AR to the

PPDO and DILG Provincial Office within the prescribed period in accordance

with Section 4.0 of PCW-DBM-DILG-NEDA JMC No. 2016-01 dated February

12, 2016.

14.10 We also recommended and Management agreed to strictly adhere to Item V of

COA Circular No. 2014-001 dated March 18, 2014, for the timely submission of

the said reports to the COA Audit Team.

14.11 We further recommended and Management agreed to ensure that the GAD AR

is accompanied by the required reports listed under Section C.8 (5) of the PCW-

DILG-DBM-NEDA JMC No. 2013-01.

SEF Utilization Report

15. The Local School Board (LSB) has not fully complied with the required posting and

submission of the Quarterly SEF Utilization Reports to DepEd and other relevant

authorities, as stipulated in Item 6.1 of the DepEd-DBM-DILG JC No. 1, s. 2017

dated January 19, 2017, thus hindering effective monitoring, transparency, and

accountability in the allocation and utilization of the SEF.

15.1 The Department of Education (DepEd), Department of Budget and Management

(DBM), and the Department of the Interior and Local Government (DepEd-DBM-

DILG) issued Joint Circular (JC) No. 1 dated January 19, 2017, to provide revised

guidelines on the use of the Special Education Fund (SEF). Specifically, Item 6.1 of

the JC states that:

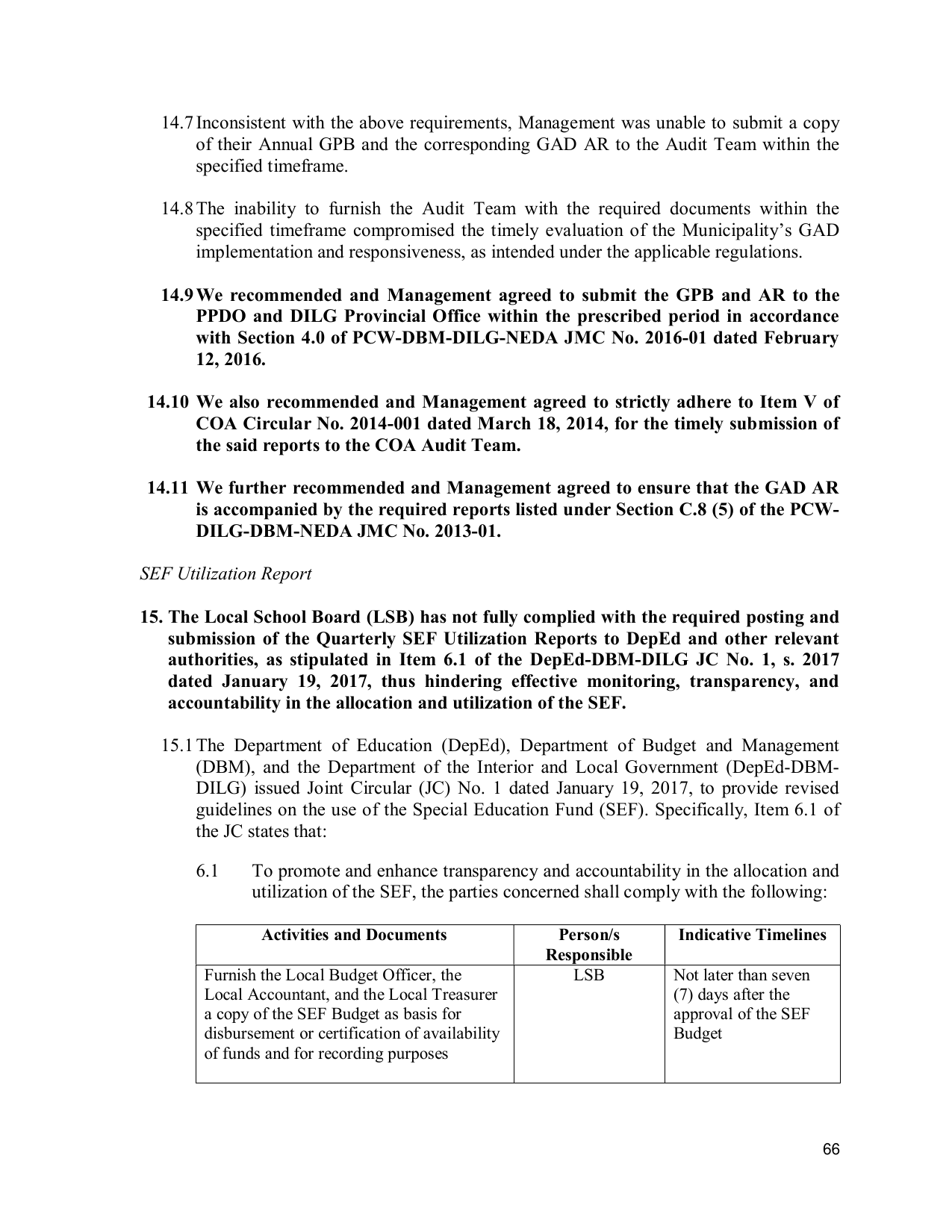

6.1 To promote and enhance transparency and accountability in the allocation and

utilization of the SEF, the parties concerned shall comply with the following:

Activities and Documents Person/s Indicative Timelines

Responsible

Furnish the Local Budget Officer, the LSB Not later than seven

Local Accountant, and the Local Treasurer (7) days after the

a copy of the SEF Budget as basis for approval of the SEF

disbursement or certification of availability Budget

of funds and for recording purposes

66