4.14 We further recommended and the Municipal Treasurer, Municipal Accountant,

and all accountable officers agreed to ensure the preparation, maintenance, and

use of all required forms, registries, and reports for the proper tracking,

issuance, transfer, return, and disposal of semi-expendable properties, as

enumerated in Section 4.7 of COA Circular No. 2024-006.

4.15 The Municipal Accountant submitted a pro forma JEV but will still need to verify the

final amounts to be adjusted.

Erroneous LDRRM Expense Entries

5. The cost of 1,500 sacks of rice, amounting to ₱4,116,000.00, charged to the previous

years’ unexpended LDRRMF was recognized as credit to Subsidy from Other

Funds instead of closing the recorded Welfare Goods Expenses account to the Trust

Fund Liabilities-DRRMF account. This treatment is inconsistent with COA

Circular Nos. 2012-002 and 2015-009 dated September 12, 2012 and December 1,

2015, respectively, thus, proper accounting was not assured.

5.1 COA Circular No. 2012-002 dated September 12, 2012, prescribes the accounting and

reporting guidelines for the Local Disaster Risk Reduction and Management Fund

(LDRRMF) of Local Government Units (LGUs), the National DRRMF provided to

LGUs, and receipts from other sources.

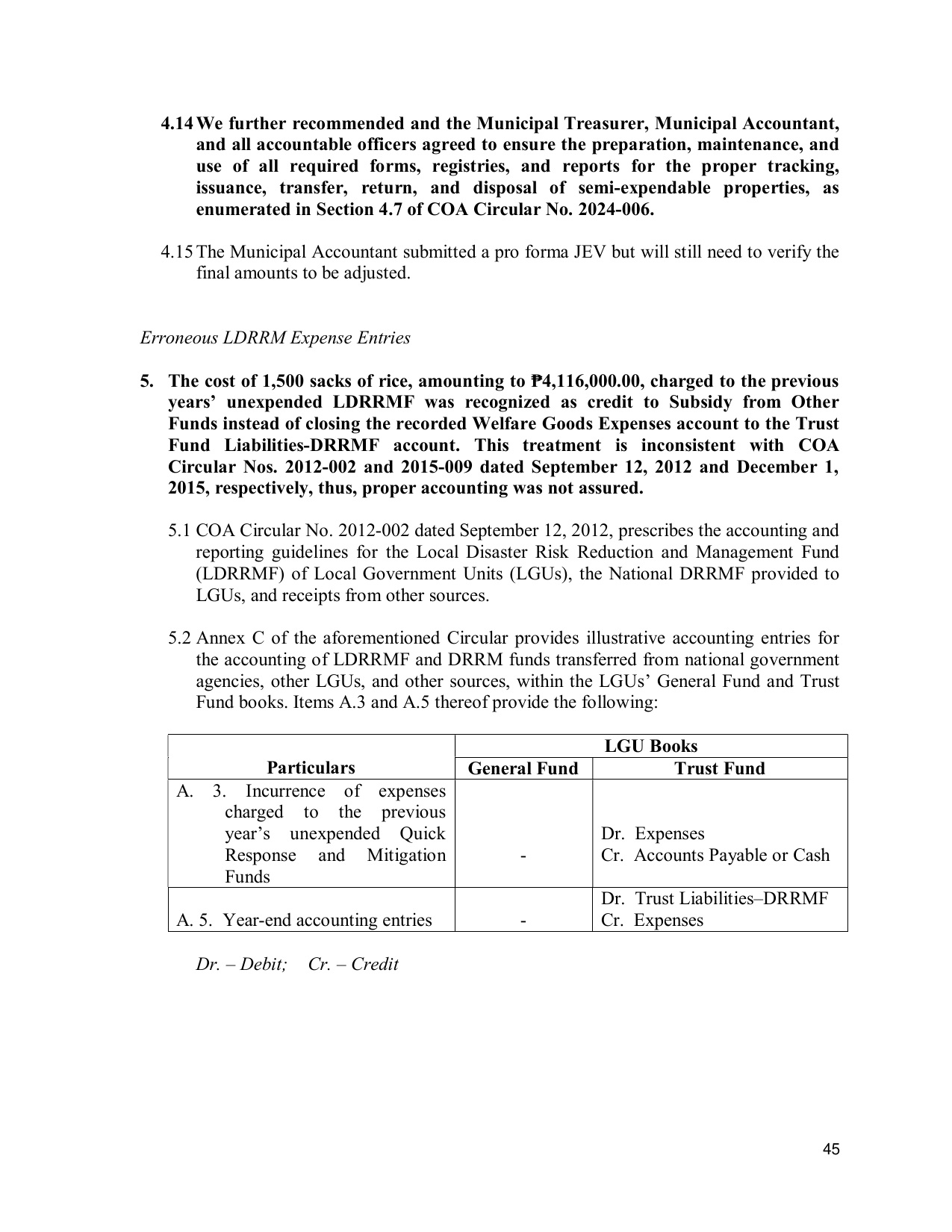

5.2 Annex C of the aforementioned Circular provides illustrative accounting entries for

the accounting of LDRRMF and DRRM funds transferred from national government

agencies, other LGUs, and other sources, within the LGUs’ General Fund and Trust

Fund books. Items A.3 and A.5 thereof provide the following:

LGU Books

Particulars General Fund Trust Fund

A. 3. Incurrence of expenses

charged to the previous

year’s unexpended Quick Dr. Expenses

Response and Mitigation - Cr. Accounts Payable or Cash

Funds

Dr. Trust Liabilities–DRRMF

A. 5. Year-end accounting entries - Cr. Expenses

Dr. – Debit; Cr. – Credit

45