or more and against which no actual claims, administrative or judicial, have been

filed or which are not covered by perfected contracts on record.

2.3 While we are aware that the above provisions pertain specifically to the unliquidated

balances of accounts payable in the books of the national government, Honorable

Celso D. Gangan, former Chairman of the Commission on Audit, as stated in his 5th

Indorsement dated September 2, 1998, reads in part:

“ Every statute be construed in connection with those already

existing in relation to the same subject matter and should be

made to harmonize and stand tighter if they can be done by fair

and reasonable interpretation. (City of Naga vs. Agna SCRA 176)

x x x.”

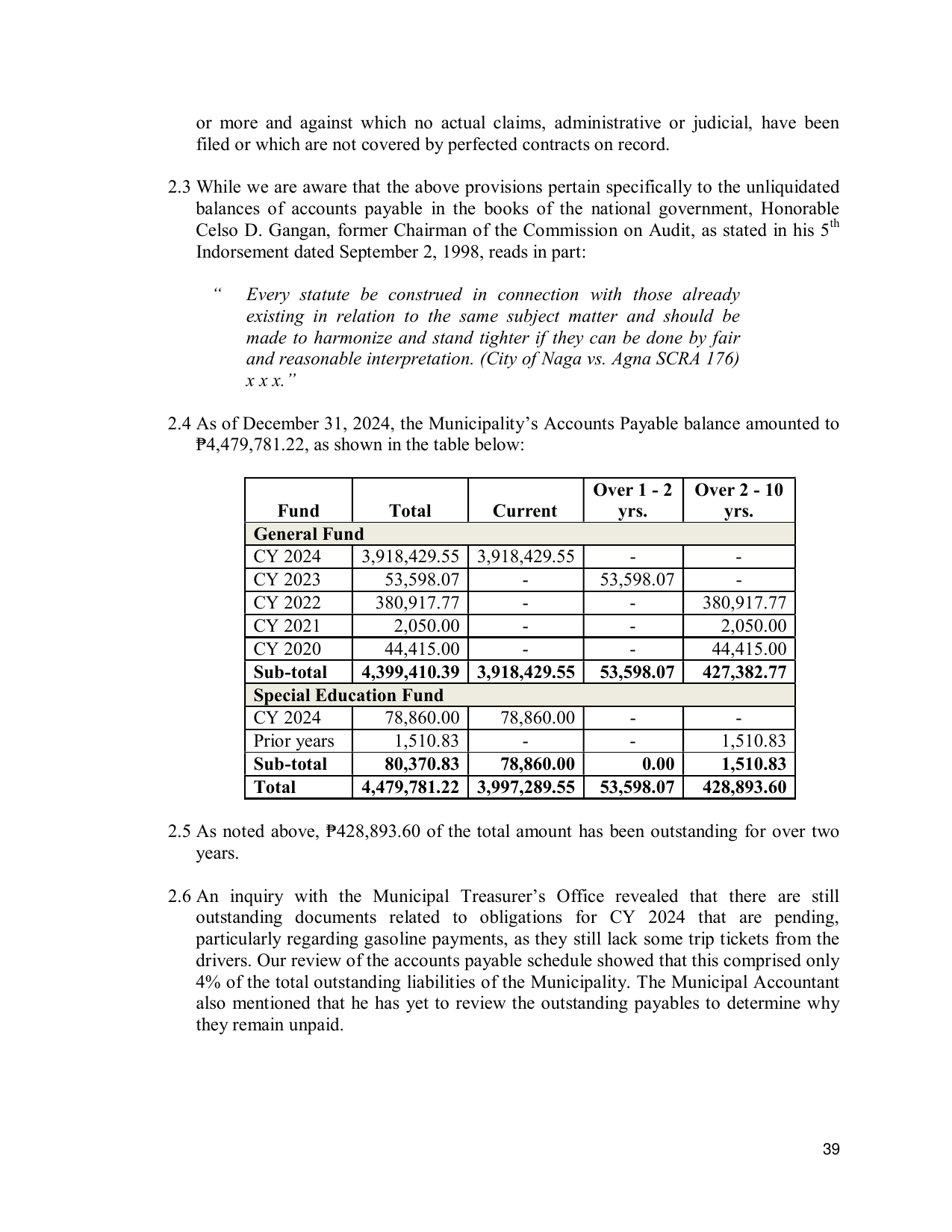

2.4 As of December 31, 2024, the Municipality’s Accounts Payable balance amounted to

₱4,479,781.22, as shown in the table below:

Over 1 - 2 Over 2 - 10

Fund Total Current yrs. yrs.

General Fund

CY 2024 3,918,429.55 3,918,429.55 - -

CY 2023 53,598.07 - 53,598.07 -

CY 2022 380,917.77 - - 380,917.77

CY 2021 2,050.00 - - 2,050.00

CY 2020 44,415.00 - - 44,415.00

Sub-total 4,399,410.39 3,918,429.55 53,598.07 427,382.77

Special Education Fund

CY 2024 78,860.00 78,860.00 - -

Prior years 1,510.83 - - 1,510.83

Sub-total 80,370.83 78,860.00 0.00 1,510.83

Total 4,479,781.22 3,997,289.55 53,598.07 428,893.60

2.5 As noted above, ₱428,893.60 of the total amount has been outstanding for over two

years.

2.6 An inquiry with the Municipal Treasurer’s Office revealed that there are still

outstanding documents related to obligations for CY 2024 that are pending,

particularly regarding gasoline payments, as they still lack some trip tickets from the

drivers. Our review of the accounts payable schedule showed that this comprised only

4% of the total outstanding liabilities of the Municipality. The Municipal Accountant

also mentioned that he has yet to review the outstanding payables to determine why

they remain unpaid.

39